Fixed-rate loans prove a bad deal

Two years and seven months later, Kim’s frustration is only growing as interest rates continue to fall.

“I found out that the rate now would be around 3 percent with the same conditions,” Kim said. “My bank says I can get 4.45 percent at best because I am an existing customer.”

As interest rates continue to fall, people who took out fixed-rate loans a few years ago are objecting to the government’s plan to expand the proportion of fixed-rate loans compared to floating-rate loans next year.

The government first encouraged consumers to choose fixed over variable-rate loans in June 2011 to try to manage the nation’s rising household debt. But since then, the interest rate has been falling.

Mr. Cho, a 40-year-old company employee who signed a contract to buy an apartment, is pondering over interest rates proposed by his bank. The fixed rate offered by the bank is 3.1 percent and the variable rate is 2.7 percent.

“I was going to choose the fixed rate without hesitation, especially when the benchmark rate is at rock bottom, but the current situation isn’t what I expected,” Cho said.

“I should make up my mind before January,” he said, “but it’s not easy to make a judgment about future rate changes.”

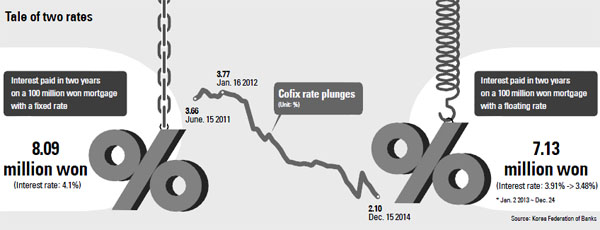

The Cofix rate, set by the Korea Federation of Banks, is a base rate for loans issued by commercial banks. The rate was 3.66 percent in June 2011, but has plunged to 2.1 percent as of Dec. 15.

Although the Bank of Korea announced on Wednesday that the central bank will maintain its current loose monetary policy, consumers are confused about what to do.

According to the Financial Consumer Agency (FCA) on Thursday, the total amount of interest paid by debtors on fixed-rate loans for the past year stood at 83 billion won. It was estimated that they paid more than those who took out variable-rate loans.

“From a long-term perspective, the government’s plan to expand fixed-rate loans is right,” said Cho Nam-hee, president of the FCA. “But the way the government has implemented the plan is wrong. Increasing fixed-rate loans should be used as a measure to encourage competition among commercial banks when the interest rate is rising. Now the banks are recommending their customers fixed rates just to meet government guidelines.”

The financial authority has a goal of raising the proportion of fixed-rate loans to 40 percent by 2017, and is putting pressure on the banks.

According to data by the Financial Services Commission and the BOK, fixed-rate loans accounted for 0.5 percent as of December 2010. The percentage rose to 20.9 percent as of September. But most of the fixed-rate loans were not purely using fixed rates. Banks have been using a trick in which they offer a fixed rate for a certain period of time, and then automatically change to floating rates.

“Forcing banks to meet the percentage required by the government isn’t good,” said Oh Soon-myung, chief of the financial consumer protection bureau at the Financial Supervisory Service. “A desirable way is to increase choices for consumers by letting banks compete with a variety of loans.”

BY CHO HYUN-SUK, PARK YU-MI [ssh@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)