Subscribers accept losses to cancel insurance policies

She lost 500,000 won but said this was acceptable given the current climate of risk and low returns.

Earlier, Seo took out a 50 million won bank loan to cover half of the deposit for a new apartment she was moving into, as well as the monthly rent of 400,000 won. However, she said she struggled to pay back the monthly interest of 200,000 won after sales at the restaurant dwindled.

“I had no option but to cancel the policy just over six months before it was set to mature,” Seo said. “Now I only have my life insurance policy.”

Squeezed by the slowing economy, market observers said more people like Seo are canceling their installment savings and insurance policies to keep their heads above water.

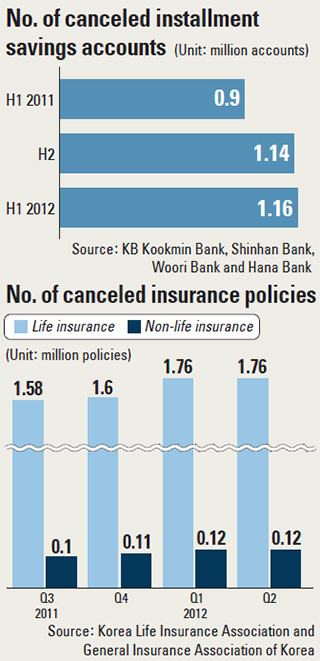

According to four local banks - KB Kookmin Bank, Shinhan Bank, Woori Bank and Hana Bank - 1.16 million installment savings accounts were canceled before they matured in the first half of this year, up 30 percent from 0.9 million a year earlier.

The sluggish economy has also dealt a severe blow to the insurance industry as waves of subscribers cancel their policies and more insurers do the same after failing to receive payments for two straight months.

A quartet of local non-life insurers reported recently that 253,000 savings-linked insurance accounts were cancelled in the first half of this year, up 40 percent from 2011. They were Samsung Fire and Marine Insurance, Hyundai Insurance, Dongbu Insurance and LIG Insurance.

Canceling means subscribers cannot receive the principal in full, and those who end their contracts with less than six months remaining don’t get a dime. Those who pull the plug one year after subscribing get 66 percent of the principal refunded on average.

“Cancellations have been escalating rapidly since the second half of last year,” said an employee at a non-life insurer.

Market observers say snowballing household debt is creating a vicious cycle.

They say growing debt has inflated interest payments and forced households to put less money in the bank. Cash-short families take out extra loans to make ends meet.

Kim Dong-yeop, chief of the retirement education center under the Mirae Asset Investment Education Research Institute, advised people to cancel their savings accounts rather than insurance policies due to the tiny size of refunds.

“If they have no other option but to cancel their insurance policies, they should go for the most recently inked policies first,” Kim said.

By Kim Hye-mi [mijukim@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)