New kind of loan for jobless endures some teething pains

After a lengthy search, he stumbled upon Woori Bank’s WiBee Mobile Loan program, which offers loans of between 1 million won and 10 million won with annual interest rates between 5.86 percent and 9.66 percent, considered mid-range. The best part was he could borrow even without a stable job.

But when he applied for a loan via his smartphone - which explains the word “mobile” in the program’s name - the young college student was disappointed to be told he couldn’t borrow more than 1 million won.

“For people in their 20s, we have a ceiling of 5 million won, which is half of the maximum of 10 million won,” said a Woori Bank official. “And lately the evaluations have become stricter.”

The mobile loan program was introduced in May 2015 and attracted a lot of customers who didn’t have a stable income or a job. It had no choice but to tighten its requirements largely because the number of overdue payments started to rise.

WiBee Mobile Loan program was the first mid-level interest rate loan program offered by a commercial bank. It was considered a blue ocean business - one with great future potential - for a financial market that was polarized between banks, which offered low interest rates but only to only people with good credit histories, and the nonbanking financial institutions like savings banks and loan sharks that charged higher interest rates for people with bad credit histories. Savings banks in Korea are more like consumer finance companies catering to low-income, bad-credit borrowers.

Woori Bank’s mobile loan program is also considered a precursor to products that may be offered by two Internet-only banks the government approved in the second half of last year.

The stricter requirements for the mobile loans has resulted in a drop in the number of applicants.

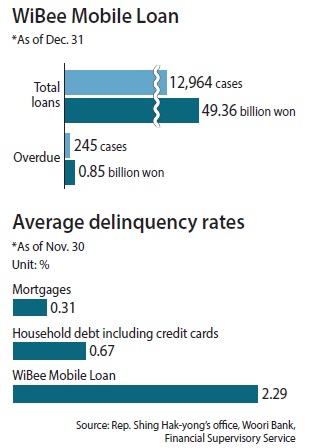

According to a report by lawmaker Shin Hak-yong, who is on the National Assembly’s National Policy Committee, overdue payments for the WiBee loan program were 2.29 percent by the end of last November and hit 3.21 percent in October. This was a stark contrast to the 0.31 percent average of late payments on mortgages. It’s even higher than the 2.19 percent late payment rates at nonbanking financial companies including credit unions. Overdue payments by borrowers in the middle and lower income class exceeded 4 percent.

“The overdue payment rate rose largely because the number of people who borrowed from the mobile loan program were in their 20s and have no stable income,” said an official at the Seoul Guarantee Insurance, a private company that guarantees the loans.

While Woori Bank argues that the overdue payment rate isn’t too high, analysts say an overdue payment exceeding 2 percent in a mere seven months since the product was launched is considered high.

To control the rising overdue payments, Seoul Guarantee Insurance asked the bank to tighten its requirements. As a result the bank reduced the maximum amount that people in their 20s could borrow while reviewing credit card spending details of applicants in their 20s or over the age of 60.

Some worry that Internet banks are going to face the same challenge.

The financial authorities plan to announce several measures that will help bolster the mid-level interest loan market later this week. They are expected to include a measure in which credit evaluations on applicants for mid-level interest rate loans from Internet banks will use Big Data, which should be more thorough than Woori Bank’s evaluations.

“The core idea of a mid-level interest rate loan is that it sets the appropriate level of interest based on a detailed categorization of a person’s credit rating using big data,” said a financial authority official.

BY KIM KYUNG-JIN [kim.youngnam@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)