U.S. tapering threatens world

Kim Jong-soo

Argentina, Turkey and other fragile emerging economies with questionable levels of current-account deficits and foreign reserves as well as short-term borrowing have all been on the watch list since last year. Stock and foreign exchange markets in emerging economies have been shaken up by capital flight ever since the U.S. Federal Reserve Chairman Ben Bernanke hinted that the U.S. central bank would phase out its stimulus program in May last year. These economies have benefited from a rush of international funds armed with ample U.S. dollars seeking higher returns. They are now devastated by the run on foreign funds with stocks falling like leaves and currencies rising fast. The situation is not as violent as the Asian currency crisis in 1997, but it is nevertheless dangerous.

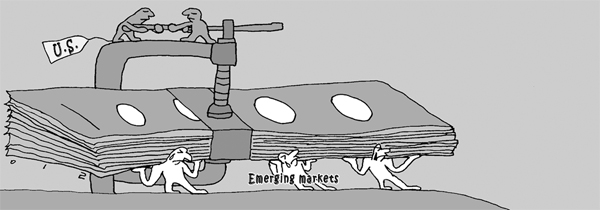

The unprecedented era of easy money began in 2008 after the U.S. monetary authorities took extreme stimulus action to respond aggressively to the Wall Street-sparked global financial crisis. While keeping the key interest rates at the rock bottom rate of zero percent, the U.S. central bank pumped out nearly a limitless amount of dollars to purchase financial institutions’ bonds every month. Through the three stages of the quantitative easing program, the United States poured out nearly $3 trillion. Those dollars, in just a few hours, sprawled out across the world in a parade of the mighty power of the greenback. They stormed into emerging markets in a quest for higher returns. The benefits of monetary easing not only helped the U.S. economy, but inflated stock and bond prices in emerging economies. The world had become accustomed to riches from forcibly contained interest rates and a stock boom from loose liquidity. Though extreme and exceptional, U.S. quantitative easing was taken for granted.

The wake-up call came from the chief of the U.S. central bank. Bernanke announced that if the stimulus program fulfilled its mission, the bank would incrementally end the usual procedures. He was merely talking about the eventual end to all of the Fed’s special steps, yet global markets grieved as if the party was over. Emerging economies should have woken up then, but the sweet taste of easy U.S. money had been too addictive. Toward the end of last year, the U.S. Fed finally announced the time had arrived and that tapering would start in January. When the party ended and guests began to exit, the vulnerabilities and fragility of weak economies were left exposed.

The countries that were slow in restructuring and had structural current-account deficits, political instability and corruption were lined up in a firing line. Argentina, Turkey, South Africa, Brazil, India, Indonesia, Hungary, Chile and Poland were all cited.

The U.S. monetary stimulus that had aimed to help the world’s largest economy combat the economic crisis turned out to doom emerging economies. The U.S. move to phase out its emergency action triggered crises for fragile economies that had been sustained by temporary foreign capital. The world had never experienced such drastic beggar-thy-neighbor results from an economic move by a country in crisis designed to help itself. But the impact on emerging economies and world markets won’t likely faze and stall the United States in its determination to wind down its monthly bond-purchasing program and end the era of ultra-loose money. More casualties from emerging world are expected to surface as monetary easing scales down.

What emerging economies face today may not be entirely due to external shocks. Many now believe the so-called BRIC countries - Brazil, Russia, India and China - that led the world economy since the mid-1990s have run out of steam. Cheap labor and rich resources no longer guarantee growth because those countries have neither endeavored to restructure nor raise productivity to build the grounds for further growth during their fast developmental stages. The U.S. tapering was only a rude awakening, and a crisis based on structural weaknesses could last for a long time.

There is no concern about the contagion reaching the South Korean economy for now. The Korean economy is sound in every aspect compared with the trouble-rocking emerging markets. But what’s worrisome is the spread of the contagion to other emerging economies. If the emerging sector, which takes up 40 percent of the global economy, is hit by a crisis, the entire world economy will share the pain. Export-reliant local economies will inevitably be hurt. A slowdown in China - Korea’s largest export market - could be a major blow. The government would have to revisit its forecast for a rebound through a three-year plan. The government has few options to fight external dangers. It can only try to contain inflows and outflows of short-term capital. But the economy must quickly be re-oriented to a domestic, demand-led growth paradigm so that it no longer is at risk from overseas factors.

Illustrated by Kang Il-goo

By Kim Jong-soo

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)