Life after retirement proves long and difficult

The bank polled 20,000 of its customers aged 20 to 64 about their finances between September and October last year with the hope of using the data to better serve its clients in financial consulting and wealth management.

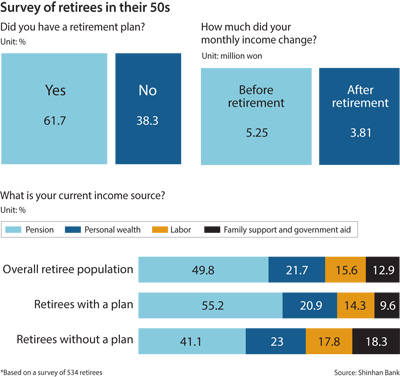

Among the findings: 61.7 percent of retirees in their 50s were prepared for retirement while 38.3 percent were not; parents spend an average 85.5 million won ($80,000), including on private tutoring, to educate a child through high school; and college graduates have to work on average at least two years as a salaried employee in a company before earning 2 million won a month.

The results paint the picture of a retiree population in dire straits. Among 534 retirees polled, many of them hoped to work until they were 59, but in reality, the average age of retirement was 56. Among those who planned out their retirement, only 24.4 percent said they retired at the time they expected.

Once leaving work, their monthly income dropped significantly from an average 5.25 million won to 3.81 million won. A majority of them, 56.1 percent, said they experienced months where their income could not cover their expenses, with nearly 60 percent of those who didn’t plan their retirement saying this was the case compared to 53.9 percent of those who did plan.

The report noted that many retirees also underestimate their expenditures. The average retiree expected to spend 2.19 million won a month but in reality spent 2.61 million won a month.

And regardless of whether retirees planned their retirement, many still rely on pension payments. For those who did not plan their retirement, 18.3 percent of their monthly income comes from family and government support, compared to 9.6 percent for those who planned.

By Shinhan Bank’s estimates, a retiree with personal wealth of 493 million won and monthly expenses of 2.19 million won will dry up their savings in 18.7 years. For most people, that means they will run out of funds before they die. According to Statistics Korea, as of 2016, the average life expectancy of a Korean man is 79.3 years and for a woman, 85.4 years.

Aside from retirement, education expenses for children have also gone up, according to Shinhan Bank. The average family spends 85.5 million won - 64 million won toward private tutoring - for a single child to get through high school. For that child to have a chance at higher education, add another 14.5 million won to bring the total to 100 million won.

The trajectory of that spending is parabolic. For toddlers, the average monthly expense on education is 120,000 won. That increases to 180,000 won in preschool. When the child enters elementary school, the monthly expense goes up to 300,000 won. In middle school, it becomes 410,000 won, and by the time the child is in high school, spending is at 470,000 won per month.

But even a college degree does not guarantee a job. According to Shinhan Bank, the average age at which recent graduates land their first job is 26.2, up from 24.3 in 2006. The average age has remained at the same level since the 2008 financial crisis.

Getting full benefits with the first job has also become more difficult. In 2006, 83.4 percent of people in their first jobs were employed as so-called regular workers, the category of employment in Korea that comes with the most benefits and job security. The figure has fallen to 60.5 percent.

It now takes at least two years for a regular worker to reach a monthly salary of 2 million won. In the first year of employment, 59.5 percent of regular workers took home 1.71 million won a month. In the second year, 77.4 percent made 2.05 million won, and in the third, 79.4 percent reported 2.18 million won in monthly pay.

But because of high living costs and debt, there’s not much left for young people to save let alone invest. According to Shinhan Bank, people in their 20s and 30s employed in the last three years made an average 1.99 million won a month, of which 1.06 million won was used for living costs, 220,000 won covered debt and 710,000 won was saved or invested.

Among people in their 20s and 30s, 47.4 percent said they were in debt and 33.1 percent said they were receiving financial support from parents or other family members.

One of the biggest changes last year was the increasing number of people opening their own businesses largely thanks to lower start-up costs.

While entrepreneurs in their 30s accounted for the majority in 2006 at 43.1 percent, their portion has since gone down to 29.5 percent, eclipsed by those in their 20s who have increased their share to 34.4 percent from a previous 24.8 percent. Older people are becoming active entrepreneurs, with 13.4 percent of business owners over the age of 50 compared to just 5.2 percent in 2006.

The average amount spent on opening a business has gone down from 94.5 million won in 2006 to 81.4 million won as more people are pursuing smaller ventures.

BY LEE HO-JEONG [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)