Loans based on income are not as big as loans based on collateral, like an apartment.

How much one can borrow from a bank to purchase a house, or other real estate, can be determined using one of two methods. The first is to use LTV, or loan-to-value ratio. It is based on the price of the collateral. If the LTV is 60 percent, then the bank would lend 60 percent of the value of the real estate to the borrower.

The other method uses DTI to determine whether or not one can afford to pay a loan.

If the bank is to lend to a borrower based on 40 percent DTI, it means that the total amount a borrower would pay annually, including the principal and interest, should not exceed 40 percent of the person’s total annual income. The DTI shows the bank whether the borrower has the ability to repay the loan or not. In this case, the value of the collateral is not considered.

Before last year, it was not difficult to take out a loan using real estate as collateral. How much money the buyer actually had did not really matter.

For example, to purchase a 700-million-won apartment, a buyer could borrow from the bank 60 percent of the price at a 60 percent LTV ratio. So someone with 280 million won on hand could buy an apartment as expensive as 700 million won.

At that time, prices of apartments and other real estate were skyrocketing, so virtually everybody was buying real estate by borrowing from the banks. The increased demand automatically led to higher real estate prices. It’s natural: with more demand, the prices got higher.

If a bank lends money based on the DTI ratio, the price of an apartment has nothing to do with the amount of money can be borrowed.

Apart from annual income, there are other factors to be calculated before deciding how much a person can borrow; these are interest rate and how long the borrower intends to take to repay the loan.

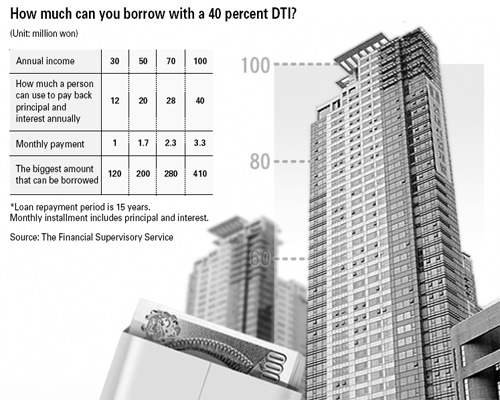

If a person with an annual income of 30 million won wants to borrow money based on a 40 percent DTI, the annual amount that he can afford to pay back toward the principal and interest is 12 million won. With a 5.58 percent interest rate and 15 years as the loan’s repayment period, the total amount that this person can borrow from the bank is 120 million.

It’s a mistake to simply multiply 12 million by 15 years. The formula is complicated, so specific numbers are calculated by using the banks’ formula tables.

When the LTV ratio is applied, the total amount that could be borrowed is 480 million won for a 700-million won apartment, while with DTI, it is only 120 million. Using the DTI method would reduce the amount of loans, which would lead to less real estate demand. So the government is requiring banks to use the DTI in speculative areas.

This regulation was an idea conceived by the Financial Supervisory Service to cool down the real estate market. It was introduced first in August 2005, but was only applied to unmarried borrowers under the age of 30 and those whose spouses already had loans with real estate as collateral. On March 30, 2006, it was applied to people buying apartments with prices higher than 600 million won in areas designated as speculative.

In November last year, the area where DTI was applied expanded to most of the Seoul metropolitan region, in an effort to dampen the speculative boom. People wanting to borrow money from banks felt disadvantaged compared to others who were able to borrow more before the DTI policy. The Service, however, will continue enforcing the policy, claiming that the excessive number of loans is the biggest reason for the sudden increase in real estate prices.

What are the problems in applying the DTI ratio? The basic idea, a “loan based on income” is fine, but one problem is that it is hard to know the income of people who are self-employed. Usually, they tend to report less than they actually make, to avoid taxes. If the DTI policy is applied, these people could borrow based on less than their actual income.

Some ideas have been introduced to solve this problem, for instance, looking at the borrowers’ credit card use and other expenses. However, this idea has yet to be fully explored.

Up to now, Korean banks only lent money to those who could provide collateral.

That made it easy to recover the loss when a borrower could not repay the loan. The bank would simply sell the collateral. In the West, this is known as “predatory lending,” because the lender takes away the collateral if a borrower cannot repay a loan. Not all loans are based on collateral.

There are loans made on credit. Banks use the CSS, or the credit rating system, and sometimes lend as much as 100 percent of the borrower’s income.

The application of DTI is a policy not only for real estate loans, but for all loans. The Financial Supervisory Service recently announced that the DTI will be applied to all financial institutions nationwide as early as February.

The Service and banks have formed a task force to draw up a “model standard.”

The new policy has been welcomed by analysts, although some say it may be a bit late.

By Choi Joon-ho JoongAng Ilbo [ebusiness@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)