For Korea Inc., 2015 is a year for restructuring

Samsung headquarters in Seocho District, southern Seoul, left, and Hanwha headquarters in Jangyo-dong, central Seoul. The two chaebol made a memorable deal on Nov. 26. [JoongAng Ilbo]

Global companies change their spots by throwing out unpromising or out-of-date businesses. IBM gave up the computer business and was reborn as a consulting and software company.

The strategy of “select and focus” is becoming common among Korea’s family-run conglomerates, which previously believed in bulking up their size by starting new subsidiaries. With an uncertain global economy, the chaebol are now actively reorganizing their business portfolios while trying to find and nurture future growth engines.

More corporate restructuring is likely in 2015, whether it’s selling or merging affiliates or slashing work forces.

“As most of Korean industry has reached a saturation stage, companies that haven’t found new growth engines are likely to reorganize their business portfolios and restructure their work forces,” said Hwang In-hak, head researcher at the Korea Economic Research Institute (KERI).

Learn from others

There are already conglomerates that missed their “golden times” to reinvent themselves, and the outcomes have been painful. Industry insiders said that the disbanding of STX and Tongyang Group in 2013 was a wake-up call for chaebol to change.

For Tongyang, one of the top 10 conglomerates in the past, a weak financial structure forced the group to rely on short-term loans and issue corporate bonds or commercial paper (CP). That eventually led Chairman Hyun Jae-hyun to be charged with fraudulently issuing and selling financial products.

“As for Tongyang, the group didn’t have a clear business model after the profitability of its cash cow - the cement business - went down,” said Moon Chang-ho, who leads the ratings department at the Korea Investors Service.

“The fall of these groups demonstrates that conglomerates should get rid of the ‘too big to fail’ notion, and should be a wake-up call to other companies to restructure themselves quickly if they face any similar problems.”

So far, Hyundai has executed 92 percent of its 3.3 trillion won ($3 billion) cash-raising plan and has been the most active group in transforming itself. The plan included sales of its three financial affiliates - Hyundai Securities, Hyundai Asset Management and Hyundai Savings Bank. The chaebol run by Chairwoman Hyun Jeong-eun has decided to base the group on logistics, machinery and business with North Korea.

Hanjin Group, Korea’s ninth-largest conglomerate and owner of Korean Air and Hanjin Shipping, also completed about 80 percent of its 5.5 trillion won plan, with a big chunk of money coming from a sale of shares in Korea’s third-largest refiner, S-Oil. The group is currently under a public relations cloud after the infamous “nut rage” incident involving former Vice President Cho Hyun-ah, who is also the oldest daughter of Chairman Cho Yang-ho. Apart from the scandal, the company is slowly emerging as a logistics giant.

Dongbu has long way to go as it only secured about 1 trillion won of its 3 trillion won cash-raising plan by this year. The group, run by Chairman Kim Joon-ki, might remain a finance-based chaebol as its core nonfinancial affiliates, which account for 40 percent of the group’s revenue, are up for sale or have been sold.

Dongbu Engineering and Construction, Korea’s 25th-largest builder and the original company of the group, had to file for court receivership on Wednesday. Analysts said that Dongbu shows that time is critical in restructuring. The group’s liquidity crunch stemmed from a slump in the steel and construction industry.

“Companies have to raise their competitiveness through R&D investments, but that takes a long time and as China is closing in on Korean companies these days, we don’t have much time,” said Chang Suk-In, a researcher at the Korea Institute for Industrial Economics and Trade (KIET). “Companies should conduct reviews of their business portfolios quickly and transform themselves.”

In Korean industrial history, there were times when many companies had to overhaul their business portfolios by cutting out struggling businesses and make deals with other companies. That happened in 1998, when the Asian financial crisis hit Korea particularly hard.

More than half of the country’s 30 conglomerates had to go through debt workout programs or declare bankruptcy. Daewoo Group, which was Korea’s No. 2 chaebol, saw its empire scattered to the wind.

Experts said the restructuring movement these days reminds them of 1998, although the background and process are a little different.

“As big deals in the past were forced by the government, these days restructuring is voluntarily done by each group for the sake of survival,” said Bae Sang-kun, vice president of KERI. “They now have the mind-set that even a slight hesitation to restructure can lead to their downfall.”

For many conglomerates, the easiest way of restructuring has been merging affiliates that do similar business, a way to save costs and slim down for quicker decision making.

Korea’s No. 1 chaebol Samsung has been one of the most active groups in integrating affiliates in recent years.

