Trade in equity-linked warrants collapsing

On a Web site where investors lodge complaints about Korea’s financial regulators, there are posts containing cries from the heart from people who bought equity-linked warrants, or ELWs.

“I’ve been investing in ELWs for more than four years, feeding my wife and kids,” wrote one retail investor in March. “But with the [latest] regulatory measures, my livelihood has been lost .?.?. Do all retail investors look like unfair traders to regulators?”

What had been the world’s second-largest market in ELWs is in danger of extinction after restrictive regulations were imposed to wipe out speculation by so-called “scalpers” - which many say are also driving away day-trading retail investors.

Equity-linked warrants are derivatives similar to options that give the holder the right, but not the obligation, to buy or sell an underlying asset at a set price on or before an expiration date.

ELWs are priced cheaply - often around 1,000 won (88 cents) per warrant - and in Korea they are tied to underlying assets like blue chip stocks in the Kospi 200 index that rank in the top 100 in terms of market cap and have plenty of turnover. As such, ELWs were an investment vehicle targeted toward retail investors who want to bet on the movement of large-cap stocks with little money.

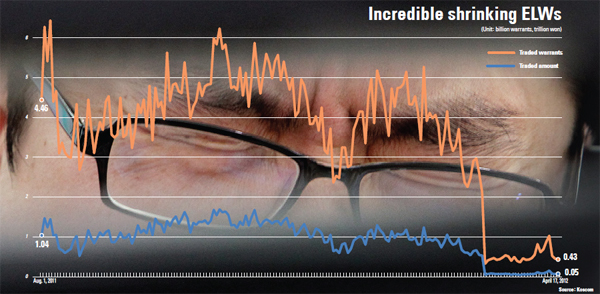

This drove the local ELW market, established in December 2005, to grow into the second-largest market in the world after Hong Kong by 2010 with average daily trading reaching 1.6 trillion won.

Those glories are now past. The Financial Services Commission instituted new rules to “bolster the soundness of the ELW market.” Since they went into effect March 12, average daily ELW trading has collapsed to 65.45 billion won. The frequency of transactions has fallen by more than 85 percent from the average daily trading in February, according to Koscom Data, an investment data provider.

Scalpers are in-and-out traders that buy and sell financial instruments many times a day in quick succession in order to profit on relatively small price changes. The FSC wanted to rein them in to reduce volatility in the ELW market.

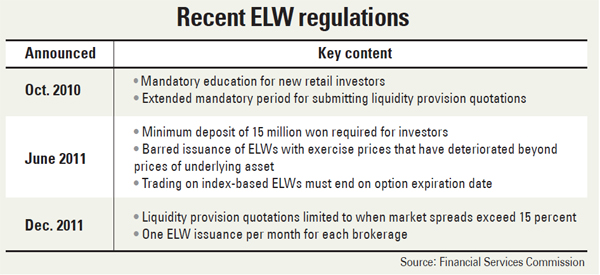

The key reason the market has collapsed is because of a new regulation that limits when liquidity providers (LPs) can submit asking prices.

Because ELW prices swing in very small units - the smallest unit, or “tick,” is just 5 won - even if a lot of traders are submitting asking prices on the market, an investor can still find that existing prices will force them to trade at a loss. As this could discourage trading, LPs use their own money to offer ELWs at additional asking prices, giving investors a much wider range of prices to sell or buy at.

Previously, LPs could submit asking prices at their own discretion. Now, LPs can only submit asking prices when the “market spread ratio” - the average gap between an asking price and bid price against the bid price - exceeds 15 percent.

“This narrowed the range of transaction prices at which investors could choose from to a crippling level,” said the director of equity derivatives at a local brokerage.

Analysts said that last month’s measures dealt a final blow to a market already reeling from previous regulatory restrictions, such as a 15 million won mandatory deposit for any newcomers to ELW trading.

“The 15 million won entry barrier might be considered more restrictive for retail investors than scalpers,” said the director. “I believe true consumer protection would be not to restrict, but to inform.”

Brokerages and investors alike are seeking alternatives to the frozen ELW market. Brokerage house officials report increased queries about the Hong Kong ELW market.

At the same time, some brokerages are trying to revive the market by educating investors on how it really works. Korea Investment & Securities held a consumer seminar on ELWs at its customer center in Garak-dong, southern Seoul, yesterday.

“In this new market environment, investors need a correct understanding of ELWs,” said Park Eun-joo, head of equity derivative marketing at Korea Investment & Securities.

By Lee Jung-yoon [joyce@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)