Household debt looms large

While the world monitors when the U.S. Fed might start winding down its stimulus program, concerns are rising over the impact it will have on a Korean economy with massive household debt.

Tom Byrne, senior vice president of Moody’s Investors Service, told reporters in Seoul yesterday that he expects economic growth to accelerate.

“We see Korea’s growth picking up relatively substantially over the next year or so,” said Byrne. “We’re a little bit conservative at 3.5 percent, perhaps more than that. Korea’s potential growth rate is probably about 4 percent - at least that’s how the IMF and research institutes have looked at it.”

Byrne said that a boost in the Korean economy depends on whether export demand remains strong, adding that conditions in the United States are gradually improving and that the European Union will exit from a recession.

Stephan Long, managing director at Moody’s, echoed that concern, saying “there’s fairly high household debt” in Korea, which poses risks to financial institutions.

“Ratings for Asian banks in general are relatively high and have been stable,” he said. “However, many Asian banking systems have seen rapid credit growth and elevated housing prices. Consequently, asset quality will be tested as loans season and monetary conditions eventually tighten once Fed tapering begins.”

A similar concern was raised earlier by the Samsung Economic Research Institute.

In a report released earlier this month, the think tank projected that the tapering will magnify the threat of household debt.

“Foreign investor presence in the Korean bond market has increased,” said Jeong Young-sik, a senior analyst at SERI. “As a result, the relationship between U.S. interests and Korean interests has gotten closer.”

The analyst said once U.S. interest rates go up, Korea’s will follow, further exacerbating the debt problem.

SERI projected that ending quantitative easing will raise the yield on 10-year U.S. Treasury bonds. If the interest rate rises 1 percentage point, it would likely add 11.1 trillion won ($10 billion) to interest payments by households and 14.5 trillion won to payments by companies.

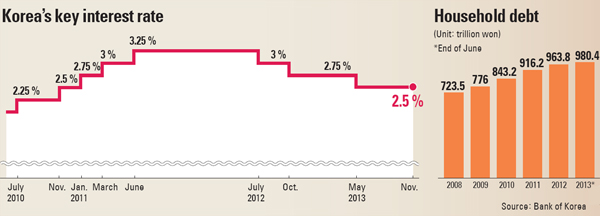

The debt burden of households has already exceeded the OECD average.

The debt ratio of loans to disposable income has grown from 137.5 percent in 2006, when the real estate market was peaking, to 163.8 percent as of 2012. The OECD average was 136.5 percent in 2011.

This could trigger a major panic in the financial markets with the possibility of elevated defaults.

“The debt soundness - particularly centering on the low-income class and those who borrowed from multiple institutions - will get worse,” the SERI analyst noted.

“Once interest rates go up, it will increase the burden on debt repayment, which will further push down real estate values and contribute to the surge of overdue payments,” said Jeong.

The housing problem has been a menace since the previous administration. Since the government adopted a record-low benchmark rate in 2009 to sail through the unprecedented global crisis of late 2008, household borrowing has risen to record levels every year. And unlike in the past, when loans were taken out for purchases of homes, the lending of late has been used to pay for necessities.

As a result, the Lee Myung-bak administration at the end of its term not only pushed for a restructuring of the insolvent savings bank industry, but pressured financial institutions, including banks, to reduce the number of new loans while converting them to less risky fixed interest rates.

Including mortgages and credit card purchases, household debt as of the first half of the year stood at a record 980 trillion won.

Equally concerning is where those loans are borrowed from.

Currently, borrowing made from individuals with low credit ratings is heavily concentrated in nonbanking financial institutions at high interest rates.

As of 2012, more than 70 percent of the loans borrowed by those with low credit ratings were from nonbanking financial institutions. Only 29 percent borrowed from banks.

“It is urgent to prepare measures against the U.S. Fed’s ending of quantitative easing and heighten risk management and secure capital,” the SERI analyst said. “[Korea] especially needs to aggressively target advanced economies that are seeing a relatively faster recovery than emerging markets.”

Bank of Korea Governor Kim Choong-soo acknowledged the potential impact that the end of quantitative easing could have on Korean household debt and added that the central bank will employee any means necessary to cushion it.

“The market has a tendency to overreact to a policy,” Kim said during a press conference held after the central bank’s monthly monetary policy meeting yesterday. “If there is such a tendency, we will employ every policy means to absorb such impact.”

Recently, there were growing concerns that the U.S. central bank could start tapering its stimulus program as early as next month as various economic indicators - including jobs - have improved recently.

However, such fears eased after Janet Yellen, the next Federal Reserve chairman, hinted through a testimony to the Senate Banking Committee that although the U.S. economy and labor market is improving, the performance still falls short of where it needs to be to start ending quantitative easing.

“A strong recovery will ultimately enable the Fed to reduce its monetary accommodation and reliance on unconventional policy tools, such as asset purchases,” said Yellen. “I believe that supporting the recovery today is the surest path to returning to a more normal approach to monetary policy.”

Meanwhile, the Korean central bank kept the key borrowing rate at 2.5 percent for the sixth consecutive month.

BY LEE HO-JEONG, LEE EUN-JOO [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)