Bridging the generation gap

She had placed around 10 million won ($9,266) in a fund product for four years until 2014, but the return accrued was only 100,000 won, a meager 1 percent of her investment.

“I thought that’s not the right way to invest. I pulled out the money and enrolled in a pension insurance product in preparation for life after retirement,” Kim said.

Kim knew that the average return ratio of the product was not that handsome, at around 3 percent, but she was attracted to the investment because she would be guaranteed payment at a specific age.

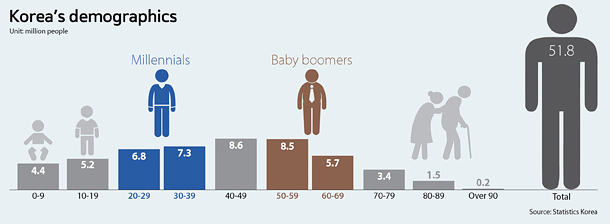

Kim is among the eight million baby boomers born between 1955 and 1963 after the Korean War, most of who have now reached or are nearing retirement age. The way boomers in their 50s and 60s spend and invest is shifting as they near retirement.

While baby boomers are leading a change in consumption patterns, the rise of so-called millennials - people born between 1981 and 1996 - is also changing the way people spend. Millennials, the sons and daughters of baby boomers, were brought up in a far more prosperous country than their parents. They tend to be highly educated and tech savvy, and just like their peers in other countries, they tend to be less inclined to follow existing social norms, including getting married and having children.

The different environment that millennials grew up in and their different interests make their spending habits and asset management noticeably different and distinctive from older generations.

Ready for retirement

Many industry insiders say that the game-changer in finance will be financial products targeting those at or approaching retirement, given the high proportion of retirees and the country’s weak national pension system. The shift is already evident in the financial asset portfolios held by Korean households.

Savings used to be the most common and popular option for managing money, but low interest rates have turned people away. In 2013, the share of pension and insurance products surpassed savings, including installment savings, in households’ financial assets for the first time, according to the Bank of Korea.

The popularity of pensions and insurance continued to rise as longer-term investment options accounted for 24.3 percent. The figure jumped to 31.8 percent in 2016, according to the Bank of Korea.

“As the population ages, demand for insurance and pension products will keep on rising, because they help people manage assets in the long term,” said Yoon Kyoung-soo, senior economist at the central bank’s financial stability analysis team.

Assets held as pension savings hit 128 trillion won in 2017, up 8.6 percent over a year earlier. Pension savings include insurance, trust funds and pension funds.

The shifting investment appetite among boomers partly stems from the weak social safety net in Korea. The average pensioner gets 330,000 won per month from the National Pension Service, far below the minimum living expense.

Besides the poor benefits, the system lacks sustainability.

“All four pension schemes - the national pension, government employees' pensions, military personnel pensions and private school teachers' pensions - are likely to face financial trouble in the near future,” said Moon Hyung-pyo, senior research fellow at the Korea Development Institute

“This imbalance between low contributions and high benefits makes the whole system financially weak and vulnerable,” he said.

This is why the poverty rate among older people in Korea is the highest among OECD member countries, with almost half of senior citizens in poverty. Many of those in their 40s and 50s are pushed out of their jobs at conglomerates and resort to manual labor or self-employment.

Those in their 50s and 60s also prefer real estate assets because property can serve as security for loans and monthly rent.

Boomers are also highly visible in the mortgage market, taking on more debt in order to own one or more properties.

People in their 50s are the largest force, at 46 percent, in the mortgage market, according to Park Choon-sung, a researcher at the Korea Institute of Finance. In the survey in 2016, those in their 30s accounted for 19 percent.

“The older age group thinks that buying property is a safe bet to grow their nest eggs,” said Park.

“Lower interest rates also contributed to reducing the appeal of other options like saving and making lending rates more attractive.”

While boomers are incentivized to prepare for their retirement, they might find it hard to secure enough money based on their spending structure.

