Retirement pay often spent early

The workers who received their payments before they had actually left the work force had either moved to a new job or received an interim payment by asking to take back money they had put into a pension plan.

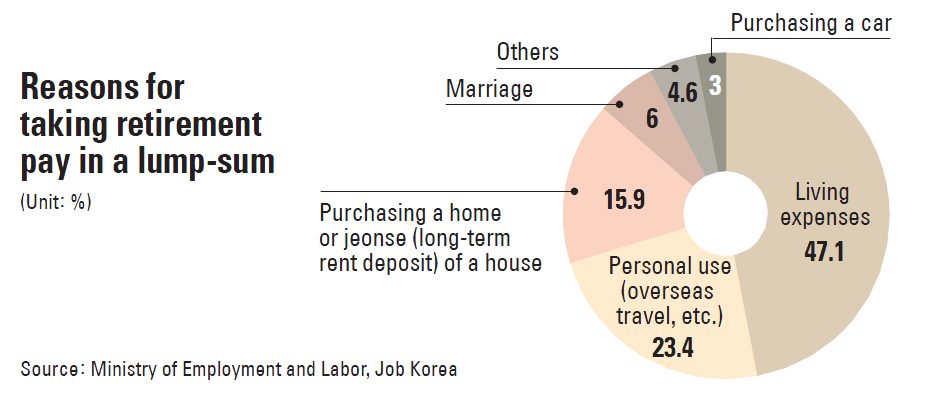

According to a survey last month of 2,950 workers over the age of 20 conducted by the Ministry of Employment and Labor and online job portal Job Korea, about 46 percent who received a lump-sum early retirement payment said they wished they had saved the money instead.

Of the respondents, 94 percent said they considered retirement pay an important source of income for when they are older, but they said they had no choice but to spend the money before retiring due to high housing prices and household debt.

The survey showed that the retirement fund being depended on most was the national pension. About 61.8 percent said they will rely most on their national pension, followed by private pension plans (54.6 percent), savings and investments (48.8 percent) and retirement pension plans offered by an employer (31.8 percent).

Despite financial burdens, experts warned that workers should invest more in life after retirement and recommended subscribing to a pension plan besides the national pension. The government pension for people older than 65 is about 450,000 won ($436) per month, which isn’t even half of the average retiree’s living cost of 1.3 million won.

“Workers should urge their employers to subscribe to a retirement plan, because about a quarter of them end up not receiving retirement pay,” said Kwon Hyuk-tae, director general of the ministry’s working condition improvement division.

“Also, if young workers receive their retirement pay in a lump sum and use it up, their retired life will be financially difficult, which can be a serious issue in the fast-aging Korean society.”

Kwon added that the Labor Ministry and financial authorities are preparing to revise a 2012 law to require private employers to make a pension plan available to their workers.

Under the current law, only public servants and employees of state-run organizations are promised a retirement plan. The law also prevents workers from taking out interim payments on their retirement or from taking a one-time lump-sum payment when they retire.

There is no penalty for not subscribing to a pension program, so some companies refuse to give any retirement pay, using bankruptcy or unstable finances as an excuse.

Large companies are more likely to use a pension plan, while smaller companies are not.

As of March this year, about 87 percent of Korean companies with more than 500 employees paid for retirement via a pension program, compared to only 15 percent of companies with less than 300 employees, according to the Financial Supervisory Service.

BY KIM JI-YOON [jiyoon.kim@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)