Rush of interest in property accumulation savings

All the counters were busy with customers inquiring about opening the accounts that offer interest rates of 3.8 percent to 4.6 percent for the first three years and tax breaks on deposits of up to 12 million won ($11,064) per year that stay in the account for more than seven years.

“Until the launch of property accumulation savings, there were no bank accounts that offered interest rates higher than 4.5 percent,” said Park Chan-min, a 32-year-old salaried worker. “I figured I shouldn’t miss this opportunity to amass a fortune.”

Korea Exchange Bank, Shinhan Bank, KB Kookmin Bank, Industrial Bank of Korea in Dogok-dong, where Tower Palace, a residential complex often considered an icon of wealth in Gangnam stands, were also busy with customers.

Access to Hometax, a Web site run by the National Tax Service where people can print out government-certified income statements, was jammed for hours Wednesday when 15 local banks began accepting applications for property accumulation savings accounts.

The Financial Supervisory Service said 279,180 accounts worth 198 million won ($181,468) were opened on Wednesday alone, and market observers estimate more than 200,000 additional accounts were established Thursday.

Heated competition

Estimating that 9 million people will sign up for property accumulation savings, banks have entered a heated competition to attract customers by raising interest rates.

Korea Exchange Bank, Standard Chartered Bank Korea, Busan Bank and Jeju Bank increased their rates by 0.3 percentage point to 0.4 percentage point.

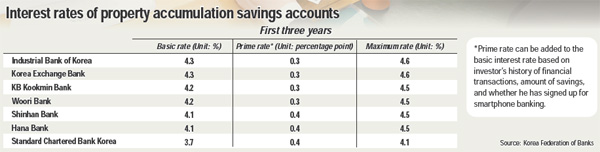

KEB on Friday raised interest for property accumulation savings to 4.6 percent from 4.3 percent.

“We have contacted customers who signed up for accounts on Wednesday and Thursday to cancel their accounts and get new accounts because interest rates have gone up,” said an employee at KEB. “We have kept the prime rate to 0.3 percentage point, and raised basic interest to 4.3 percent from 4 percent.”

The changes mean KEB and Industrial Bank of Korea offer the highest rate (4.6 percent including prime rate) that customers can get depending on their history of financial transactions, amount of savings and whether they signed up for smartphone banking.

NH Nonghyup Bank, KB Kookmin Bank, Shinhan Bank and Hana Bank offer 4.5 percent annual interest, including prime rate.

Excluding prime rate, Nonghyup and Industrial Bank of Korea offer the highest basic interest at 4.3 percent. Still, that is at least a percentage point higher than ordinary savings accounts, banks said.

Market observers said the government’s revival of property accumulation savings for the first time in 18 years has encouraged people to rush to banks as account holders will get a 14 percent interest income tax exemption when they deposit up to 12 million won per year in the account for more than seven years.

Salaried workers with less than 50 million won in annual income and business owners with 35 million won in business income are eligible for property accumulation savings accounts.

Positive effect

The government has revived property accumulation savings to boost household savings and provide a solid investment option for a wide range of people.

After introducing the policy in 1976, the government abolished property accumulation savings in 1995, citing diminishing government resources.

The household savings rate at banks that rose as high as 25.9 percent in 1988 from 7.5 percent in 1975 and contributed to the country’s economic development, but tumbled to 2.7 percent in 2011.

Experts said decreasing household savings could hamper economic growth, and property accumulation savings could be a good option.

“If the ratio had been 5.3 percent, the OECD average, in 2011, Korea’s economic growth rate would have been at least 0.5 percentage point higher,” said Kim Cheon-gu, a research fellow at Hyundai Economic Research Institute. “If the household savings rate goes down by 1 percent, investments decrease by 0.25 percentage point and economic growth falls by 0.19 percentage point.”

Moon Hong-cheol, an analyst at Dongbu Securities, expects the boom in property accumulation savings to boost demand for two- and three-year bonds.

“Banks are likely to buy more two-and three-year bonds as they give fixed interest for the first three years to the accounts. Banks’ demand for one- and two-year bonds to manage time deposits and their demand for three- to five-year bonds to manage annuity insurance will shift to two-and-three year bonds to efficiently manage property accumulation savings.”

Not so fast

Experts, however, warn investors not to blindly invest in property accumulation savings accounts.

They said people should thoroughly check whether they have an adequate regular source of income to deposit up to 12 million won per year in the account for more than seven years as terminating accounts could lead them to have to repay exempted taxes to banks.

Only 20 percent have managed to keep accounts for more than seven years without terminating them, market observers said.

They also warned that interest rates for property accumulation savings accounts could go down as initial rates are fixed only for the first three years.

“If the low interest rate trend continues, this would lower the interest of property accumulation savings to the 3 percent range and investors may find the financial product less attractive,” said a banker. “Most banks are considering not giving prime rate in addition to basic interest from the fourth year. Investors should determine whether to deposit money in the account after checking their financial condition as well as bank policies. There’s still plenty of time left for investors to make a decision, because the government will not stop giving tax breaks on the account until 2015.”

By Kim Mi-ju [mijukim@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)