Korea’s fintech start-ups set sights abroad

Financial Services Commission (FSC) Chairman Yim Jong-yong will bring as many as 10 fintech firms to London in July to demonstrate the nation’s cutting-edge technologies to globally renowned financial institutions.

Before that, the first overseas Demo Day events will take place in Singapore and other Southeast Asian countries in June.

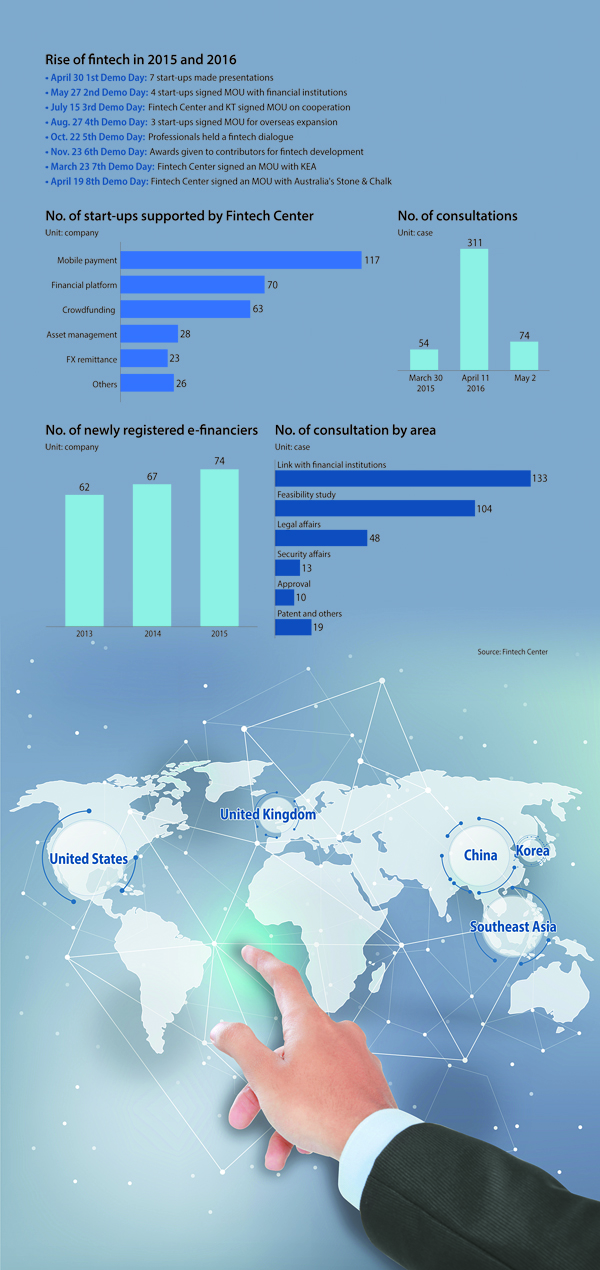

Demo Days offer fintech start-ups the chance to show off their technologies and services for officials at major financial companies and give them chances to attract investors. The eighth such event was held last week.

The FSC is also planning to hold Demo Days in the United States and China this year.

“The key words in the emerging fintech industry will be robo-advisers, big data and global expansion this year,” said Yim at a ceremony held to mark the first anniversary of the launch of the Fintech Center in Pangyo, Seongnam in March. “We will help local fintech firms go abroad. The FSC will hold Demo Days in fintech hubs like Southeast Asian countries, Britain, the United States and China this year.”

Experts point out overseas expansion is the basis from which small companies can become global giants.

“The domestic market is too small, and the government shouldn’t force start-ups to compete with each other for ‘rice balls’ in a limited market,” said Jung Yoo-shin, a professor of information technology (IT) and finance at Sogang University and head of the Fintech Center. “From the very beginning, local start-ups need to go abroad and compete like Israeli start-ups do.”

The global start-up market is growing as mobile technologies evolve and Internet access becomes more prevalent, Jung said, and Korean firms can discover a world of opportunities outside their own country.

“It is true that overseas expansion is necessary,” said Lee Seung-gun, CEO of Viva Republica and chairman of the newly launched Korea Fintech Industry Network Association. “But it is hard for companies with no track record of success at home to get recognition in other countries.”