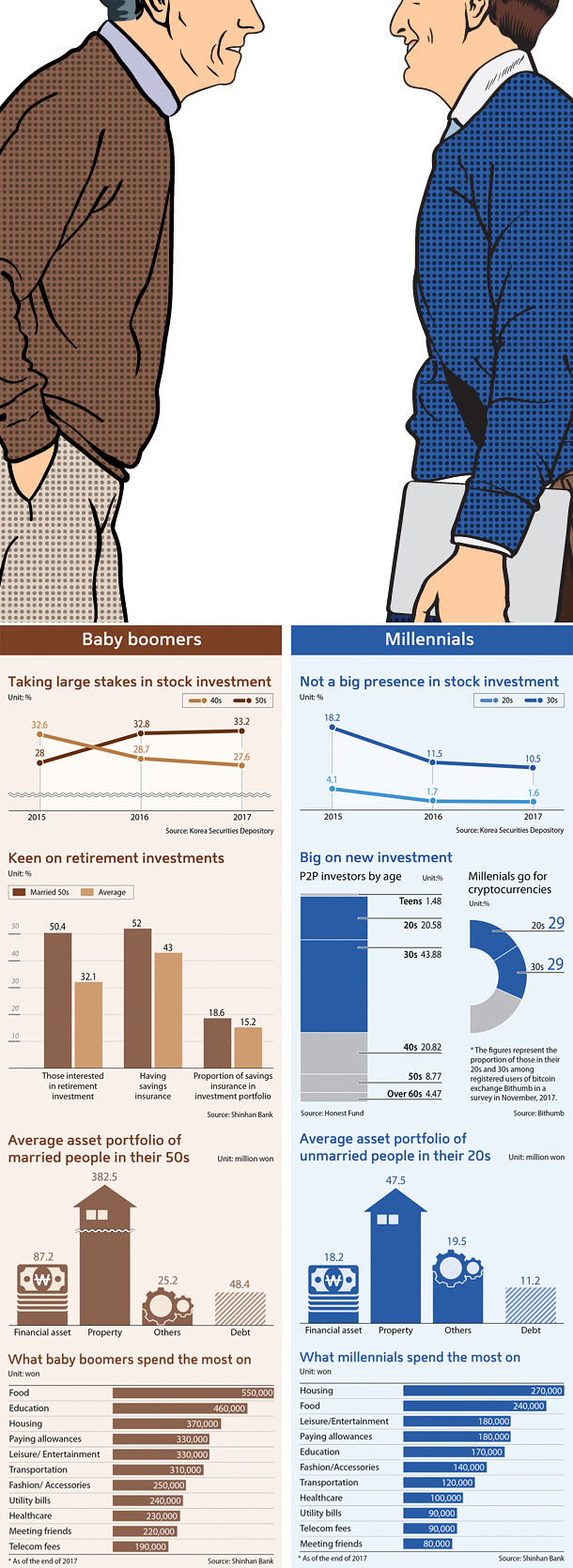

A large portion of monthly expenditure of those married in their 50s is devoted to supporting children and elderly parents, according to a report published by Shinhan Bank, as many baby boomers are the main earners among parents and children with limited income.

The surveyed 50-somethings spent 460,000 won on education in 2017, the second highest expenditure after food. Giving allowances to parents and children came fourth at 330,000 won after housing fees at 360,000 won.

Mirae Asset Retirement Research Institute found earlier this month that 73.3 percent of people in their 50s and 60s live with children aged over 20 and 87.5 percent have experience of financially supporting them.

In a survey released earlier this month, 44.6 percent said they regularly give pocket money to their parents, while 28.4 percent occasional support their parents.

But this doesn’t necessarily mean that boomers' lives are all about sacrifice.

Baby boomers tend to spend more on leisure and cultural activities compared to people in their late 60s and early 70s, according to a report by the Korea Institute for Industrial Economics & Trade.

“Baby boomers think of retirement as a new chapter in their lives, a different approach from the previous generation,” the report noted.

“They are willing to map out new plans and make them happen.”

