Funds and REITs building muscle

On Oct. 15, more than 10 institutional investors crowded into the room to bid for the Jeongdong Building in Jung District, central Seoul. Igis Asset Management offered 270 billion won ($244 million) and is in the process of purchasing the property. Samsung SRA Asset Management, which bought the Jeongdong Building in March 2010 for 178 billion won, will realize profit of nearly 100 billion after only five years.

In July, a real estate investment trust (REIT) managed by Saengbo Real Estate Trust bought the Taeyoung Engineering and Construction company building as a 103.1 billion won sale-leaseback deal.

Real estate funds and REITs have become the biggest investors in the local real estate market, and they are particularly interested in office buildings valued at 100 billion won or more.

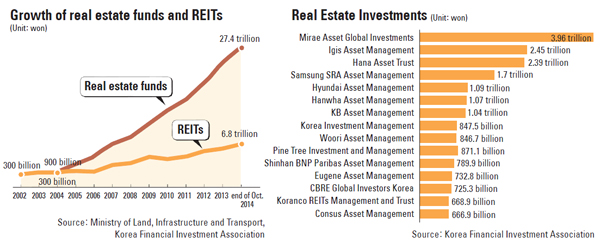

As of October, real estate funds and REIT investments were estimated to have assets of about 34.3 trillion won, with 27.5 trillion won of that in real estate funds and 6.8 trillion won in REITs.

The total amount of real estate investment in major commercial properties would be much more if overseas investment funds are included.

Although most real estate funds and REIT investments focus on properties that promise stable lease income such as hotels and commercial facilities, market experts project they are likely to advance to midsize and small properties like apartments that can be rented out.

As fund and REIT investment continues to grow every year, its influence on the real estate market is expected to expand as well.

Real estate funds have seen a significant increase, considering they totaled only 900 billion won 10 years ago. Additionally, REIT investments also have grown significantly as they amounted to 300 billion won when they were introduced to Korea in 2002.

REIT-management businesses mostly eye large commercial buildings, but they are also interested in small and midsize properties like urban lifestyle housing.

Asset management companies that handle real estate funds are more focused on project financing and commercial building rentals.

But lately, as project-financing capital has struggled to find new opportunities due to limited infrastructure and industrial projects, real estate fund investments have been focusing more on commercial buildings that offer less risk thanks to rental income.

Large investments have been flowing into the purchase of major commercial buildings. In the second quarter, eight large structures in Seoul were sold, including the Cigna Tower, Central Place and the Mirae Asset Life Insurance building.

Sales of these buildings amounted to more than 1 trillion won, which is a 43 percent increase compared to 700 billion won in the first quarter.

The amount in the third quarter dipped from the second quarter. However, 13 major buildings were sold, including the Hyundai Securities Building in Yeouido and the Seorin Building in the heart of Seoul in Jongno District. The combined value of the purchases was 900 billion won.

In the past, buyers and sellers of office buildings were predominantly private companies, particularly conglomerates.

Before the economic crisis, companies bought properties to either expand their office space or business operations, not to lease out. There were some wealthy individual investors who would buy and then rent office space.

It has only been since the late 2000s that asset management companies and REIT management companies started to take over commercial property markets.

Many companies were interested in the property market largely because it was an easy way for conglomerates to expand their assets as real estate values steadily rose. They also wanted to show off their power and wealth to competitors.

But the situation today has changed.

Companies are selling off their properties as real estate values are either stuck in a limbo or falling. Some are selling to secure funds, but most are selling because it is more profitable to expand their businesses than be stuck with real estate whose price hasn’t changed much.

Retail giants like Lotte Shopping and Homeplus have been selling their property to adjust their business strategies. Retailers are using funds from the sale of larger properties to invest in establishing a wider network of smaller stores.

Lotte Shopping has sold two department stores and seven discount marts for about 600 billion won, and it recently signed a memorandum of understanding with Capstone Asset Management worth 500 billion won to sell more department stores and marts.

The returns from these major investments differ. Sometimes it can be more than 40 percent, but in the majority of cases it is 5 to 7 percent.

Of course, there are some that end up losing money. Usually, profits are made either from leasing or reselling the property. Asset management companies tend to hold their real estate investments for three to five years.

Currently, there are 20 or so asset management companies that handle real estate funds, with about half being more active. It’s not difficult for asset management companies to create a real estate fund, as it only needs to be reported to the Financial Services Commission.

Currently, there are 90 or so companies that handle REITs.

Fund managers and investors today seem to have turned their eyes to overseas properties, as markets like the United States see real estate recovering.

“Mirae Asset Global Investments recently bought [the Wacker Drive] office tower in Chicago for $218 million,” said Choi Jae-kyun of ShinYoung Asset. “Samsung SRA Asset Management bought the Pinsent Masons office building in London for $215 million and is pushing for a 190 billion won investment in the Four Seasons Hotel in Hawaii.”

The real estate investment business can be lucrative for management companies. They collect 0.3 percent as a management fee annually and 1 to 2 percent commission when properties are bought and sold, as well as an additional 10 to 20 percent of the profit at the time of the sale.

So what influence do real estate funds and REITs have on the local real estate market?

Market experts say they provide stable growth, cushioning the blow when the market quickly freezes and keeping transactions going when the market spirals downward.

However, they also have a side effect. Reckless competition by asset management companies could end up excessively heating up the property market and these companies also could collude in fixing rent prices to maintain a certain level of profit and keep rents high.

“When management firms have a large influence, the property market could be distorted as they end up trading major properties among themselves,” said Kim Hyo-yeol, a real estate consultant.

BY CHOI YOUNG-JIN [eunjik@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)