China should be used as a benchmark when it comes to fintech success, experts say.

“China is four to five years ahead of us in fintech,” Lee said. “It is a financially advanced country, outstripping Korea in every sector because the regulatory environment is really different. The government lifted almost all regulations for fintech.”

In the past, China had a relatively poor credit card payment system and fewer ATMs per person than Korea, according to Lee.

“Fintech firms filled that gap, and those ventures and existing financial institutions have naturally grown together,” Lee said.

National efforts to deregulate the market are what Korea needs now, he added.

China is home to more than a few world-class fintech giants.

According to the Leading Global Fintech Innovator Report 2015 by KPMG, big data-based insurance company ZhongAn is No. 1 on the list of the world’s 100 top fintech firms. Qufenqi, an electronics retailer that lets people pay in monthly installments and also offers micro-loans to students, is ranked fourth.

China is particularly advanced in big data technologies, and Korean firms that are planning to enter the Chinese market are advised to operate in other sectors like security and robo-advisory services.

“Because of its huge population, China excels in big data,” Jung said. “But they are weak when it comes to robo-advisory services. As the stock market tumbles showed early this year, they lack algorithmic investment tools. Korean makers of robo-advisers can keep an eye on the Chinese market, considering that demand will rise as long as its economy keeps growing.”

Top: FSC Chairman Yim Jong-yong, third from left, poses after signing a partnership between Stone & Chalk, an Australia fintech accelerator, and Korea’s own Fintech Center. Bottom: Developers of KTB Solution showcase their smart sign technology at Citi Mobile Challenge held in Hong Kong in December. [FINANCIAL SERVICES COMMISSION; CITI]

Fintech has been at the center of the FSC’s reform plans for Korea’s financial sector. As soon as the FSC decided to focus on the industry, it established the Fintech Center, where start-ups or entrepreneurs with technologies can receive professional consultation on the feasibility of their business or profit model. The center also helps connect start-ups with financial institutions for help getting funding.

“The FSC will spare no effort in raising the competitiveness of Korean fintech companies overseas,” the chairman said. “This year, our goal is to export Korean fintech services all over the world.”

For the past year, the Fintech Center has offered advice to as many as 320 firms.

In a survey last year, about 66 percent of the companies said they are satisfied with the center’s services.

“It wasn’t easy for us to meet people in charge of IT for banks or card companies before the center was established,” said Jeong Hee-suk, CEO of a small biometrics firm.

This year, to support more potential fintech entrepreneurs, the center will establish a Web portal that is tailored to searches for fintech-related information like statistics. It will also start supporting the mergers and acquisitions of firms as part of efforts to help expand the size of the industry.

The government-led initiative is leading to the creation of infrastructure for fintech. The Korea Fintech Industry Network Association was officially launched on April 25. As many as 108 companies participated in the launch as members.

“Our goal is to represent the fintech ecosystem and help it develop into a major industry,” said Lee. “We will help companies deal with regulatory issues and cooperate with banks and other financial institutions. For banks, we can help find really promising start-ups.”

Starting with the deregulation for crowdfunding in January, the FSC is going to loosen more rules this year to boost big data and robo-advisory services.

Still, the industry wants more.

“The regulation requiring that cards use integrated-circuit [IC] chips is hindering growth of new payment services,” said Kwon Hae-won, CEO of the mobile payment service Paycock, referring to the security chips embedded in most newly issued cards.

“All card-reading devices are required to be able to read the chips, meaning that eventually we will all have to use cards with the chips. But three years ago in Europe, IC technology was proved vulnerable to hacking.”

But some experts say that the government-backed initiative is actually hampering the development of the fintech firms.

“The government announces it will loosen one regulation out of hundreds of others, then replaces those regulations with guidelines it suggests companies follow,” said Kim Seung-joo, a professor of information security at Korea University.

“Every company that follows them ends up with similar services,” he added, arguing that the government should step back entirely and create a more open eco-system for development instead.

BY SONG SU-HYUN, KIM JI-YOON [song.suhyun@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)