Among stymied Korean banks, the rate of interest in India is on the rise

“Gurgaon is a new city close to the country’s capital where Samsung Electronics, Hankook Tire and a majority of Korean companies are located,” said Sohn Tae-seung, vice president of Woori Bank, who accompanied Lee. “Once we get official approval from the Indian government, we plan to work on opening the new branch by October.”

In April, Kwon Seon-joo, president of the Industrial Bank of Korea (IBK), visited India to participate in a ceremony celebrating the bank’s new branch in New Delhi. IBK received approval by the Indian government last year.

“This is the first branch that IBK has opened up overseas this year,” said an IBK official. “We plan to focus our business on providing various financial services, including loans to Korean small and midsize companies that have entered the Indian market.”

Smaller Korean provincial banking group BNK Financial Group also has taken an interest in India since Chairman Sung Se-whan toured cities, including New Delhi and Chennai, for five days in March.

Korean banking groups’ interest in India has risen. Banks that don’t have a branch there are working with financial authorities on possible locations for new ones.

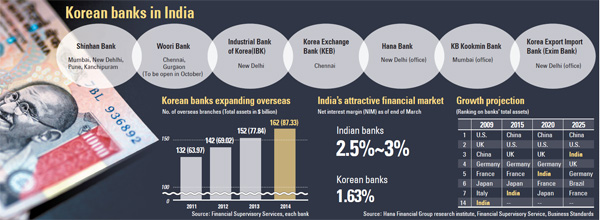

According to the Korean financial industry, nine branches and offices in India are run by Korean Banks. The first to enter the country was Shinhan in 1996. Shinhan now has four branches and offices in India, with the last opening in the city of Pune in December. Korea Exchange Bank (KEB) opened a branch in Chennai in March. KEB’s office in New Delhi, which has been operating since 2008, received approval from the Indian central bank to convert to a branch in February.

Other Korean banks with a presence in India are Korea Export Import Bank and KB Kookmin Bank.

Korean banks are interested in India largely because profitability at home has been eroding under the Bank of Korea’s loose monetary policy as part of the government’s campaign to boost the economy and cutthroat competition.

According to the Financial Supervisory Service, in the first quarter the average net interest margin (NIM), a gauge of banks’ profitability, was 1.63 percent, an all-time low. That’s how much the banks would make after collecting loan interest and paying interest on deposits. The NIM rate was almost the same as last year’s inflation rate of 1.3 percent.

The net interest margin for Indian banks is much larger. India’s average NIM, according to the country’s business newspaper, is 2.5 percent to 3 percent due to strong economic growth. As Prime Minister Narendra Modi has pushed for market-friendly policies, the Indian economy in the first quarter reported a 7.5 percent year-on-year increase. By comparison, China’s posted 7 percent growth in the first three months of the year. This year, Modi plans to increase investment on infrastructure, including power supplies and a new airport.

“The quality of financial industry service in India is relatively low and therefore we would be able to provide various financial services not only to Korean companies, but to local companies,” said Sohn of Woori. “As we expect the economic growth potential to be stronger in India, we plan to open two or three additional branches next year.”

But some experts warn of moving too fast.

“There’s a huge potential for growth as 60 to 65 percent of the population in India is receiving financial services,” said Cho Choong-jae, economist at Korea Institute for International Economic Policy. “However, Korean banks face a lot of competition from Indian banks, including state-run institutions, and a lot of international banks do business there. [Korean banks] need to approach the market through a strict localization strategy.”

BY YEOM JI-HYUN, CHO HYUN-SOOK [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)