Card firms say users will feel brunt

Owners of around 1,000 gas stations stage a mass rally demanding that the government force credit card companies to lower their handling fees. They also requested an end to the favoritism shown to gas stations run by Nonghyup and raised penalties for selling fake gasoline at the protest march in front of the government complex in Gwacheon, Gyeonggi, yesterday. [YONHAP]

As various parties dispute the legitimacy of credit card handling fees, which small businesses and restaurateurs say would still be unfairly high despite conciliatory proposals by financial companies to trim their margins, the latter are now subtly appealing to consumers to take sides.

The companies claim that any further lowering of the fees beyond what they have suggested in recent days would not only result in huge losses for themselves, but also a greater burden being placed on the shoulders of regular credit card users.

They maintain that the voices crying out to erode the fees are not taking into account the costs that go into operating a credit card services business. These, they contend, would end up being transferred to consumers if small businesses from gas stations to beauty parlors don’t pay up.

Rate not so high

In a post on social networking site Facebook, Choi Gi-eui, the CEO of KB Kookmin Card, said that “fee cuts appear to be a ticking time bomb toward reductions in customer benefits.”

Credit card companies said, due to the high processing costs, they already lose money on transactions below 10,000 won ($8.75), which make up a significant share of total card transactions in Korea.

“Although the break-even point is different for each card company, it’s true that a small credit card charge below 10,000 won is basically a guaranteed loss for all card firms,” said Kang Sang-won, spokesperson for the Korea Credit Finance Association (Crefia), the local trade group for card and consumer finance companies.

Using restaurants and an assumed transaction fee of 2.3 percent to illustrate the point, for every 10,000 won meal paid for by plastic, the restaurateur must pay a 230 won fee to the card company.

Of this, the company must pay 170 won to the value-added network (VAN) operators that install the card swiping machines and run the payment processing network.

It must then pay a further 120 to 130 won to cover its expenses, such as borrowing the money in the first place and footing the bill in advance. The net result is that the card company loses up to 70 won for every charge of 10,000 won or less.

Analysts say that the cut in card transaction fees for small businesses announced this week would cost each card company estimated losses of billions of won, although industry-wide figures are virtually nonexistent as companies are loathe to disclose these.

“No local credit card companies are listed except for Samsung Card, and exact data is hard to come by,” said Koo Kyung-hee, a banking and card sector analyst at Hyundai Securities. “But credit card transaction fees are the main source of revenue for card companies,” he added.

“In the case of Samsung Card, the cut in card transaction fees for small businesses [announced on Monday] is estimated to cost the company between 10 billion won and 20 billion won in annual losses.”

Experts said the latest development would have an impact but that it was not likely to be devastating.

“In terms of total profits, the loss is not dire, but it’s certainly a negative development,” said Koo, the card sector analyst. “Card companies will be pushed to make up for [the loss] by reducing their marketing and sales budgets, which in the case of Samsung Card runs into several trillion won per year.”

Those that take the card companies’ view argue that forecasts of budget reductions will cut into various discounts and services that many plastic-carrying citizens count on, such as gas price or grocery discounts.

“If there was pressure to lower the price of a bag of chips, you’d get fewer chips in a bag,” said Yun Chang-hyun, a professor of business administration at the University of Seoul. “If credit card transaction fees are lowered, a decrease in customer benefits, such as point systems, is sure to follow.”

Demanding a lower rate

The restaurateurs that are demanding credit card companies lower the commission rates claim their demands are not excessive.

Shin Hoon, head of the Korea Restaurant Association’s policy development bureau, said that all the restaurateurs are asking for is fairness.

“We’re not asking that the credit card companies lower their commission rates excessively to 1 percent or lower, as is the case in other countries,” Shin said.

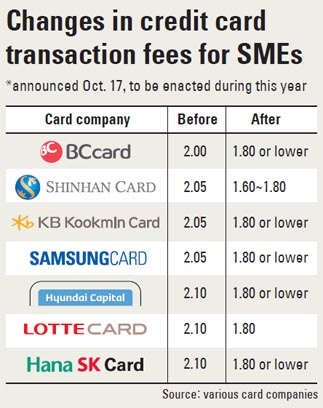

“Although the companies announced that they plan to lower rates above 2.5 percent to 1.8 percent, they have attached a condition that does not apply to other areas,” he said.

“If other businesses, such as department stores and gas stations, receive the unilateral rates regardless of their annual revenues, why should different rates be applied to small restaurants based on their earnings?” he added.

Citing a study by the Korea Insurance Research Institute in December last year, the association claimed that commission rates in Korea are considerably higher than those in other advanced economies.

The report put the average rate here at 2.08 percent, compared to 0.7 percent in France, 0.8 percent in Australia and 0.95 percent in Denmark.

“Most of the people who run small restaurants are in the low- to middle -income classes, so the high rates leave them with little leftover after labor and other costs are subtracted,” it said.

