Store owners paying for card firms’ marketing costs

Financial experts insist that Korea’s credit card payment system not only hinders competition among issuers, but also transfers the cost of attracting subscribers onto store owners.

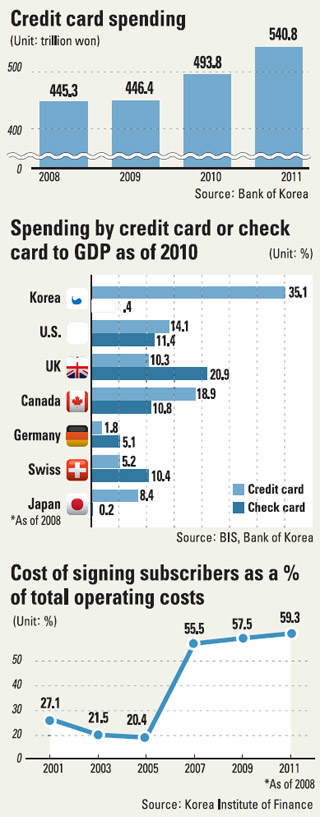

Last year, Korea’s credit card users spent over 540 trillion won ($483 billion), up from 493 trillion won in 2010, according to a recent report by the Bank of Korea.

With the average commission rate set at 2 percent, this means local businesses had to pay a whopping 10 trillion won in commission fees to card companies last year.

And a recent study by the Korea Institute of Public Finance shows that the rates levied on businesses have been growing at a galloping pace.

According to the study, the commissions they paid surged 321 percent from 2.27 trillion won in 2000 to 7.29 trillion won in 2010.

“This will eventually lead to higher inflation, meaning that the burden could spill over to consumers,” said Kim Jae-jin, a senior researcher at the Korea Institute of Public Finance.

The amount spent on credit cards last year was so high that it has only been eclipsed once in Korea’s history, which happened back in 2002 when it stood at nearly 620 trillion won and the local financial industry was rattled by a credit card crisis.

What is even more alarming is that installment payments by individual consumers amounted to 86 trillion won in 2011, a new record that smashed the 72 trillion won record set 10 years ago.

Encouraging credit card use

In 1999, the government started encouraging credit card spending by offering tax benefits such as end-of-year tax returns. The drive was so popular that regulations were changed and fines slapped on small shops that denied credit card use for miniscule payments of less than 1,000 won.

The government had two objectives in mind when pursuing this policy. The first was to revitalize the economy by promoting spending, which hit a lull after the Asian financial crisis in late 1997. The second was to make financial transactions more transparent to reduce tax evasion. Credit card spending started to pick up but dropped off again after hitting its peak in 2002. It fell to 352 trillion won in 2004 after the country was dealt a heavy blow by excessive competition among credit card companies, which led them to authorize multiple cards for high-risk groups including students and others with stockpiles of bad debt. This led to relentless subscriptions by people who had little realistic chance of paying back the money they borrowed.

As a result, credit card loans surged while delinquency flourished. In the end, LG Card went under and the government was forced to take extreme measures to resolve the problem.

However, since 2005, credit card spending has once again started to accelerate. Of total private spending in recent years, credit cards accounted for more than 60 percent, or 90 percent of all card payments including debit cards.

Credit card usage is exceptionally popular in Korea, even compared to major economies like the U.S., UK and Australia, where debit cards are more often the preferred choice. As a result, credit card companies have been aggressively investing to attract more subscribers despite government pressure to cool their promotions.

The operating costs of credit card companies, excluding banks such as Hana, Shinhan and KB Kookmin, reached 600 billion won last year, double that of 10 years ago. Moreover, nearly 60 percent of these costs went on attracting subscribers, up from 27 percent in 2001. Some of these costs are then transferred to small shops.

Isolated structure

The reason credit card companies here can transfer the financial burden to stores is largely because of the isolated structure of the industry, unlike in countries like the U.S. and Australia, which operate more open systems, according to the Korea Finance Institute.

In Korea, credit card companies not only issue cards, but also function as the acquiring bank. This gives stores very few options in terms of choosing between different commission rates.

Additionally, Korean law dictates that businesses are not allowed to waive credit card payments, further restricting their choices.

The open system that is used in the U.S. differs as the card issuer is separate from the acquiring bank. The latter processes the credit or debit card that businesses use to buy a product or service, which allows the issuer to be more competitive by offering lower commission rates and a wider variety of products.

Experts say the Korean system lets credit card companies transfer their costs to customers when commission rates are lowered.

“Instead of lowering their commission rates, credit card companies will likely reduce the benefits offered to subscribers in order to cover their operating costs, including the money spent on promotions to attract more customers,” said an official at the Korea Finance Institute.

“So discount services may be jettisoned, along with programs that accumulate points to be redeemed at a later stage in the form of other products or services.”

By Lee Ho-jeong [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)