As insurers enjoy record profits, policy holders feel the pinch

Controversy is brewing in the non-life insurance industry as record profits are to fall into the laps of shareholders in the form of hefty dividend returns, with policy holders excluded from the benefits.

And while property insurers are reaping in returns, they insist prices should be raised due to the persistent growth of loss ratios over the years.

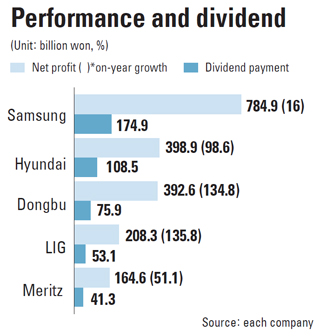

Major non-life insurance firms have announced their performance results for the 2011 fiscal year that started in April and ended in March 2012. Most reported net profits doubling on-year.

LIG Insurance saw its net profit surge 135 percent on-year to 208 billion won ($181 million) while Dongbu Insurance’s net profit saw a similar expansion of 134 percent to 392 billion won.

The net profit of Samsung Fire & Marine Insurance saw a more limited 16 percent growth compared to the 2010 fiscal year, reaching 784.9 billion won.

However, non-life insurers claim that these profits were not the result of exceptional growth in insurance sales.

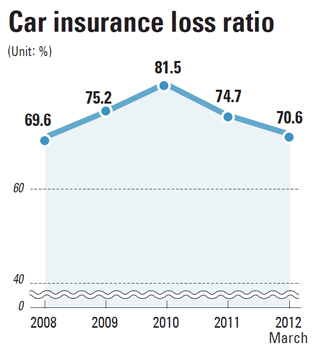

They cited instead lowered insurance loss ratios on car insurance and increased profits from managing assets as the major factors boosting profits.

v“In the 2010 fiscal year, non-life insurance companies overall lost 1 trillion won in car insurance alone,” said an official at the Korea Non-life Insurance Association (KNIA).

“Last year that loss was limited to 300 billion won.”

Regulations on the financial burden in repairing insured cars that were in accidents have changed, and insurance companies are now responsible for paying less and improving loss ratios.

Previously, when an insured car got into an accident, the policy holder only had to pay a certain fixed amount - usually around 50,000 won - while the rest was covered by the insurance company.

Additionally, car accidents fell immensely as it snowed less than in previous year.

“Although the losses from car insurance have fallen significantly, we are still suffering from losses,” said Han Je-hee, an LIG Insurance official. “Most of the profits came from managing our assets.”

The insurers’ persistent claims that the profits resulted from exceptional investments on its assets is speculated as a move to seal off any pressure in lowering insurance payments.

Earlier this year, as the loss ratios on car insurance fell, non-life insurers lowered insurance payments on cars by 2 percent.

Some claims that the insurers have been nervous of the possibility that lowered car insurance payments may start a movement that would pressure the insurers to lower other policies.

“[The insurers] managed the assets while embracing risks and therefore this profit should not be passed on to policy holders,” said Ko Joong-boong, an official at KNIA.

“It is the same logic in saying that the losses that were generated from bad investments of assets would be transferred to customers by raising insurance payments.”

Accoding to the KNIA, 11 non-life insurers have raised the insurance payments on renewed three-year maturity medical indemnity insurance policies by an average of 34 percent recently.

“As medical insurance has become popularized, the outflow of medical costs has increased significantly,” said an employee working at a non-life insurance firm speaking on the condition of anonymity.

“As the loss ratio has reached 110 percent, raising the payments on renewed insurance policies is inevitable.”

The insurance companies, however, are under fire since while they are busy trying to raise insurance payments when suffering from losses, they are busy handing huge dividend returns to management and shareholders when making profits.

LIG Insurance, Samsung Fire & Marine Insurance, Meritz Fire & Marine Insurance, Hyundai Marine & Fire Insurance and Dongbu Insurance are scheduled to hold its shareholders meeting in June.

The insurance firms are planning to pay a combined 453.7 billion won in dividends to their shareholders. This is 23 percent of the combined 1.9 trillion won net profits.

The Financial Supervisory Service in March called the heads of the non-life insurers to ask them to refrain from making huge dividend payments.

“The non-life insurers should be thinking of how to return the huge profits that they have made to the consumers, but they are showing a tendency to only take care of shareholders,” said Cho Nam-hee, secretary general of the Korea Finance Consumer Federation.

“The expanded profits made from asset managements are actually money that the insurance policy holders have supplied through their insurance payments and therefore it is appropriate that the profit should be returned.”

By Lim Mi-jin [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)