The restaurateurs and other small businesses claim that if a company’s annual revenue is below 200 million won, it earns roughly 18 million won a month in revenue. This means their net profits are far lower than that pocketed by employees at big conglomerates, they claim.

Meanwhile, credit card companies announced earlier that they will not only lower their rates to a maximum of 1.8 percent, but also extend the eligibility criteria for those to whom it applies to businesses with annual revenue below 200 million won. The cut-off point currently stands at 120 million won.

However, many restaurateurs were not satisfied with the proposal and demanded that the lower rate be applied across the board without any conditions attached.

“As Grand National Party leader Hong Joon-pyo has said, there should not be any discrimination in rates,” Shin said.

The restaurant association said the controversy had been gathering heat under the surface for a significant time before it erupted in recent weeks.

“This has been a demand that we have been making for years,” Shin said.

By Lee Jung-yoon, Lee Ho-jeong [joyce@joongang.co.kr]

한글 관련 기사 [머니투데이]

카드수수료 논란, 포인트·무이자할부 축소?

신용카드 수수료가 적정한지를 두고 벌어지는 업계와 당국의 줄다리기가 소비자 혜택 축소로 돌아갈 공산이 커졌다.

여론과 외압에 밀려 수수료를 내리기로 결정한 카드사들이 포인트, 무이자할부 축소 등 소비자 혜택을 줄일 수밖에 없다고 공공연히 밝히고 있기 때문이다.

하지만 카드사는 서로 눈치를 보는 상황이다. 누가 먼저 나서느냐에 따라 자사의 카드시장 점유율에도 역풍이 불 수 있어서다.

◇카드사 "또 수수료 인하? 우리도 적자"=20일 카드업계에 따르면 카드사들은 더 이상의 수수료 인하는 어렵다는 입장을 내놓고 있다. 신용판매에 따른 이익이 크지 않다는 이유에서다.

A카드사 고위 관계자는 "가맹점 수수료가 수익(매출)에서 차지하는 비중은 50%이상이지만 이익 기여도는 10%도 안 된다"고 털어놨다.

정태영 현대카드 사장과 최기의 KB국민카드 사장도 SNS(소셜네트워크서비스)를 통해 이같은 입장을 토로했다.

정 사장은 트위터를 통해 "젖소목장(카드사)이 있는데 우유판매(신용판매)는 적자라서 정작 소 사고파는 일(카드론 등 현금대출)이 주업이 되었다. 그런데 소장사로 돈을 버니 우유값(가맹점 수수료)을 더 낮추란다"라고 현 상황에 대한 속마음을 털어놨다.

최 사장은 페이스북을 통해 "카드 수수료 인하 발표에도 가맹점들은 여전히 불만"이라며 "수수료 인하가 이미 제공된 고객의 혜택 축소로 향해 가는 시한폭탄처럼 보인다"고 밝혔다.

◇소비자 혜택 축소 필요···하지만 누가?=금융당국도 드러내 놓고 말을 안 하지만 카드 이용에 따른 소비자 혜택이 너무 많다는 입장을 갖고 있다. 이를 줄여 가맹점 부담을 줄이는 쪽으로 가자는 복안도 읽힌다.

금융감독원에 따르면 카드사 전체의 매출액은 신용판매(가맹점 수수료 46.1%, 할부 수수료 7.8%)가 53.9%로 비중이 높고, 이어 현금대출(현금서비스, 카드론) 25.2%, 기타(리볼빙 등) 20.9% 순이다. 반면 이익은 대부분 현금대출에서 나오고 있다. 카드사의 신용판매 이익은 대부분 포인트, 마일리지, 할인, 무이자할부 등의 형태로 소비자에게 돌아간다.

이는 카드사들의 과당경쟁이 빚어낸 결과다. 금융당국은수수료 인하를 압박하면 카드사들이 스스로 소비자 혜택을 줄일 것으로 보고 있다.

하지만 카드사들은 스스로 소비자 혜택을 줄이지 못하는 구조가 됐다. 시장점유율 하락으로 이어질 것이라는 우려 때문이다.

◇혜택 축소엔 당국이 나서야 한다?=카드업계 안팎에서는 신용카드 수수료의 원가가 불명확한 만큼 투명한 정보공개로 소비자를 이해시키려는 노력이 필요하다는 의견이 나오고 있다.

B카드사 고위 관계자는 "신용카드의 시장구조를 건드리지 않는 한 해답이 없다"고 지적했다. 이제라도 신용카드의 시장구조와 수수료 체계에 대한 공동연구가 필요하다는 것이다.

금융사들이 공적 역할도 담당해야 한다는 자성의 목소리도 나온다. 또 다른 금융업계 고위관계자는 "현재 금융사는 (서민들 대상으로 돈장사를 해 부자들에게 혜택을 주는) `거꾸로 된` 부의 재분배 역할을 하고 있다"고 꼬집었다.

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)