Market assesses Tongyang fallout

With financial authorities now turning the case over to the prosecutor’s office, the question in the market is how much impact the Tongyang crisis will have on the retail corporate bond market.

Some market experts say retail investors will be hesitant to invest in corporate bonds and commercial paper, especially those issued from companies with low credit ratings. As a result, such companies will struggle more to secure capital inflows, which have been dwindling since late last year.

Retail investors damaged

According to the Financial Supervisory Service (FSS), the corporate bonds and commercial paper of Tongyang’s affiliates amounts to 1.4 trillion won ($1.3 billion). Most of the 40,000 investors who purchased the bonds and papers are individuals.

As of Saturday, more than 7,300 people had filed damage reports totaling 309 billion won to the FSS. Of those, 72.6 percent were people who invested less than 50 million won.

“I invested 20 million won in Tongyang bonds,” said a retail investor named Chang. “If I knew that the company would fall apart just overnight, I wouldn’t have made the investment.

“All I did was trust the broker. But now that the situation has burst, they’re denying any responsibility.”

Another investor named Choi said she knew nothing about corporate bonds before she was approached by a broker in August.

“I entrusted the savings that I have scraped together for the past three years because the broker told me that the interest was higher than the bank’s,” Choi said. “They didn’t warn me about the risk. When I consulted with the employee right before the situation unraveled, they told me that the situation would not deteriorate to the point where Tongyang would file for court receivership. But when I called back after they did, the only thing I got was apologies, saying they, too, were blinded by their own chairman.”

Choi said she has trouble going about her daily life due to severe stress from the bad investment.

Tongyang Securities was selling Tongyang affiliates’ bonds with low ratings at yields of 8 percent to 9 percent. In contrast, the interest on savings deposits in banks was 2.63 percent in August, the lowest since 1996 when data was first compiled.

As complaints over investments made in Tongyang by retail investors mount, the FSS for the first time in 15 years decided to pursue an extensive investigation with no time frame.

The last time the financial authority undertook an open-ended investigation was in the late 1990s during the Asian financial crisis.

AA or higher

Market experts say the Tongyang crisis will make investors further recoil from corporate bond sales, which have been hurting since the collapse of major conglomerates like Woongjin, LIG and STX.

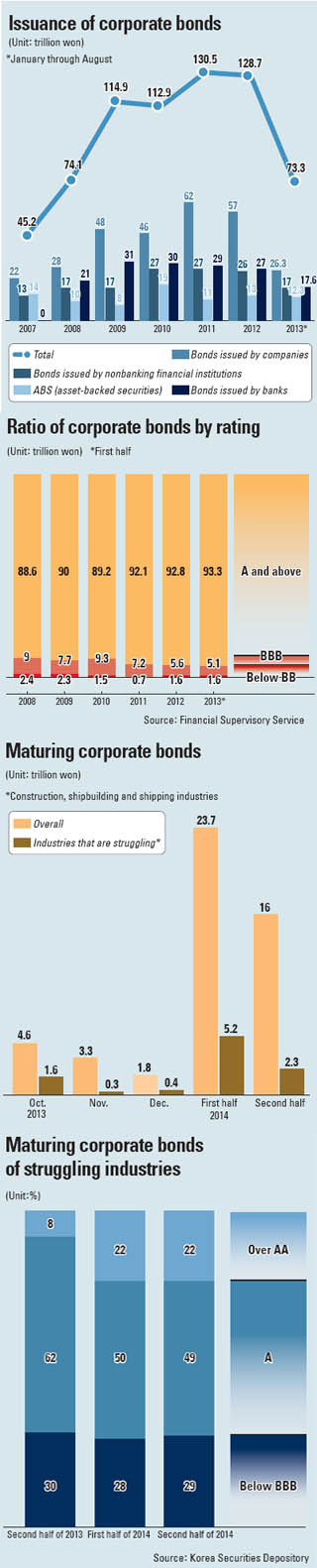

After LIG and Woongjin collapsed and failed to pay their debts, companies started to have trouble finding investors to buy their bonds. And this year after STX also failed to extend its debt with creditors, the corporate bond market further withered with institutional investors starting to look only at companies with credit ratings of AA or above.

