If won rises too fast, it’s too late

Currencies are also ranked. The U.S. dollar sits in first place. It has not always been at the top as it changed places with the British sterling to become the world’s reserve currency with the end of World War II. To rebuild a global financial order from the rubbles of war, allied nations gathered in Bretton Woods, New Hampshire, in July 1944.

To fund postwar reconstruction and revive international trade, the states agreed to fix their exchange rates to the U.S. dollar that was linked to gold: $1 per 35 ounces of bullion. Thus was born the first global monetary order, Bretton Woods, named after the location of its birth. The British resisted, but American politicians won the argument. Value is determined by national strength, and the United States was undoubtedly the most powerful nation at the time.

Over the following seven decades, the dollar has survived numerous currency wars. The Fed defended its hegemony adroitly. During wealthier times, it reinforced the greenback, and in slower days with debt piling up and waning trade competitiveness, it let the dollar weaken. The dollar flowed with the economic current, but mostly with small ripples. A weak dollar served as a panacea for U.S. economic headaches. It strengthened competitiveness of made-in-the-U.S. products and helped cut deficits and lower debt.

The U.S. printed out bills and drove down the currency value to keep the dollar weak against other currencies. Its weak-dollar campaign drew criticism from trade competitors, but the U.S. chose to ignore it to keep America Inc. competitive. The self-interested monetary policy was famously epitomized by Secretary of Treasury John Connally, who bluntly told his foreign counterparts who protested the devaluation, “The dollar may be our currency, but it’s [devaluation is] your problem.”

The bloodless currency warfare, or competitive devaluation, can be more demoralizing and devastating than territorial battles. You are attacked and lose without knowing why and are sometimes unaware of the defeat. Japanese economist Yoshikawa Mototada in his book on currency wars said a state hands over its assets gracefully to the enemy after losing the invisible war, which makes the defeat more humiliating and painful. He claimed that the 1990 bursting of the bubble in Japanese assets that led to the lost decades was exacted by the crushing defeat of the “strong yen” versus “weak dollar” war. He said the ramifications of the defeat were as mortifying and devastating as the atomic bomb dropped on Japan during World War II.

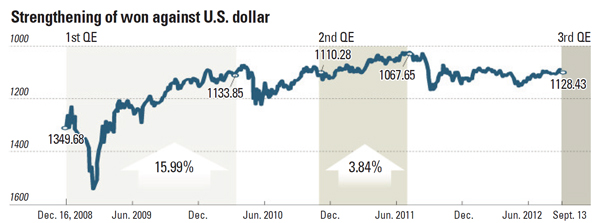

The world is now again swept in a new currency war, ignited by Washington’s old trick of weakening the dollar. The U.S. Federal Reserve announced and immediately acted on the third round of quantitative easing, pledging to purchase a total of $40 billion a month in mortgage-backed securities to prop up the economy by keeping the borrowing rates low and encouraging spending.

The so-called beggar-thy-neighbor policy - or a gain at other nations’ expense - triggered similar counteractions from Europe and Japan, likely joined by China. In just weeks, Americans, Europeans and Japanese have all begun to print new money, which is unprecedented in the global financial market, said one securities broker. The competitive devaluation immediately drew a chorus of criticism from the emerging corner. Brazilian Finance Minister Guido Mantega had harsh words for the Fed’s “protectionist” move and warned of strong defensive actions to fend off the ills of a weak dollar and flood of global liquidity.

The ripples have already arrived on our shores. The stimulus cash from richer economies is already rushing into the local market chasing foreign exchange gains. Foreigners snatched up 1.6 trillion won ($1.4 billion) worth of Korean equities and bonds on the day the Fed announced its monetary stimulus program. Foreigners this year bought 40 trillion won in Korean assets. The stock price index recovered to above 2,000 and the won hit new year-highs.

But today’s boon can be tomorrow’s nightmare if such a lofty amount of capital exits. We were already there after the last second round of U.S. quantitative easing in 2010. The Korean market is called a cash machine for foreigners. We must not sit around idly, blinded by the rise in stocks and currency values. If necessary, our monetary authorities should take necessary easing actions and capital controls.

Yet the Bank of Korea last week decided to keep the key interest rate unchanged. The Ministry of Strategy and Finance simply responded with verbal interventions that it was “keeping a close watch.” A senior official said the government would not want to easily disturb the bullish trend in the stock market due to the presidential election in December.

But the aftermath of a free-falling currency is devastating. Historian Niall Ferguson wrote about the collapse of the pound, saying the British learned one thing as their currency yielded global primacy to the U.S. dollar: A nation must be strong for the currency to be a burden on other economies or otherwise the burden will be theirs.

* The author is the editor of the business desk of the JoongAng Ilbo.

by Yi Jung-jae

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)