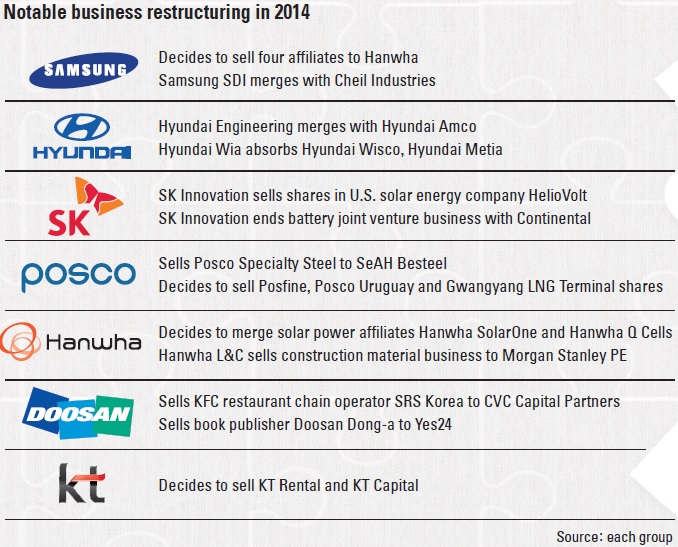

The group, headed by Chairman Lee Kun-hee, who has been hospitalized since May, had Samsung Everland (now Cheil Industries) sell its building management business to its security service affiliate S1 in 2013, while merging Samsung SDS and Samsung SNS.

Last year, it integrated Cheil Industries’ material business unit with battery maker Samsung SDI. The group also tried to merge Samsung Engineering and Samsung Heavy Industries, but that was cancelled due to opposition from shareholders.

No. 2 conglomerate Hyundai Motor was also aggressive in 2014, merging its construction affiliate Hyundai Amco and Hyundai Engineering, while Hyundai Wia absorbed its parts-making affiliates Hyundai Wisco and Hyundai Metia.

The world’s fifth-largest automotive group also made Hyundai Steel absorb Hyundai Hysco’s cold-rolled steel business, which boosted its competitiveness in automobile steel sheet development. It also merged its system integration affiliate Hyundai AutoEver with Hyundai C&I.

But what really signaled that restructuring was going on in earnest was the big deal between Samsung and Hanwha that was announced on Nov. 26.

The two conglomerates surprised the market by saying that Samsung’s defense and chemical affiliates - Samsung Techwin, Samsung Thales, Samsung General Chemicals and Samsung Total Petrochemicals - would be sold to No. 10 chaebol Hanwha Group.

Since Samsung hasn’t sold its business units since the late 1990s and the size of the deal was 1.9 trillion won ($1.7 billion), it was considered one of the biggest corporate deals between conglomerates in decades. The deal is expected to be finalized in the first half of this year.

What surprised people was that the two conglomerates made the deal voluntarily and the companies up for sale weren’t weak or uncompetitive, but still had the potential to grow.

“Samsung’s last company in line can be a front-runner for Hanwha,” said Bae. “Restructuring ‘zombie companies’ is important, but there should also be an effort to reposition good companies in an industry.”

Experts said it was a win-win deal for both sides. For Samsung, the deal allows the group to focus on IT/electronics, finance and heavy industries, while Hanwha can step up as the No. 1 player in the defense and petrochemical businesses.

“U.S. companies have been growing their competitiveness through M&As and reorganization of business portfolios,” said Ha Tae-hyung, head of the Hyundai Research Institute (HRI). “As the advantage of ‘select and focus’ is highlighted, big deals between corporations should become a new trend.”

Others conglomerates are trying to find the right business portfolios.

Posco, the nation’s sixth-largest conglomerate, is selling its affiliates to reduce its size and focus on what it’s best at: steelmaking. Chairman Kwon Oh-joon, who took the helm in March, has said that the group will review all new business projects.

Korea’s largest steelmaker is trying to sell its liquefied natural gas (LNG) terminal at the Gwangyang steel mill; Posfine, a slag powder producer; and its forest products company Posco Uruguay. It already inked a deal with SeAH Besteel to sell Posco Specialty Steel.

Last year, Doosan, Korea’s 12th-largest conglomerate, sold its book publishing affiliate Doosan Dong-A to online bookstore Yes24. It also sold SRS Korea, which manages the KFC restaurant chain in Korea, to the European private equity firm CVC Capital Partners. The group, which previously owned the Burger King franchise in Korea and a brewery business, has transformed itself into a heavy industries and machinery conglomerate.

However, analysts said selling off affiliates is not the only answer in restructuring. In fact, both Posco and Doosan made investments in future growth engines. While Posco acquired coal power generator Tongyang Power, Doosan last year bought two fuel cell manufacturers.

“Companies’ business portfolio reorganizations have been mainly focused on increasing efficiency of management, but for the sake of the future it should be conducted in a way to find future growth engines,” said Baek Heung-gi, a senior researcher at HRI. “They should actively use M&As as a way to build revenue sources in new markets.”

Analysts said the widening industry trend of “select and focus” pushes companies to even sell good companies if they don’t fit into a future business plan.

For example, Hyosung last year sold its PET packaging business unit to Standard Chartered PE for 415 billion won. Hyosung’s packaging business, which makes PET bottles for beers and other drinks, controlled the No. 1 market share (30.5 percent) with an operating profit ratio reaching two digits.

Work forces are wary

While making adjustments to business structures is a smart way to survive, it doesn’t always go smoothly. In particular, employees worry about job stability when a lot of restructuring goes on in difficult economic times.

