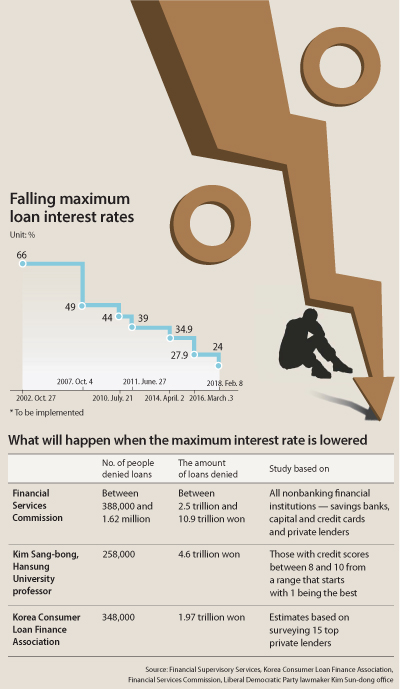

Up to 1.62 million loan seekers may be denied

This is almost as much as the 1.82 million who already have such loans, 1.25 of whom took them out last year.

Nonbanking institutions include savings banks, credit card companies, capital firms and private lenders. Savings banks, which in Korea are more like consumer finance companies, cater to low-income, bad-credit borrowers.

But other estimates have been more conservative. Kim Sang-bong, an economics professor at Hansung University, said at least 258,000 will be denied loans, while the Korea Consumer Loan Finance Association, in surveying the top 15 private lending companies, came up with an estimate of 348,000 denials due to the maximum legal interest rate being lowered, a figure that will go up when private lenders fold or shrink.

During his election campaign, President Moon Jae-in promised to lower the legal maximum loan interest rate to 20 percent to ease loan burdens for people with low credit scores, a move the loan industry has been opposing, but for now, the government has settled at 24 percent, a decision that was passed during a cabinet meeting at the end of last month.

The lowering of the interest rate has come two years after the previous Park Geun-hye government in March lowered the maximum rate to 27.9 percent. Since 2002, after the law was revised, the maximum legal loan interest rate has been falling from 66 percent. The first change came after the interest rate was lowered to 49 percent in October 2007, and since then it has been lowered 3 to 7 percent every nine months to three years.

The nation’s key interest rates have remained at their lowest ever, 1.25 percent, for almost a year and a half. Since the Bank of Korea has kept the nation’s key interest rates low, private lenders have room to further lower their own interest rates on loans.

But the situation has been turning around with the Korean central bank under pressure to raise interest rates amid a steady recovery of the nation’s economy, which is expected to post 3 percent annual growth by the end of this year. There are already expectations building of a rate hike as early as this month.

“The industry will be faced with double the problems if the key interest rates are raised while the interest rates on loans are forced to be lowered,” said Lee Jae-sun, secretary general of the Korea Consumer Loan Finance Association. “Loans supplied by private lenders will be undeniable, but the issue will be how much it will shrink.”

Some of the nonbanking financial industries are already under pressure by the government to lower their loan interest rates. One of these is the credit card industry.

Currently the interest rates on loans borrowed from credit card companies, including cash services, is around 15 percent. For late payments, the interest rates that the credit card companies impose are between 23 percent and 27.9 percent, the current maximum limit.

In the case of Shinhan Card, when the person borrows a loan with an interest rates of 17.9 percent or lower, it imposes a 23 percent interest rate when that payment is a month late. But that rates goes up to 23.5 percent when it is three months late, and 24 percent when it is more than 3 months late.

For a loan with an annual interest of more than 20.1 percent, a 27.3 percent interest rate is imposed when the return of the loan is late for a month. That rate goes up to 27.6 percent when it is late for three months, and then to the maximum 27.9 percent.

The government is hoping to lower the initial interest rates on loans to 10 percent. If it does, late-payment interest rates will also be lowered. Most of the people who use credit card loans have unfavorable conditions, such as low credit scores or multiple loans.

According to the Financial Supervisory Service, as of the first half of this year the balance on loans borrowed from credit card companies amounts to 24.4 trillion won ($21.5 billion). Those who borrowed from multiple loan borrowers with three or more loans accounts for 60.9 percent, or 14.9 trillion won.

“Although the Financial Supervisory Services has not yet come up with a detailed guideline, the fact that they are looking into how interest rates on loans are set is interpreted as telling the credit card companies to lower their interest rates,” said a credit card company official, who spoke on the condition of anonymity. “Each credit card company is currently analyzing how much profit will be lost when lowering both the initial interest rates on loans and overdue interest rates, as well as how many people will be denied under the tougher loan evaluations.”

As it has become tougher to get loans from financial institutions, there are concerns that those with lower credit scores will turn to illegal lenders. The government hopes to prevent such effects and is working on measures scheduled to be announced next month.

One of the major measures that the government is looking into is tightening surveillance and investigations against illegal lending, while also planning to expand the policy finance provided by state-owned financial institutions for those with low credit scores who are denied loans by private financial firms.

In 2010, Japan lowered its maximum legal interest rates from 29.2 percent to 20 percent. Although the actual implementation of this had a grace period of three and a half years, it resulted in many of the major private lenders shutting down businesses while those with low credit scores flocked to illegal lenders. As a result, the Japanese government forced the four major financial holding companies to take over the major private lenders. Recently, major Japanese banks have been offering loans to people with low credit scores with a 15 percent interest.

“One of Korea’s strengths is that the nonbanking financial industry is better developed than Japan’s,” said Jung Hee-soo, a researcher at Hana Institute of Finance. “We need measures where nonbanking financial companies expand loans to those with low credit ratings, as well as raising the support of government-led loan policies.”

The loans that the government will be offering, however, will be limited to those with an annual income of less than 35 million won. But those without jobs or those with overdue loans will be ineligible.

BY HAN AE-RAN, JUNG JIN-WOO AND LEE HO-JEONG [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)