Fintech: a new frontier in banking and finance

“Fintech, which emerged as a new financial model that converges finance with information technology, will shake up our existing financial industry and will settle as a new growth engine for the nation’s economy,” Financial Services Commission Chairman Yim Jong-yong said during a financial industry job fair held at COEX in southern Seoul late last month.

The expansion and development of fintech has been one of the key reform measures that the Financial Services Commission has been pushing since 2015, especially as many conventional financial institutions are struggling from dwindling profitability caused by record-low interest rates, lukewarm local stock markets and unstable global markets.

Korea’s fintech has gone through rapid changes since December 2009, when Hana Bank launched the country’s first mobile banking app just months after the first iPhone developed by Apple landed on our shores.

In the past two years, leading Korean banks have been aggressively jumping into fintech, with a particular focus on mobile banking services.

Woori Bank was the first financial institution in the country to introduce a mobile banking service that allowed users to apply for and receive loans completely in the app. The loans offered through Woori’s WiBee Bank app had so-called midrange interest rates aimed at small businesses. Since launching last May, the bank has lent out 120 billion won ($105.75 million) through the app.

Shinhan Financial Group quickly followed with Sunny Bank in December and one-upped Woori by letting users open a new account without having to physically visit a bank branch. The app also allowed users to apply for midrange-interest loans.

In just six months, Sunny Bank now has roughly 700,000 subscribers. One of the app’s most popular services is foreign exchange, where an estimated 370 billion won has been converted, comprising about a quarter of the bank’s overall foreign exchange transactions.

Shinhan Financial Group, the bank’s parent company, is going beyond just providing mobile banking services. It is the first in the industry to run a fintech cooperation program called Shinhan Future’s Lab. Launched last May in partnership with global consulting company Accenture, the program provides support including financial loans, consulting and mentoring to fintech start-ups with potential. The idea is to build a cooperative relationship with start-ups instead of simply investing in the companies.

Rival KEB Hana Bank introduced its 1Q app in February this year. An expansion of an app it had first released in 2009, the 1Q app lets users open accounts and make payments.

Most notably, 1Q was the first Korean mobile banking app to be offered in China in May. The services cater exclusively to Chinese customers such as those related to Korean medical tourism, as many tourists from China visit Seoul for medical services.

Kim Jung-tai, chairman of Hana Financial Group, the parent company of KEB Hana Bank, has shown interest in applying the latest technology to the company’s financial services. His ambitions include expanding overseas.

Hana’s merger last year with Korea Exchange Bank was part of those efforts. The newly formed KEB Hana Bank now has the largest number of overseas branches among leading Korean commercial banks, and its operations abroad contribute significantly to the financial group’s banking business. Last year, KEB Hana made $176.4 million from its overseas businesses, accounting for roughly 18 percent of its overall net profit.

Hana Financial Group has also been increasing its cooperation with fintech start-ups. Since June last year, the company has been running a program called 1Q Lab, named after its mobile app, offering office space, legal advice and mentoring to start-ups.

“Bank transactions that don’t go through a teller now make up 90 percent of all transactions, and mobile banking now exceeds internet banking, which shows the rapid changes of customers’ digital technology needs,” a Hana spokesperson said. “There is a need to satisfy the demands of customers through innovation and convergence between finance and IT.”

Another major financial institution, KB Financial Group, though late to join the game, introduced its Liiv KB app in June, offering new conveniences for users such as a feature to split restaurant bills between friends.

State-run banks, too, are jumping on the fintech wagon. The Industrial Bank of Korea is cooperating with start-ups through its incubator program Dream Lab. In particular, the bank has been connecting promising companies with crowd-funding.

One major concern stemming from fintech has been security, and the need to verify customers’ identities without human interaction has spawned all sorts of innovative authentication measures from financial institutions.

KEB Hana Bank was the first among its competitors to verify users’ identities through a smartphone iris scanner, a feature taken straight from science fiction. Woori Bank and NH Nonghyup Bank have made it possible to log in to their apps through smartphones’ fingerprint scanners.

