Household debts climb worryingly

The household debt crisis, which was losing urgency earlier this year due to heavy pressure from the government to decelerate the growth of household borrowing, has once again reignited as debt reached a new record level.

The speed at which the debts are mounting and affecting the middle and upper income classes is raising alarms that debt could be a millstone around the economy’s neck.

The government says it is aware of the deteriorating situation and will soon launch countermeasures. Yet the government is also accused of being overly sanguine about the mounting problem, having recently eased borrowing restrictions on real estate purchases to give a fillip to the property market - at the risk of encouraging more borrowing.

At a National Assembly hearing a week ago, Finance Minister Bahk Jae-wan told lawmakers that he acknowledged the severity of the household debt problem and promised government measures targeted at vulnerable types of people, such as those who borrowed multiple loans or people who are “house poor” - whose properties’ values are lower than their mortgages, and who can barely afford other expenses beyond mortgage payments.

Yet the minister downplayed the growing risk.

“We believe the [debt] situation could be [directed toward] a soft landing since the speed of household debt expansion is slowing while the [debt] quality structure is improving,” Bahk said. “Yet we will continue to stay alert and continue to manage the risk factors.”

He added that the debt situation needs to be tackled with particular caution as the wrong moves could send out faulty signals to the market.

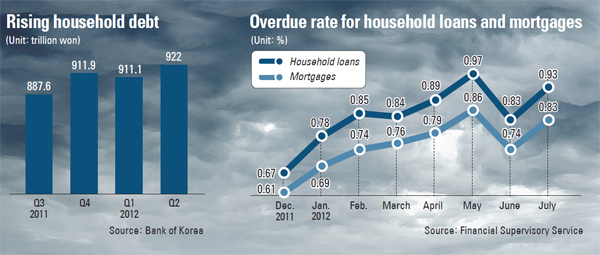

According the Bank of Korea, household loans has reached 922 trillion won ($814 million) as of the end of June, a new record. The rate of expansion has slowed. In the second quarter, household debt grew 5.6 percent on-year compared to 7 percent growth in the first quarter and 8 percent growth in the third and fourth quarters of last year.

However, when compared on a quarterly basis, borrowing has regained its momentum.

And Korea’s household debt today is twice the size of what it was a decade ago. In 2002, household debt totaled 465 trillion won.

Furthermore, the proportion of borrowers behind on their payments of household debt is on the rise. As of July, the overdue rate was 0.93 percent, up from 0.83 percent the month before. The overdue rate in May hit a five-year high of 0.97 percent. In February 2007, the rate was 0.93 percent.

The mortgage delinquency rate in July was 0.83 percent, up from 0.74 percent in June.

According to the financial industry, the government’s pressure on commercial banks to cut back on household loans has pushed many borrowers to nonbanking financial companies. Borrowings in that sector are rising rapidly.

As of May, the number of people who are overdue on payments to credit card companies is estimated to have grown 25 percent compared to a year earlier, while delinquent customers are estimated to have grown 18 percent in savings banks and 12 percent in private lenders from a year earlier.

Hitting the upper classes

The loans are growing in size and in lateness - and increasingly, the problem is spilling over to the middle and upper classes.

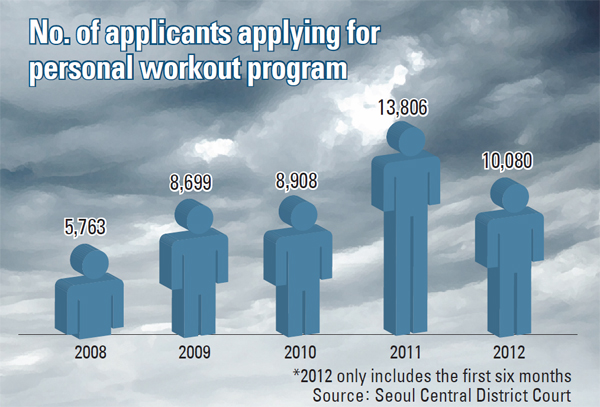

This year alone, the number of people applying for personal debt workouts in courts has grown significantly.

In Seoul alone, the number of people who have requested debt workouts in the first half of the year amounted to over 10,080. Considering that 13,800 people applied for workouts in all of 2011, things are worse this year.

The proportion of middle and upper class people applying for debt workouts is on the rise.

Recent data by the Credit Counseling & Recovery Service showed that among those who applied for debt workout in the first half of this year, 82 percent earned less than 1.5 million won a month, a decline from 88 percent in 2010.

A family of four that makes less than 1.5 million won a month is considered to be lower income.

Debt workouts are usually applied for by people who haven’t paid back loans for more than three months. Through negotiation with the financial company that handed the loan, they can either have their debt reduced, the interest rate lowered or the term of the loan extended.

Such programs are limited to people with debt of less than 500 million won and the ability to pay off their debt through a stable income.

Even size of the debts being worked out is on the rise. People who requested debt workout on more than 50 million won in loans accounted for 9 percent of the total in 2011. This figure grew to 10 percent in the first half of this year.

Absence of solution

While debt continues to balloon, the government has yet to come up with measures other than forcing the financial industry to limit their lending.

The last time the Ministry of Strategy and Finance and the financial regulators laid out measures to curb household debt was in February.

In the interim, the government kept saying it would come up with additional measures if needed urgently.

At a forum in December, Kim Seok-dong, the Financial Services Commission chairman, said, “We will step up our management so that household debt will increase at an acceptable level.”

Yet in the past six months, no detailed measures to cushion the rising risk have been introduced.

Analysts say the government should look into the problem more deeply.

“There are demands for rushed solutions without properly understanding the pressure that result from the mushrooming household debt,” said Yoo Kyung-won, a Sangmyung University professor.

“Measures that are made too hastily will only dodge the problem temporarily and cannot be a fundamental solution.”

By Lee Ho-jeong [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)