More retirees drowning in debt

However, the clothing stores that made up his chief client base went under when the local clothing business soured during the 2008 financial crisis, and Lee has been plagued by bad credit ever since. This happened after he started relying on credit cards to pay his bills, as well as progressively higher-interest loans at savings banks and private lenders to cover monthly paychecks and rent before his own business failed.

Experts point out that amid the nation’s snowballing household debt problem, citizens of retirement age are drowning in deeper levels of debt as much of the older generation is financially ill-equipped for life after they stop working.

According to the Credit Counseling and Recovery Service (CCRS), a non-profit debt settlement organization, out of 75,850 delinquent borrowers that signed up for debt workouts last year, 24.2 percent or 18,342 people were over 50 years old.

More people in their fifties were in debt than any other demographic, with 19.4 percent of those undergoing debt settlement programs last year aged between 50 and 59. People over 50 have been steadily making up a larger share of total delinquent borrowers, rising from just 8.12 percent in 2002.

A personal debt workout program involves a deal with financial companies that sees them agree to write off up to 50 percent of a delinquent borrower’s debt, as well as clearing all loan interest payments and late penalties. Borrowers who are labeled “delinquent” after failing to pay their debt for a period longer than 90 days can pay back the principal over up to 10 years.

Debt had become a serious threat to the credit ratings of more than 20,000 people of retirement age, if the 2,636 people over 50 who signed up for “free workouts” last year are factored in. The programs were aimed at giving potential delinquent borrowers a way out before their credit ratings crash.

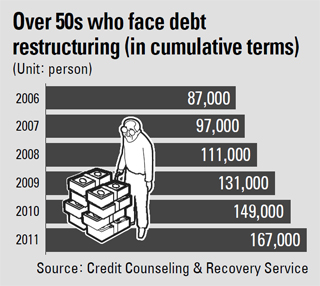

With a cumulative 167,015 people over the age of 50 becoming delinquent borrowers in the last decade, according to the CCRS, one in every 100 people in this age now falls into this category.

“It appears that while there are many remaining expenses, such as living costs or children’s education costs, those among the retirement-age population that have retired, lost their job or failed in their self-employed businesses seem to be increasing,” said a CCRS spokesperson.

“Delinquent borrowers are increasing in tandem with rising total household debt, and the growing ranks of the so-called ‘poor homeowners’ [citizens who own a house but are still mired in debt] is also a serious problem.”

Korea’s household debt reached 892.46 trillion won last year.

By Lee Jung-yoon [joyce@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)