Poorer households borrow to live

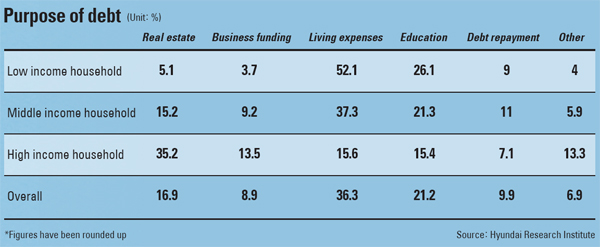

A study by the Hyundai Research Institute released yesterday found that 52 percent of lower-income families’ debt goes to buying necessities and pay bills.

Furthermore, 26 percent of the debt borrowed from such households was used for education. This is a stark contrast to upper-class households, where the largest portion of debt, or 35 percent, was used to buy real estate.

Until now, although debt has been persistently rising since the global financial crisis of late 2008, the government downplayed the risk to financial markets because most household debt was generated by the upper class to buy real estate.

Currently, household debt including credit card purchases is estimated to exceeded 1,000 trillion won ($922.7 billion). As of the third quarter last year, Korean household debt stood at an all-time high of 992 trillion won.

The biggest reason behind the rising debt burden turned out to be a slow expansion of income.

Borrowing by lower-income households at financial institutions grew 2.2 percent from 25.8 million won in 2012 to 36.7 million won in the following year.

However, disposable income during the same period shrank 5.4 percent, from 9.3 million won to 8.8 million won.

As a result, their debt accounted for 414.8 percent of their annual disposable income last year, compared to 276 percent in 2012.

During the same period, the percentage of debt to disposable income for middle-income households grew 2.5 percentage points to 152.4 percent, while for upper-income families it grew 1.6 percentage points to 156.8 percent.

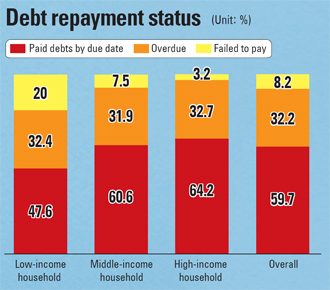

In other words, the burden of debt repayments for lower-income households is much heavier than that of middle- and upper-income families.

The debt interest payment burden of lower-income households also has increased, whereas that of middle- and upper-income families dropped during the same period.

Interest payments accounted for 21 percent of disposable income, compared to 13.8 percent in 2012. During this period, interest payments for middle-class households dropped from 7.9 percent of disposable income to 7.7 percent.

It was the same for upper-income households, whose debt interest payment from 8.2 percent of disposable income to 7.6 percent.

“The upper- and middle-income classes are paying up their principal, which is easing their debt burden,” said Kim Kwang-seok, an analyst at Hyundai Research Institute. “The situation for lower-income families is concerning, as they could be stuck in a vicious cycle because the amount they are borrowing to pay for their living expenses is increasing at the same time their interest burden is rising.”

Kim particularly noted that the lower-income families are struggling to repay their debt on time since most of their debt are used for living expenses with no additional income.

Among lower-income debtors, who are late on their payments, 44 percent blamed it on their lack of income.

The analyst said creating measures specifically designed for different income levels is important.

In particular, measures for lower-income classes should be targeted at improving their income by offering stable and secure jobs, attracting them to less burdensome debt programs to improve their credit ratings and adjusting their debts.

BY LEE HO-JEONG [ojlee8@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)