Already, employees of Samsung Techwin and Samsung Total Petrochemicals formed a union and opposed the mega deal with Hanwha. Some 1,500 employees of Samsung Techwin held a rally on Dec. 16 at its plant in Pangyo, Gyeonggi, holding picket signs reading, “Not for sale.”

Although Hanwha has promised to maintain the jobs of the Samsung employees, they are worried that the group might reposition or transfer their jobs after the acquisition is done. In addition, adjusting to a new corporate culture and giving up the pride of being a Samsung employee are big concerns.

“A company buys another company because it covets the technology, infrastructure and talented work force, but if no employee wants to join, there is no meaning,” said a spokesman from Hanwha. “We are confident that we can cooperate and create synergy by making a better corporate culture.”

But anyone who can maintain a job is lucky in a time of restructuring. Hyundai Heavy Industries, which posted more than 3 trillion won in losses last year, shed 81 executives - or 31 percent - as a part of its restructuring plan.

As for KT, Korea’s second-largest mobile carrier, more than 8,000 workers left the company in April on a voluntary retirement basis. Its executives also were reduced about 30 percent since Chairman Hwang Chang-gyu took the helm last January. The group is also restructuring by selling units like KT Rental and KT Capital.

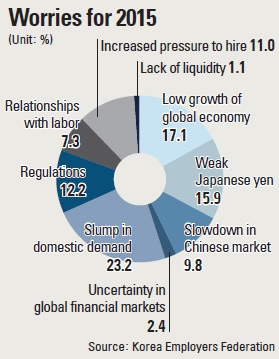

Mergers or sales of affiliates means that jobs can be reduced. A recent survey by the Korea Employers Federation showed that 51.4 percent of conglomerates have said they are planning retrenchments this year.

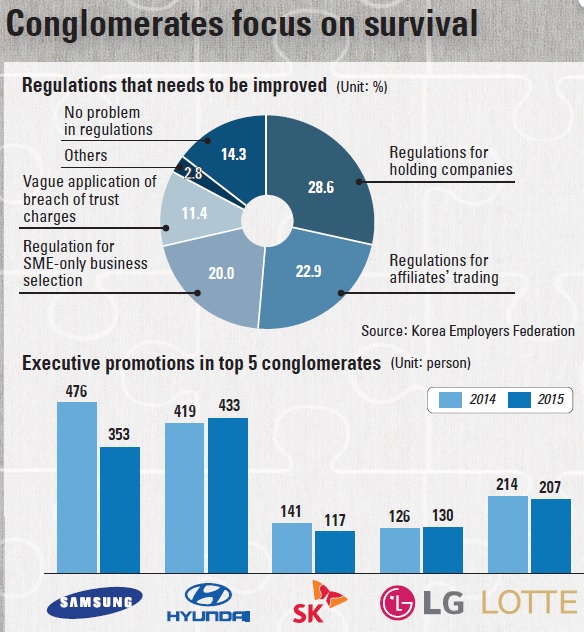

The fear of work force restructuring is even felt at the No. 1 conglomerate, Samsung. In fact, the executive reshuffle by Samsung for 2015 showed that only 353 people were promoted, which is 123 fewer than in the previous year. Affiliates Samsung Life Insurance, Samsung Securities, Samsung SDI and Samsung Electro-Mechanics all ran voluntary retirement programs in 2014.

“In global competition, you can’t blame companies for restructuring on their own,” said Bae from KERI. “But the issue of cutting the work force can lead to weak domestic demand that impacts the local economy, so companies should be more considerate.”

Government to give aid

While uncertain and difficult economic times are pushing companies to restructure, the government is also stepping up to help companies in the process.

In its 2015 economy policy plan announced Dec. 22, the government said it has planned a special law that helps companies restructure. In the first half of this year, the government will give orders to research institutions to examine the issue and will form a task force.

The law is widely referred to as the “one shot” business reinvigoration law, which benchmarks Japan’s business revitalization law from 1999. The Japanese law has facilitated more than 500 business restructurings.

The government is claiming that the new law would especially help those manufacturers that are having a tough time in the global market, squeezed by the weak yen and the rise of China.

The ultimate goal is to provide a shortcut for business restructurings in two ways. The law is expected to allow acquisition and registration tax cuts for companies that eliminate underperforming affiliates or rearrange their business units overall. It will also encourage mergers and acquisitions by cutting in half the Fair Trade Commission’s screening period, which currently makes companies wait as long as a month.

Not surprisingly, companies are welcoming this “one shot” law. Companies in struggling industries like shipbuilding and construction hope the law can help them specifically.

“There are still some regulations to be eased, but a plan to adopt this law shows that the government has a strong will to revive the Korean economy and help corporate management,” said an official from the Korea Chamber of Commerce and Industry. “As many Japanese companies benefited from a similar law, the government should make this law quickly and the National Assembly should pass it quickly.”

Experts say it’s about time the government makes a conducive environment for companies to restructure. “In order to have market-friendly restructuring, the government playing a certain role is essential,” said Lee Myung-ho, who directs corporate structure improvement policies at the Financial Supervisory Service.

BY JOO KYUNG-DON [kjoo@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)