Korea’s millennials opt to avoid traditional investment options such as stocks and funds due to a lack of budget and the perception that bigger players such as foreign investors and older, high net wealth individuals have an edge over them. They are keen to venture into relatively new investment options such as peer-to-peer financing and cryptocurrency trading.

Their share in the stock market is minor compared to those in their 40s and 50s and has shrunk recently. People in their 20s accounted for 4.1 percent of investors on the main bourse Kospi and the junior Kosdaq in 2015, but their share shrank to a mere 1.6 percent in 2017. Those in their 30s took up 18.2 percent in 2015, but that figure fell to 10.5 percent in 2017.

People in their 40s and 50s take the lion’s share, with 50-somethings accounting for 33.2 percent and 40-somethings at 27.6 percent.

“The major client base at securities and asset management companies is people aged between 40 and 50,” said a source at Mirae Asset Global Investments, the country’s largest asset manager.

“On the other hand, young people don’t appear to take an interest in investment since they are minor players at brokerage and investment companies,” the source said.

General distrust in the Korean capital market is also a factor.

“A series of scandals involving short-selling and internal trading ruined the reputation and transparency of Korea’s capital market,” said Nam Ki-nam, a researcher at the Korea Capital Market Institute.

Kim Hee-yeon, a 31-year-old working in the marketing division at a tech firm, echoes the sentiment. She shies away from traditional investment and funds, but manages 8 million won through Peer-to-Peer (P2P) investment.

“Young ordinary investors like me can’t turn a profit in the stock market because we have less time, money and market information,” she said. “The timing of buying and selling is critical, but we can’t just sit watching our mobiles to check the prices,” she said.

But younger investors do want to do something with their money, with relatively new investment options such as P2P financing and cryptocurrency trading proving especially popular with people in their 20s and 30s.

Honest Fund, a major P2P platform operator, said that people in their 30s make up the bulk of its user database, accounting for 43.88 percent. Those in their 20s also took up a large portion at 20.58 percent, following users in their 40s at 20.82.

On the other hand, boomers have a weak presence since the combined share of people in their 50s and 60s is less than 15 percent.

“It seems that young people like the fact that the whole process can be done online, and you can start with a small amount of money,” said a spokesperson at Honest Fund.

Kim also invested about 8 million won through a P2P provider called Lendit.

Borrowers are directly paired with lenders through online and mobile marketplace platforms, and lenders get a share of the interest charged to borrowers.

Younger consumers led the bitcoin boom in Korea, making the country one of the top three most active cryptocurrency markets in the world.

Bithumb, a leading cryptocurrency exchange in Korea, said that more than 50 percent of its users are those in their 20s and 30s.

While baby boomers have a distinctive propensity to buy properties, millennials don’t seem that interested.

“Baby boomers prioritize houses and property. Traditionally, they were considered a safe and essential asset,” said Ha Joon-kyung, an economics professor at Hanyang University.

“But buying a house doesn’t carry such weight among younger people, putting aside the fact that they don’t have enough money to make the purchase.”

In baby boomers’ asset portfolios, real estate accounted for 382.5 million won on average in 2017, the top asset, while financial assets were worth 87.2 million won, according to Shinhan Bank.

The average value of real estate shrinks to 47.5 million won for unmarried people in their 20s.

Millennials also take a different approach to spending.

Researchers say the generation is heavily focused on themselves and the experiences that define them - and are compelled to share those self-validating experiences.

Samsung Securities summed up the tendency as “YOLO spending”, citing the acronym that stands for “you only live once.”

“Millennials are found to spend generously on products and services designed to entertain - such as games, drones and tourism,” said a Samsung Securities report released in February.

Going to fancy restaurants and buying desserts, cosmetics and IT products are cited as items millennials consider valuable enough to spend generously on.

In a survey by Shinhan Bank, unmarried people in their 20s spent an average 240,000 won a month on food, the second highest category in their monthly expenditure, and 180,000 won on leisure and entertainment, the third highest category.

