What is a microcredit loan, and how does it work?

Bank personnel discuss loans at Samsung Smile Microcredit Bank, which was established by contributions from Samsung Group. [JoongAng Photo]

In Korea, microcredit is often called miso geumyung, which literally means “smile finance.” Here, microcredit targets the poor, especially those who have low credit ratings.

Why do these people have low ratings? Why do they need microcredit? Well, let’s find out.

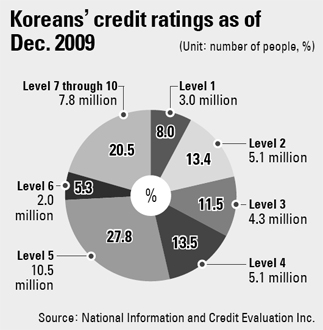

If your parents borrow money from banks or use credit cards, eventually there will be records of whether they have paid back the loans or repaid the credit card companies. The records are compiled by credit rating agencies. These agencies rate people’s credit-worthiness from 1 to 10, with 1 being the highest rank. According to the National Information and Credit Evaluation Inc., 37.8 million Koreans had credit ratings as of last year. The most common rating, shared by 10.5 million people, was 5. If these people continue to work, pay back their loans and make credit card payments, their credit ratings will improve. If they don’t, their ratings will fall.

If your credit rating falls to 7 or below, you will not be able to get a bank loan. You are considered “unbankable.” As of last year 7.8 million Koreans, or 20.5 percent of the people with credit ratings, were unbankable. Without the ability to get a commercial bank loan, unbankables have to rely on capital companies or savings banks. They pay a high price: Commercial banks charge 6 to 8 percent annual interests on loans, while savings banks charge 20 to 30 percent.

The interest rates are higher for people with low credit ratings because there is a higher chance that these loans won’t be repaid. According to the National Information and Credit Evaluation Inc., only 0.14 percent of those with the level 1 rating failed to pay interest or principle on their loans in a three-month period as of 2008, a mere 14 out of 10,000.

In contrast, 56.4 percent of the people with a level 10 rating failed to pay. Banks charge high interest rates to unbankables to make up for the ones who don’t pay back their loans.

And some banks simply don’t lend to people with low credit ratings. Savings banks were founded to help the poor but in fact they do not extend much credit to low-income households.

In 2003, the country went through the so called “card crisis.” Many credit card users were unable to make payments and a large number of credit card debts went bad. Since then, financial institutions have been more reluctant to extend loans to the poor. Instead, they focused their business on mortgage loans. Mortgages are low-risk because the home and property are collateral: The bank can take the house if the borrower fails to pay.

Lending was also affected by the financial crisis that started in September 2008. Job growth has stagnated and the economy dipped. Financial institutions cut back on loans. Thus, low-income households without collateral found it even harder to borrow.

As a result of all these factors, people with low credit ratings go to private lenders. Under the usury law, private lenders cannot charge more than an annual interest rate of 49 percent and most charge just that. This means that if someone borrows 1 million won ($886), he would have to pay 490,000 won in interest. This is really burdensome. With such high interest rates, private lenders make a lot of money. A large private lender in the country made more than 100 billion won in net profit last year.

The government amended the usury law, lowering the maximum annual interest rate to 44 percent beginning in June or July. It plans to lower the rate to 39 percent within this year.

The government believes that high interest rates hurt low-income households. Those who have delayed repayment of loans or payment for their credit card spending for three months or longer are blacklisted by financial institutions and unable to do any financial deals such as new borrowing or getting a new credit card.

However, if low-income families can borrow at a reasonable interest rate, things can change. Those who need money urgently can take out loans rather than relying on loan sharks. Those who want to start a business can borrow. If they succeed, they can join the middle class.

If the country’s middle class grows, the economy will improve. That’s why the government, companies and banks contributed a large amount of money to establish microcredit finance businesses.

However, even microcredit banks do not extend loans to everybody. If people don’t pay their loans, the amount of money they can lend will be depleted. To obtain loans, potential borrowers need to have at least some ability to pay it back.

By Kim Won-bae [jbiz91@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)