Gov’t eases household debt fears

Finance Minister Hyun Oh-seok, left, and Shin Je-yoon, FSC chairman answer lawmakers’ questions yesterday at a hearing in Yeouido, western Seoul. [NEWSIS]

However, they added that the 960 trillion won ($839 billion) debt is not at a critical tipping point that could severely disrupt financial markets.

For the first time, a National Assembly hearing on household debt was held in Yeouido at which the top government’s top economic officials - Deputy Prime Minster on Economics and Finance Minister Hyun Oh-seok, Financial Services Commission Chairman Shin Je-yoon, Financial Supervisory Service Gov. Choi Soo-hyun, Land Minister Suh Seoung-hwan, Bank of Korea Gov. Kim Choong-soo and Credit Counseling and Recovery Service Chairman Lee Chong-hwi - sat in a row facing lawmakers.

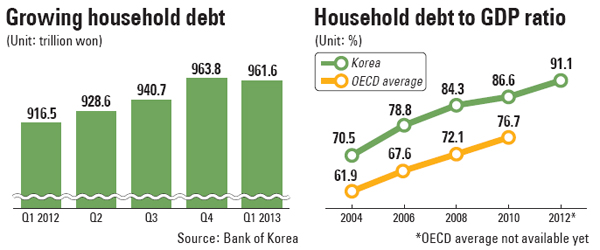

As of March 31, debt stood at 961.6 trillion won. Although this is a slight dip from the record of 963.8 trillion won posted in the fourth quarter last year, experts say that at the current pace, even with banks more conservative in their lending, household debt will easily surpass 1,000 trillion won in the near future.

Furthermore, the household debt to GDP ratio stood at 89.5 percent as of late 2011; the OECD average is 76 percent. Korea ranked 10th among the 28 member countries.

The government says there is low risk of current debt growth triggering a financial crisis.

Korea has had two debt-triggered financial crises in the past. From 1995 to 1997, household debt soared 22 percent annually, making the economy even more vulnerable during the 1997-98 Asian financial crisis.

From 2000 through 2002, household debt again surged 27 percent each year due to falling income and increasing credit card use.

“The current growth in household debt is not at a serious level, although we consider the matter a serious issue,” said Finance Minister Hyun at the hearing yesterday.? The Ministry of Finance’s report showed the country’s top earners account for 71 percent of the total debt.

But the government officials acknowledged the risk.

The finance minister pointed out the impact debt could have on domestic economic growth.

Although 71 percent of debt was by high-income earners, they have cut back on spending recently.

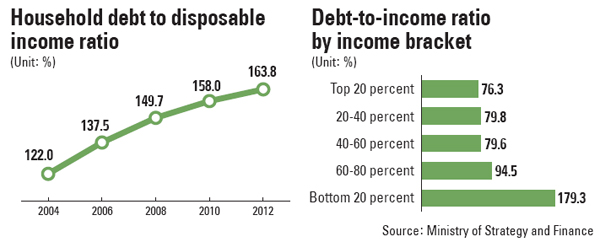

The government also expressed concern about low-income households and senior citizens, whose debt-to-disposable income ratio hovers at about 180 percent.

As of March, households in the bottom 20 percent income bracket hit a debt-to-income ration of 184 percent, higher than any other group.?

By age, the rate for those in their 50s hit 207 percent and in their 60s 253 percent.

According to data from the Financial Services Commission, an estimated 3.22 million debtors have loans from multiple institutions, while the so-called “house poor,” those unable to pay their mortgages, number about 98,000.

As low-income people increasingly chose nonbanking financial institutions for easier credit, the growth in those loans outpaced that of loans by commercial banks in recent years.?

The proportion of higher-interest loans issued by nonbanking financial companies rose from 29 percent in 2006 to 34 percent as of March 31.

As for the looming end of U.S. quantitative easing and possibly higher interest rates in the local market, the deputy prime minister said those with adjustable interest rate loans can save money by switching to loans with fixed rates.

BOK Gov. Kim proposed to establish a bad bank in order to prevent soured loans from increasing.

“There should be a contingency plan to deal with soured loans en masse in case of delayed economic recovery and falls in housing prices,” he said.

FSC Chairman Shin mentioned that the government’s flagship “People’s Happy Fund” will help to address the household debt issue.?

“Since a significant number of low-income households are not able to repay their debt, the government is trying to write off part of their debt,” Shin said. “The FSC will come up with a plan to improve the microfinance industry and is considering conducting a comprehensive investigation into debt amounts of those in the bottom 20 percent income bracket.”

BY Song su-hyun [ssh@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)