Younger borrowers are big players in mortgage market

Analysis of mortgage loan data by age groups from four major banks - Kookmin, Shinhan, Nonghyup and KEB Hana - shows loans issued to people in their 20s and 30s grew by 28 percent over a two-year period from August 2013 to August this year.

This compares with 13 percent growth in overall mortgage loans during the same period, from 199.85 trillion won ($166.65 billion) in 2013 to 226.44 trillion won in 2015.

The growing numbers are driven by young people who are opting to buy their homes as they are finding it more difficult to manage a jeonse (lump-sum deposit) deal.

Chang, a 32-year-old office worker, is typical of the group. He is living in a double-income household and recently bought a 105.8-square meter (1138.8-square foot) apartment in southwestern Seoul that the family used to rent on jeonse.

With children growing up, moving around has become too big of a hassle for Chang, and the jeonse price, around 350 million won, has neared the sale price. He decided to buy his home and went to his primary bank for a mortgage loan.

For an apartment with an estimated value of 400 million won, with an actual sale price range of around 430 million to 450 million won, he was able to get a 280 million won deal, or 70 percent of the house’s value.

The interest rate was also relatively low in the high-2 percent to low-3 percent range. Over 30 years, he makes payments of 1 million won per month, including interest and principal.

“Finding an available jeonse is as hard as picking stars from the sky, and semi-jeonse lease contracts require 1 million won monthly rents over the security deposit of 100 million won,” Chang said. “I thought it would be better to pay off the mortgage interests with that kind of money.”

“Even if the home price was to fall to 90 percent of the current value over the next 10-year period, I am still better off than paying wolse for the next 10 years,” Chang said.

And there are many more people in the same age group as Chang who are deciding to become home owners.

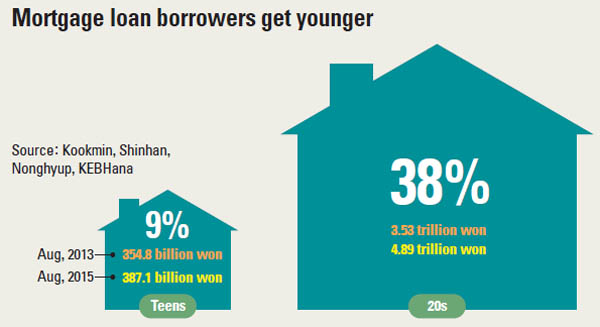

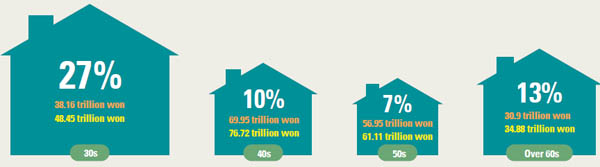

In the two years leading up to August this year, outstanding mortgage loans issued to people in their 20s increased by 38 percent to 4.89 trillion won from 3.53 trillion won, and loans issued to people in their 30s rose 27 percent to 48.45 trillion won from the previous 38.16 trillion won.

This is steep growth compared with the 10 percent loan value growth issued to people in their 40s, who have traditionally been the major buyers.

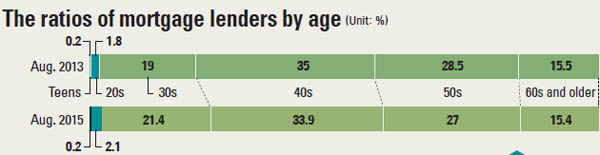

Looking at overall home mortgage loans, amounts issued to borrowers in their 20s and 30s accounted for 23.5 percent of the total as of August this year, rising from the previous 20.8 percent in August 2013. The proportion of loans issued to people in their 40s fell to 33.9 percent from the previous 35 percent and borrowers in their 50s to 27 percent from 28.5 percent.

In the new home pre-sale market, consumers in their 20s and 30s have also become primary buyers.

In July pre-sales at Wangsimni Xi, being built by GS Engineering & Construction in northern Seoul, nearly 47 percent of the buyers were in their 20s and 30s. Just over 24 percent were in their 40s and 22 percent in their 50s.

In the pre-sale of Daewoo Engineering & Construction’s Ansan Central Prugio in Gyeonggi and Daelim apartment in Boryeong, South Chungcheong, more than 30 percent of the people who signed the contract were in their 20s and 30s.

“Just last year, people in their 40s and 50s were major buyers in the pre-sale market, but this has changed this year,” said Shin Byeong-cheol, a senior official in charge of pre-sales with GS Engineering & Construction. “People in their 20s and 30s, who used to account for around 20 percent of the total contracts, now account for as much as 40 percent in some sales.”

Experts say younger people may be less inclined to buy new homes at pre-sale markets after next year.

“From next year, new lending rules that require installment payments of principals will be implemented. This will probably dampen demand from younger people who may find principal payments burdensome,” said Lee Nam-soo, a senior real estate analyst at Shinhan Investment.

Mortgage payment schemes that require only interest payments for the first few years are popular.

There are also worries that young buyers may be purchasing properties at peak prices.

“There is a higher possibility of housing price falls and an interest rate hike [in the near future].

“If and when external economic and financial conditions deteriorate, housing prices could plunge,” said Kim Ji-seop, a researcher at the Korea Development Institute. “One should consider such a scenario when setting up their loan scheme.”

BY KYEONG-JIN, HWANG EUI-YOUNG AND PARK JUNG-YOUN [park.jungyoun@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)