Medical insurance delay a pain for consumers

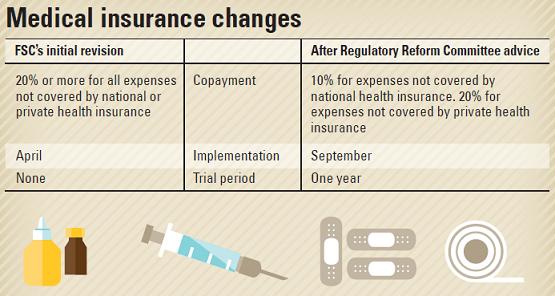

The Financial Services Commission (FSC) in February announced it would revise the bill on insurance law to make co-payments at least 20 percent of the cost of medical services, compared to previous regulations that allowed co-payments of 10-20 percent.

The financial authority justified the move by saying low co-payments encourage subscribers to get unnecessary medical treatment or services and that results in higher premium costs.

However, insurers still sell medical insurance with the 10 percent co-payments because the revised bill has been approved only by the Regulatory Reform Committee made up of experts from academia, business and government. The FSC on Thursday announced it will implement the new co-payment standard in September, five months later than planned.

“As I was told that I didn’t have much time, I didn’t have the opportunity to meticulously compare different insurance policies,” said Shim. “I feel like I was duped in a marketing scheme.”

Insurance companies were the only ones to profit from the government’s indecisive policy implementation.

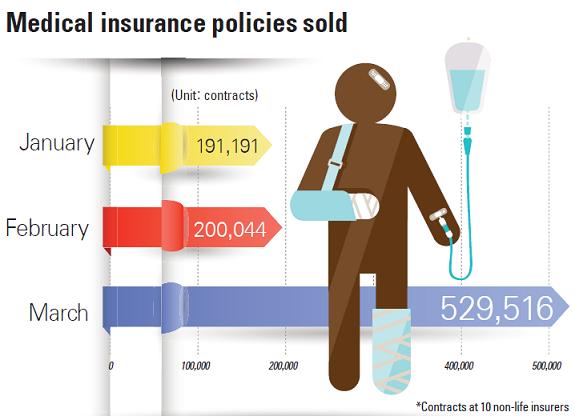

The number of new medical insurance policies sold by 10 non-life insurance companies was 190,000 in January and 200,000 in February, then skyrocketed to 530,000 in March.

“Insurance companies are likely to hold large-scale marketing ahead of September,” said an insurance company official, who wished not to be named.

The government faces heavy criticism that its policy execution resulted in profits for insurance companies and confusion for consumers. In fact, there have been questions raised since the FSC’s decision to standardize co-payments, which was deemed contrary to the interests of consumers.

Even the government’s reform committee that reviewed the revised law was skeptical. The reasons the committee did not give the green light right away was because it saw that the FSC needed to collect input from stakeholders, including medical institutions, insurance companies and consumers, since a majority of the population subscribes to private medical insurance.

The reform committee requested a revision of the revised bill, which changed many of the details.

Private medical insurance is a policy that pays a percentage of the cost of treatment that is not covered by national health insurance. Under the initial proposal by the FSC, co-payments would have been at least 20 percent for both those covered by national health insurance and those not covered.

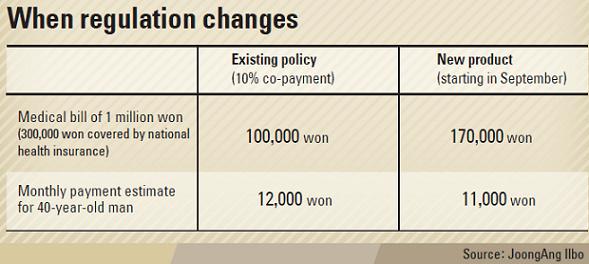

For example, if a patient received a medical bill of 1 million won ($915), that person would have to pay 200,000 won out of pocket, while the insurance company would pay the remaining 800,000 won. But after the committee advised the FSC to make the adjustment, the co-payments would be 20 percent for those not covered by the national health insurance and 10 percent for those who are.

In this case, 300,000 won would be covered by national health insurance while the remaining 70 percent would be covered by the insurance company. And under this system, the patient’s co-payment would be 30,000 won less, or 170,000 won.

Additionally, the committee has told the FSC to include a clause placing a one-year limit on the co-payment rates, since it is unclear whether standardizing the ratio at 20 percent will actually help reduce insurance premiums.

It said it is giving the commission the authority to come up with a measure that would strengthen scrutiny of insurance use by subscribers, which it considers a more fundamental solution to the problem of rising costs.

The FSC also is working on a measure for the Health Insurance Review and Assessment Service to check the appropriate level of insurance coverage on expensive procedures such as MRI and CT scans. But it also is unclear whether that will happen because of strong opposition from the medical community.

“There’s a strong possibility the issue could become a hot potato when it is discussed in the National Assembly,” said an FSC official.

BY CHO MIN-GEUN[lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)