Push on for fintech-ready loans

Even non-banking financial companies are jumping into the market, as mid-range interest rate products are possible with the rapid development of fintech that uses big data to determine a person’s credit rating by evaluating their spending habits and whether they have a steady income.

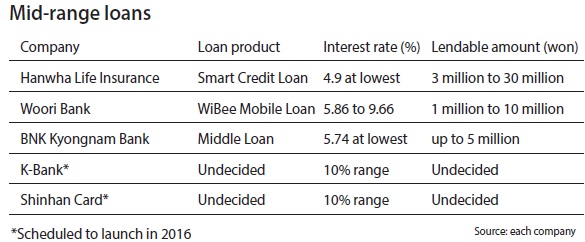

The latest to join the race is Hanwha Life Insurance, which became the nation’s first insurer to offer a fintech-based loan with mid-range interest rates on Wednesday.

According to the insurer, the loan product is targeted at people whose credit rating is in the mid-range, who have trouble getting loans from commercial banks and have to resort to non-banking institutions and high-interest loans. These are people whose credit rating is between four and seven on a scale of one to 10, with one having the best credibility.

Under the insurer’s Smart Credit Loan those in the mid-range credit rating could apply for loans where the minimum interest rate starts at 4.5 percent. This is cheaper than the average 10 percent asked at nonbanking financial companies, including savings banks and credit unions and much lower than the 20 percent or higher offered by private lenders.

The company is planning to make loans available for as much as 30 million won ($24,000) and as little as 3 million won. The loan can be requested through the insurance company’s mobile app, and the credit level of the person applying for the loan is determined based on their health insurance payment records.

Hanwha has developed its own credit assessment model with a local fintech firm, which evaluates the applicant by keeping track of their income and spending patterns via data collected through social media and payment records.

“So far, mid-range lending programs were only allowed for employees of big-name companies or those at listed companies,” said Kim Mi-ho, head of the financial product department at Hanwha Life.

While its 2015 revenue dipped to the minus level to record a net loss due to a tight insurance market, Hanwha eventually aims to make the lending business a future cash cow by opening a loan marketplace in September where borrowers can choose the most suitable mobile lending program.

However, some have questioned whether mid-level interest loans can contribute to improving the insurer’s shrinking revenue structure.

Financial companies are targeting people with mid-range and low credit levels as the official launch of Internet-exclusive banks that the financial authority approved last year - KT and Kakao - is expected to come in the second half.

Woori Bank has already launched its mobile-based WiBee Bank and Shinhan Bank has Sunny Bank, both of which specialize in mid-range loans.

BNK Kyongnam and Gwangju Banks have rolled out mobile loans in the 5 to 14 percent range. Card companies like Woori, Samsung and Shinhan are seeking to launch mid-range loans with a rate below 10 percent by working with data collectors such as banks and telecom carriers.

“Because the big data-based credit ratings system is so new, there are no successful examples yet, and financiers are jumping on mid-range loans after subscribing to surety insurance firms,” said Jung Hee-soo, head of the retail financing research team at the Hana Institute of Finance. “But there are reasons why different financiers are flocking to this. There is enough demand among mid-risk borrowers.”

BY KIM JI-YOON [kim.jiyoon@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)