Banks see Q2 profits slide

Net interest margin (NIM), a barometer of local banks’ profitability, has hit 1.58 percent, the lowest since the FSS started compiling the data in the first quarter of 2003.

NIM refers to the difference between the interest income generated by banks and the amount of interest paid to their lenders.

NIM has continued to fall since 2010, when the margin recorded 2.4 percent. The key interest rate, slashed to a record-low 1.5 percent in June, has given banks little room to profit.

The FSS estimated local banks’ Q2 net profits at 2.2 trillion won, down 5.4 percent from last year’s 2.4 trillion won.

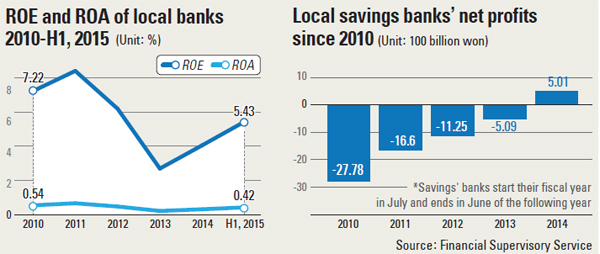

Other key measures of profitability like return on assets (ROA) and return on equity (ROE), also deteriorated in the second quarter, the data showed.

ROA, which indicates how efficiently a company uses its assets to create earnings, has fallen to 0.42 percent, down 0.09 percentage point year-on-year.

ROE, which measures a company’s profitability relative to the money shareholders have invested - has also declined by 1.14 percentage points year-on-year, to 5.51 percent in the second quarter.

ROA and ROE in the first half of the year have improved compared to the first half of 2014, but when compared to their 10-year average, both have worsened significantly, the data showed.

Local banks’ ROA and ROE for the first half of this year were 0.42 percent and 5.43 percent, slightly better than 2014’s 0.31 percent and 4.05 percent. But they were significantly down from their 10-year average (2005 to 2014) of 0.6 percent and 8.04 percent, according to the financial regulator.

In the United States last year, commercial banks’ ROA averaged 1 percent, and their ROE averaged 8.97.

Banks’ interest-related earnings fell 6 percent to 8.3 trillion won in the second quarter of this year, compared with last year’s 8.8 trillion won.

Costs related to bad debts have also risen by 14.6 percent to 2.1 trillion won, from last year’s 1.9 trillion won, as a number of large corporations have entered debt workout programs due to financial troubles.

There were, however, some hopeful signs. Banks have seen an increase in their non-interest earnings, which include commissions from product sales, profits from securities, foreign currency exchange and derivatives.

Non-interest earnings rose nearly 60 percent to 2.5 trillion won, from last year’s 1.5 trillion won, thanks mainly to higher earnings generated from securities.

Eight major commercial lenders, including Kookmin and Hana, saw profits from the sale of their stakes in Korea Housing & Urban Guarantee amount to a combined 0.6 trillion won.

But in the coming quarters and years, banks will face increasingly stiff competition, as the latest set of deregulatory measures will eventually help other non-banks enter the territory that previously belonged to them, analysts say.

“Banks need to find a new source of revenue,” said Sohn Joon-beom, a researcher at Hana Institute of Finance. “They probably need to look to increasing demand for asset management services.”

The brightest spot in the banking sector was savings banks, which posted profits for the first time in seven years.

Local savings banks posted 500.8 billion won in net profits for fiscal 2014, which was a dramatic change from the losses of 508.9 billion won seen the previous year, according to the FSS.

Saving banks start their financial year in July and end in June.

Earnings improvements were due to a huge drop in allowance for bad debts which had been eating into their earnings for years.

Allowances for bad debts have fallen from 1.19 trillion won in fiscal 2013 to 575 billion won for fiscal 2014, down by more than 600 billion won as banks have significantly cleaned up their balance sheets.

Savings banks’ assets also rose 9.4 percent to 40.2 trillion won, while the overall loan delinquency rate has fallen to 11.5 percent from last year’s 17.6 percent.

BY PARK JUNG-YOUN [park.jungyoun@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)