A report by the Bank of Korea to the National Assembly last week noted that the polarization of capital inflows and investments between highly rated companies and those in the lower end of the spectrum has been widening.

It added there is a possibility that the local corporate bond market could see another severe investment drought similar to the one in May and June amid speculation the U.S. Federal Reserve would soon taper its bond-purchasing program.

“Due to the Tongyang situation, the woes of companies with lower ratings will likely deepen further,” said a BOK official. “Especially companies that secure capital inflows through the route of corporate bonds and commercial paper will suffer severely.”

The preference for bonds from high-rated companies is also distinctively visible in yields. As of last Friday, AA corporate bonds yielded an average of 5.78 percent more than BBB bonds. At the end of September, the gap was 5.38 percent.

“The widening interest gap shows how much the Tongyang bond situation has affected the market,” said Moon Hong-cheol, a Dongbu Securities researcher.

HMC Investment Securities credit analyst Hwang Won-ha said that due to the recent crisis, the risks for companies in a similar situation as Tongyang - low credit ratings, high credit risks and lack of interest from institutional investors - will increase.

“These are companies that have to rely on attracting retail investors through high interest rates,” Hwang said. “Now the risk of renewing their debt has increased.”

As a result, bonds that are high risk and high yield will see their footprint shrink as investors rush to blue-chip bonds.

Last week, the trading of AAA bonds accounted for 38 percent of all corporate bonds. AA trades were 52 percent and A 8 percent. While the trading of AAA bonds grew, those of A fell.

Ripple effect

The widespread doubt is no longer limited to those with low credit ratings.

Dongbu Steel earlier this month proposed a 10.7 percent interest, two-year maturity corporate bond. Dongbu Steel’s credit rating is BBB and the proposed rate was 1.3 percentage points higher than the 8.7 percent interest the company proposed on an identical corporate bond issued in May. Yet with the situation at Tongyang, many in the market question whether the sale will succeed even with the high 10.7 percent yield.

GS, an AA company, plans to issue 100 billion won worth of three-year maturity bonds, and the market is skeptical of its success.

“Because of the growing doubts over corporate bonds, it’s not easy for companies with ratings above A to issue bonds,” said Hwang Won-hwa, an HMC Investment and Securities analyst. “We will have to see whether it succeeds.”

Earlier this year, only 17 percent of corporate bond sales failed to meet their target. But last month, the rate more than doubled to 36 percent.

At the end of last month, A-rated Hanjin Heavy Industries and Construction paid maturing bonds worth 250 billion won and BBB+ rated Kyeryong Construction paid maturing bonds worth 41 billion won with funds they come up with on their own. Typically, companies pay maturing bonds by issuing new bonds.

Analysts say that this time, the companies didn’t have a choice.

“If the payment on maturing bonds fails because of unsuccessful sales of newly issued bonds, the issuer loses credibility in the market,” said Kim Ik-sang, a researcher at HI Investment and Securities.

Companies that fail to sell bonds to institutional investors usually turn to retail investors. This year, market watchers say, that has been particularly true.

“Most of the corporate bonds with low credit ratings weren’t able to sell to institutional investors,” said Lee Kyung-rok, analyst at NH Investments and Securities.

Retail investors’ holdings of companies in construction, shipbuilding, shipping and other struggling sectors are relatively higher than those with higher ratings.

This month alone, maturing corporate bonds with a rating below A are estimated to be over 1 trillion won. Overall corporate bonds maturing this month are estimated to be 4.6 trillion won.

Government measures

In July, after the corporate bond market showed signs of withering after STX’s problems and widening concern over possible tapering of the U.S. stimulus program, the government introduced measures aimed at easing such anxieties.

The measure announced by the Financial Services Commission was to provide 6.4 trillion won in liquidity to help companies struggling due to low credit ratings. The plan was to issue primary collateralized bond obligations (P-CBOs) worth 6.4 trillion won between July and December 2014. The P-CBOs will allow state-run financial institutions, mainly Korea Development Bank (KDB), to purchase 80 percent of companies’ maturing bonds.

However, even then many market experts were skeptical on whether the measures would have a long-term effect on making corporate bonds more attractive to investors.

One analyst who asked for anonymity said the government measure was not effective and that the Tongyang crisis has only served to reinforce investors’ doubts about corporate bonds.

By Lee Ho-jeong [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)