Perhaps one of the most daring security features is Shinhan Bank’s ATM hand scanner. Last December, the bank was the first to install technology in their ATMs that can log users in by examining the veins in the palm of their hands.

Cho Yong-byoung, president of Shinhan Bank, said the new biometric verification method could allow 90 percent of the work normally handled at a bank window to be done at an ATM. This means customers could potentially do more at the machine than just withdraw and deposit cash after a bank closes.

All these developments in fintech come at a critical time, as banks and securities firms have been seeing profits shrink on the back of a record-low key interest rate. The net profit of local commercial banks has been falling in recent years, from 8.7 trillion won in 2012 to 3.5 trillion won last year. Returns on assets and returns on equity, which are used as indicators for banks’ profitability, are at 0.16 percent and 2.14 percent, the lowest since 2000.

As a result, financial groups have been undergoing major restructuring including reducing the number of brick-and-mortar branches. The top five banking groups closed 260 branches between 2012 and 2015 and brought the total number of branches down to 5,096 at the end of last year.

That figure has since further dropped to below 5,000, after banks closed 127 branches in the first half of the year.

“When the profit made from interest rates is shrinking rapidly, the business models are changing fast in order for survival,” said Kim Hye-mi, a senior researcher at the Hana Institute of Finance.

Even with all these innovations, there is still a long way to go for Korea, considering that banks only just started to pick up on the fintech wave a few years ago and some countries like China are already leagues ahead.

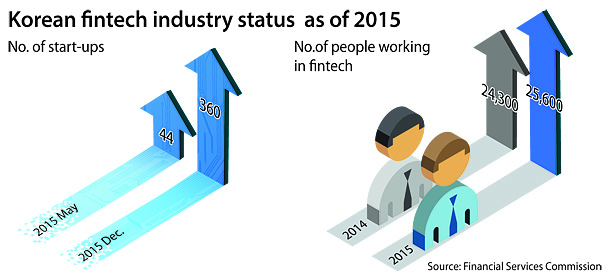

The Financial Services Commission estimates there are 360 fintech start-ups in Korea as of last year. Although it’s an increase of more than 700 percent from 44 companies in the first half of last year, it still falls behind China, whose fintech industry has grown at an exceptional rate.

According to McKinsey, China’s internet finance has already exceeded other markets by number of users and amount spent. At the end of last year, the market reached $1.8 trillion. This is remarkable growth, considering China only jumped into the fintech business in 2011 and digital payments in 2012 only totaled $793 billion.

“It’s amazing how you don’t even need to carry around a plastic card and all you need is your smartphone to make payments,” said an employee of a Korean game company who lived in Shenzhen, one of the leading cities for IT in China. “Compared to fintech utilization in Shenzhen, Korea is still far behind.”

The country’s financial institutions are now playing catch-up. Shinhan’s credit card affiliates launched a Mobile Platform Alliance to expand its current service offerings to nonfinancial ones, such as providing information on public transportation, car sharing, convenience store discounts and designated driver service. The financial group said it has already signed a partnership with 20 companies and plans to double that figure by the end of the year.

“The idea is to converge the financial business with other nonrelated businesses,” a Shinhan Financial Group spokesperson said.

KB Financial Group has focused on expanding its fintech services by investing in Kakao Bank, which will go into service early next year. The collaboration between a major financial institution and operator of KakaoTalk, the country’s most widely used messaging app, is expected to provide customers with a wider choice of financial products.

“Inevitably, fintech will bring huge changes not only to the financial and tech industries but also the very core of our lifestyle,” said Jung Yoo-shin, a Sogang University professor who also heads a fintech center that launched in November last year.

The professor noted that innovations in biometric security are one part of the change, but the real shifts will come in the way we conduct financial affairs. Banks will no longer have exclusive dominance on deposits and loan services, Jung said, while tech companies will rise as a strong competitor.

“The fintech industry is about who creates the platform, and competition will become fierce, as it hasn’t officially taken off in any country yet including in Korea,” Jung said. “It is still open season.”

BY LEE HO-JEONG [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)