What is a government debt relief program?

That’s when the U.S. government announced it would provide $100 billion in a relief program for the two mortgage financing companies Fannie Mae and Freddie Mac.

Fannie Mae and Freddie Mae were originally strong companies.

However, they ran into trouble after the real estate market in the United States began to dramatically lose value.

Rumors spread that the two companies might go bankrupt.

The problem is that if they had closed business, the impact of their demise would have been felt far and wide.

The financial companies that invested in Fannie Mae would hit rocky water and, in turn, it would become difficult for private companies to borrow money.

There was a real danger of a destabilizing chain reaction rocking the world’s financial base.

But on Sept. 9, the stock market appeared to show signs of recovery because it was generally felt by investors that uncertainties in the U.S. economy, and on a global level, had been solved, for the time being.

A debt relief program works like this: The government guarantees the debt that a company owes (mostly to financial companies), taking control of the company in trouble. It is not an outright loan.

In November 1997, the Bank of Korea’s foreign reserves were hitting bottom. The Korean government had to request a loan worth $19.5 billion from the International Monetary Fund to keep bankruptcy at bay.

During the late 1990s financial crisis, dubbed the IMF era here, many companies went bankrupt and many people lost their livelihoods.

The government used the loan to pay off debts of Korean companies in trouble.

In return Korea’s economic policy had to fall in line with IMF conditions.

Other than the loan from the IMF, the Korean government issued numerous bonds to help ailing financial and private companies.

However, the government only rescues companies that have a huge influence on the nation’s economy or companies whose business is vital to national security, such as defense projects and electrical power.

It doesn’t bail out every company that is in trouble; that would not be realistic.

For example, the U.S. government provided debt relief to Lockheed, an aircraft manufacturer, and Penn Central, a U.S. transportation company, in the early 1970s.

In the late 1970s, Chrysler, the automobile manufacturer, also got debt relief.

During the financial crisis of the late 1990s, the Korean government helped out Daewoo Group and Hyundai Group because of their significance to the national economy.

The government intervened in the selling of Daewoo Shipbuilding and Marine Engineering because it has a huge stake in the shipbuilder, having provided relief in the past.

Naturally, there is fierce debate over which companies should get financial help from the government during dire economic times.

Another issue is that companies might not pay back funds expended.

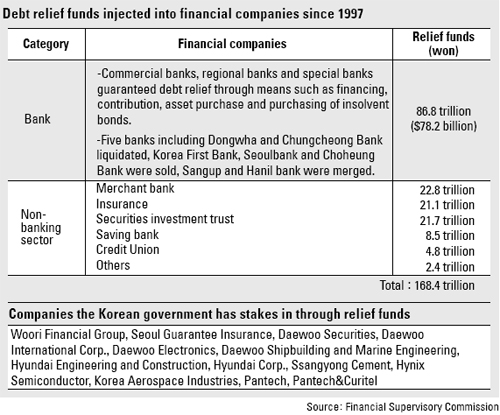

Since 1997, the Korean government has poured 168.5 trillion won to bail out financial and non-financial companies.

But since the end of June this year, only 91.7 trillion won has been recouped.

A certain amount of loss is inevitable since many companies go bankrupt despite a government bailout.

There are arguments that claim debt relief programs undermine the very foundation of a free market economy. The market functions on the assumption that companies take responsibility for their own finances.

It is possible, critics say, that companies might become reckless if they think that every time they run into financial difficulties the government will come running with a generous bailout package that the company can use to set its house in order.

A similar argument has surrounded the rescue of the two mortgage giants, Fannie Mae and Freddie Mac.

The U.S. government recently decided to provide a financial lifeline to the two.

Both were originally public companies under the U.S. government.

Fannie Mae, which was established in 1938, was privatized in 1968. Freddie Mac, which was born in 1970, was privatized in 1989; both continued to have government backing.

Because the companies were formerly state-run institutions, it was easy for them to draw capital and received tax benefits.

A comparison can be made with Korean companies.

Posco, Korea Electric Power Corp. and KT&G were listed on the stock market after they were privatized.

But all three still retain strong characteristics of public companies.

Fannie Mae and Freddie Mac both had a similar role to play in the United States.

Home buyers visit banks and companies specializing in mortgage loans to borrow money. Therefore banks and mortgage loan companies need substantial financial resources.

The two mortgage giants buy mortgage loans from private banks and mortgage companies, making them the biggest actors in the U.S. mortgage market.

However, after the U.S. Federal Reserve raised interest rates, the interest payments that home buyers needed to pay went up.

With the U.S. economy slowing down, real estate prices started to fall. As a result, the number of people who couldn’t afford to pay the interest - let alone the principal on mortgages - started to increase.

As the unpaid interest and principals on mortgage loans started to accumulate, the number of mortgage loan companies that were turning insolvent started to grow as well.

This situation affected Fannie Mae and Freddie Mac, which had lent money to private banks and mortgage companies.

It is yet to be seen whether the relief program to save the mortgage giants will break the chain of such financial insolvency.

By Kim Jun-hyun JoongAng Ilbo [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)