U.S. private pensions are attractive model here

Hechter earned $130,000 a year and averaged an annual $10,000 in savings in his employees’ retirement plan (ERP) and individual retirement account (IRA). His private pension was boosted by numerous tax benefits, and once he became 50, he was given additional tax reductions.

“I thought it was a little risky to rely solely on the public pension so I started to save a considerable amount of money in my private pension when I started working in the early 1980s,” Hechter said. “I have delayed opening up my private pension for now but if I were to use it, I would be able to maintain a standard of living comparable to the one I had when I was working.”

For many retired Koreans searching for jobs due to insufficient retirement savings, the American private pension system is a dream. The United States has a very developed private pension system even compared to advanced European countries.

The U.S. system is worth $17.4 trillion won, or 53 percent of the world’s private pension market. Considering the United States established a retirement pension plan similar to the private pension as early as 1875, it is no surprise that its pension system is so advanced.

“Americans believe that they should look after themselves during retirement,” Kim Parker, director of social trends research at the Pew Research Center, said. “As a result, the pension system has grown while focusing on the role of private individuals rather than that of the public.”

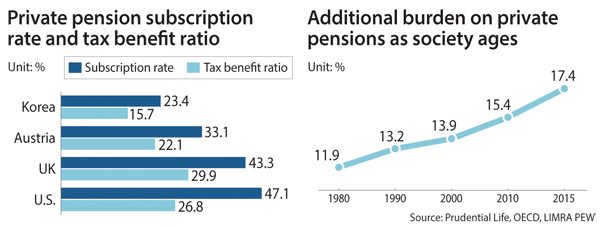

For the United States, the private pension plan is one of the key ways to support its aging society. According to the Pew Research Center, 20 percent of the U.S. population will be 65 years old or older by around 2050. This places a considerable burden on the younger generation. A survey found that 30 percent of people with parents aged 65 or over gave their parents economic support in the last 12 months, while 60 percent said that they had provided day-to-day care for their parents.

This pressure on American families is likely to increase in the next few years as the population ages.

The U.S. government is responding to these changes by offering “catch-up” contributions, or additional tax benefits to people aged over 50 as they prepare their retirement plans. Washington is providing additional income tax reductions to taxpayers even when they do not qualify for regular income tax reductions. People aged 50 and over are permitted an annual $6,500 tax exemption thanks to this policy.

In addition, citizens can withdraw from their private pension funds without being subject to taxation, subject to conditions. They are also being offered pension rewards that exempt taxation on withdrawals of up to $10,000 when they are over 59 years and six months old.

However, the government is taking measures to ensure that people do not take advantage of the system. Should citizens benefit from the “catch-up” policy and cancel or withdraw their private pensions before they turn 59-and-a-half, they will have to pay 10 percent additional tax on top of all the taxes they had deductions on.

“There are 10,000 new retirees every day in the United States and that number is expected to rise, so there are increasing concerns about an ageing society,” said Paul Henry, managing director of the Life Insurance Managing Research Association. “Individuals are worried, but thanks to the tax benefits offered by the government, they are able to find the right private pension for them to prepare their retirement.”

Meanwhile, support for Koreans nearing retirement and retired Koreans who work is decreasing. According to the Korea Life Insurance Association, tax benefits for retirement savings amounted to 8.8 trillion won in 2014, down from 9 trillion in 2013. This is because the tax benefits for pensions were changed from income tax reductions to tax credit reductions.

Furthermore, due to the controversy surrounding tax reductions for the wealthy, the benefit for tax-free lump-sum payments for pensions exceeding 200,000 won ended in 2013. Considering the dwindling support for private pensions, it is no surprise that in Korea, 23.4 percent of working citizens (aged 15 to 64) have voluntarily registered for private pensions, while in the United States, that figure stands at 47.1 percent.

“Korea needs to implement some policies to encourage voluntary registration for private pension funds,” said Kim Won-shik, a professor of economics at Konkuk University. “By focusing on today’s tax revenue, we may find retirees struggling in poverty tomorrow.”

BY KANG BYUNG-CHUL [ebusiness@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)