Auto insurers pace entry into China

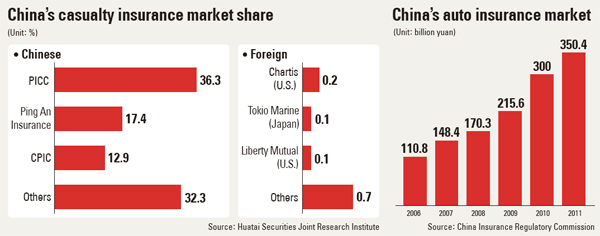

“The market is already worth 350 billion yuan [$55 billion] but its growth potential is unlimited, and foreign insurance companies are closely watching the market,” Woo said.

“We need to be careful in terms of how fast we try to enter the market and how much we are going to spend.”

Samsung is not alone among local insurers pursuing business opportunities in China.

At the beginning of last month, Beijing completely opened up its auto liability insurance market to foreign operators.

In the past, they were only able to sell supplementary auto insurance products.

The Chinese auto insurance market has expanded 136 percent since 2007, but analysts believe there is still huge room for growth.

“The number of new cars being registered there every year stands at between 13 million and 18 million, which is roughly equal to the total number of cars registered in Korea,” Woo said.

“And we see things continuing at this pace for some time.”

Samsung Fire and Marine Insurance, LIG Insurance and Hyundai Insurance are already selling supplementary auto insurance policies in China in cooperation with Chinese brands.

They are expected to launch their own brands there within one or two years.

“We partnered with Chinese companies as we had no other option,” said Lee Jae-yong, chief of foreign operations at Hyundai Insurance.

“But now that we can sell policies independently, we’ll be able to compete with Chinese insurers on our own.”

However, pundits say the market will not be an easy one to crack because of all the red tape involved in getting permits from regional governments.

To build a national sales network, insurers need licenses from 22 provinces, five autonomous regions and four direct-controlled municipalities, with the exception of Hong Kong and Macao.

“Insurers need to have a large amount of capital to obtain permits and it will be difficult for small insurers to enter China,” said an official at a local casualty insurer.

At present, three Chinese companies control two-thirds of the market, giving them enormous clout.

Korea’s Dongbu Insurance set up a small company in China in February 2011 to focus on the market there.

“We are interested in the Chinese market, but we came to the conclusion that, considering the huge cost and time involved, we need to build up more experience first,” said Shin Hae-yong, who leads a department at Dongbu.

“After we learn more about the Chinese market through the sales agency we have established there, we’ll enter it directly.”

“Non-Chinese insurers have insufficient sales networks in China and their market data is lacking. They won’t be able to expand their market share there quickly,” said Kang Mi-jeon, a researcher at the Hana Institute of Finance.

“Local insurers have neither the network nor the reputation to thrive in China, so they need to differentiate their services, such as by focusing on the wealthy.”

By Lim Mi-jin, Kim Hye-mi [jbiz91@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)