A variable rate that doesn’t move

Lee, 52, wasn’t too happy when he went to the bank to make a payment on his loan.

It’s been 11 months since he extended the three-year maturity loan on a variable rate for another year. During the past 11 months the central bank lowered the key borrowing rate twice - yet the interest rate on his loan has remained unchanged at 5.73 percent.

When he complained to the bank, an employee told him that the interest rate remained the same because he extended his debt for a year. As a result, it reflects changes in interest rates after a year instead of reflecting changes in a three-month or six-month period.

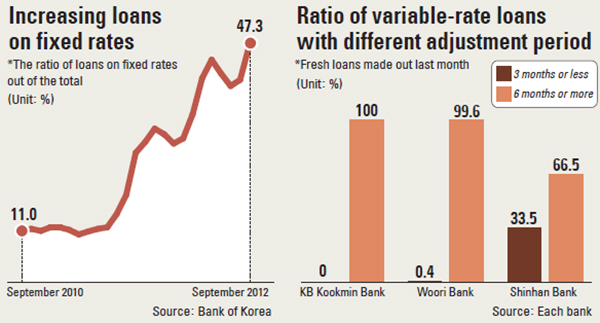

As the threat of recession looms over the economy, banks are cutting back on loans with a three-month variable rate. Instead they are expanding products with six- to 12-month variable rates.

This is a contrast to two years ago when almost 90 percent of the variable rate loans reflected the changes every three months. A six- to 12-month variable rate is practically a fixed-rate loan as the lowering of the seven-day repo rate doesn’t affect those loans for a long while.

In fact when customers ask banks for a three-month variable rate loan, they are told it’s possible to get one but the rate is higher than on six-month variable rates.

The banks began to increase the sales of such loans in the second half of last year. This was when the euro zone crisis and the deepening global recession were spreading worries that the central bank would be pressured to lower the key borrowing rate.

Some of the banks simply stopped selling three-month variable rate loan products.

Since this year, KB Kookmin Bank has been selling only loan products with a six-month rate. It’s almost the same with Woori Bank. Last month, among the new mortgages taken out by customers, those with a three-month rate only accounted for 0.36 percent of the total.

According to industry analysts, the variable rate on mortgages fell to the 4 percent range this month. However, people who took out loans in June still have to pay a 5 percent rate.

“Offering a loan product with a one-year rate at a time when interest rates are falling is just cheating customers who lack information,” said Cho Nam-hee, head of the consumer protection group Financial Consumer Agency.

Others say the fact that consumers’ choices are limited is a major problem.

“It’s really hard to call loans with six- to 12-month rates, variable rate products,” said Kim Woo-jin, a researcher at the Korea Institute of Finance. “Especially when those with three-month rates are no longer selling in the market, consumers are being deprived of a choice.”

He said that abroad, banks call their customers when the central bank raises the benchmark borrowing rates and ask if they are interested in switching to a fixed rate product, while when interest rates are going down, they ask if they’re interested in switching to a variable rate product. It seems banks in Korea are doing to opposite,” Kim said.

The banks say they are just following the orders of the financial regulators to stabilize the household debt situation.

Since last year, financial regulators have been pressuring banks to curb lending as borrowings were breaking new records. As of June this year, household borrowing amounted to a record level of 922 trillion won ($844 billion). The financial regulators said the debt is a threat to the stability of the financial markets.

“Customers could face a burden when they borrow loans with shorter adjustment periods and the key borrowing rate starts being raised,” said an official at KB Kookmin Bank.

“It is the financial regulators policy to expand loans on fixed rates as well as loans with longer adjustment period.”

By Lim Mi-jin [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)