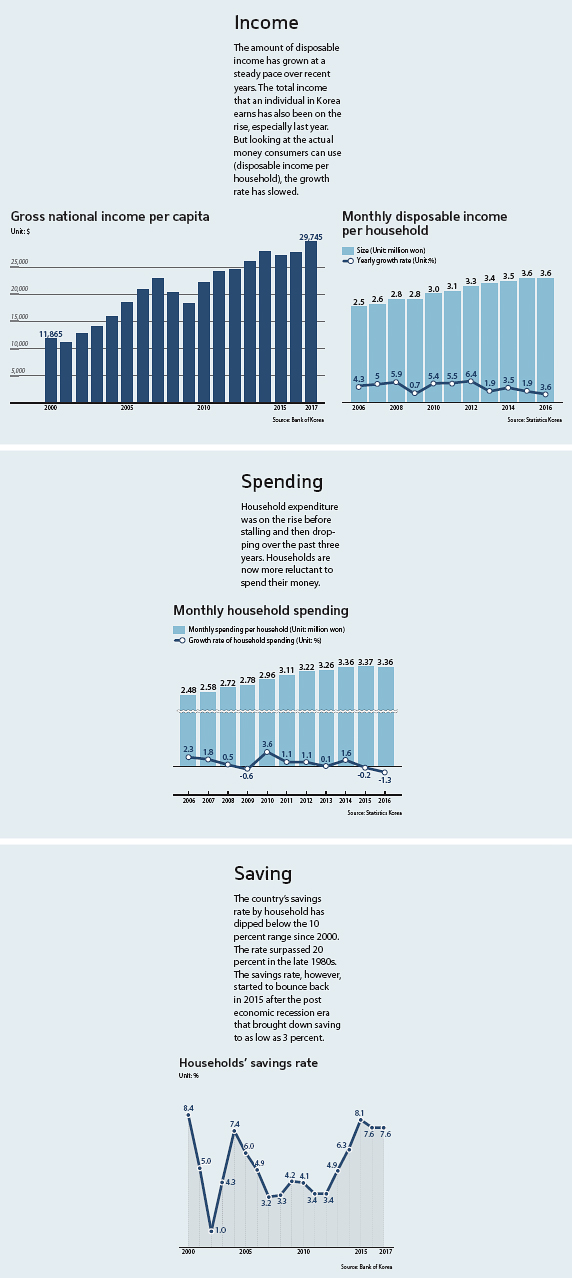

Korea’s economy has expanded over recent years as gross domestic product and per capita income have been on the rise.

News reports have hailed the country’s national income per capita - expected to cross the $30,000 mark this year - as evidence that Korea is entering the ranks of truly developed economies. Different income indicators show steady growth over recent years.

But many people - especially in the low- to mid-income bracket - struggle to see the apparent progress reflected in their daily lives because the amount of money that they can actually use at their discretion remains stagnant.

The growth of monthly disposable income per household has slowed since 2015, according to Statistics Korea. Household disposable income grew 3.5 percent in 2014 over a year ago, but the rate stalled in 2015 at 1.9 percent and further shrank to 0.7 percent in 2016.

Experts see the tepid growth of disposable income as linked to the increase in fixed spending - interest for mortgages, pension contributions and taxes - which outpaces disposable income.

“The reason why consumption has been on the decline is the increasing cost of pensions, taxes and other expenditures related to the social safety net,” said Byun Yang-gyu, a former researcher at the Korea Economic Research Institute who now works at Kim & Chang law firm.

The savings rate recently rebounded after stagnant growth.

In the 1970s, the country’s spending rate surpassed 30 percent, but it has since fallen in line with other developed countries. The rate hit a low point in 2007 during the global economic recession, but has bounced back to 7.6 percent.

“The recent increase in saving appears to be related to demand for real estate,” said Kim Hyung-suk, a senior economist at the Bank of Korea.

“People tend to save more money when they hope to buy a house, but now that the government is trying to slow down the housing market, the rate will likely remain stagnant.”

BY PARK EUN-JEE [park.eunjee@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)