Collective home loans spur worry

Although banks have tightened screening for loans to individuals to curb debt growth, collective loans are issued to a group of home buyers who have submitted pre-orders before reconstruction begins. There is no individual scrutiny of a buyer’s credentials. Loans of that kind are rising at a fast rate, causing concerns about the future effect on the housing and financial markets.

The collective loans are guaranteed by Korea Housing & Urban Guarantee Corporation.

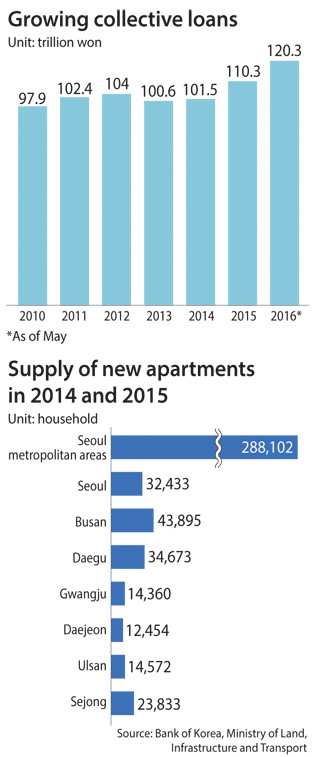

As of May, the value of such loans stood at 120.3 trillion won ($105 billion), up 10 trillion won over the previous 12 months.

The loans also jumped significantly, from 101.5 trillion won in 2014 to 110.3 trillion in 2015, largely because of the increase in supply of newly built or reconstructed apartments during that period.

According to Real Estate 114, an online real estate information provider, the number of new apartments slated for completion in 2017 is about 360,000 units, to be followed by 330,000 more in 2018. Including smaller row houses in the mix, the total figure would be above 500,000 each year.

“The recent increases in apartment supply are expected to affect market prices, as supply has exceeded demand compared to previous years,” the central bank report said.

An appropriate level of housing units to be supplied a year is between 330,000 and 390,000, according to government estimates.

“One million units of new houses is quite large even if we consider that the growth in housing supply had remained flat since 2008 in the wake of the global financial crisis,” said Shim Kyo-eon, a real estate professor at Konkuk University. “The housing market might have ‘indigestion’ as move-ins are concentrated next year.”

The “indigestion” means bumps in the money flows that should take place as people move from an old house to a new one. When moving into a new residence, a homeowner or tenant first makes a down payment, usually 10 percent of the housing price, when signing a purchase or lease contract. The buyer pays the rest of the agreed price when actually moving into the unit and, if all goes well, receives money from the sale or lease money refund from the old residence.

Those transfers of money can be a shock to the financial system, because many of them involve mortgages or general loans issued by both banks and non-bank institutions and the market may not be in balance.

“When the new housing supply spikes, some homeowners might have difficulty finding tenants, so they might reluctantly cut prices to fill up the houses, leading to an overall fall in housing prices,” said Lee Nam-soo, head of real estate at Shinhan Investment Corporation.

The 10 trillion won increase in collective loans is fueling concerns about the country’s household debt issue in an oversupplied housing market.

Park Won-kap, a senior researcher of real estate at KB Kookmin Bank, said that home buyers may find that the market price of their new house has dropped since they first bid on it and agreed to a collective loan. Nevertheless, they are stuck with the agreed original price.

Collective loans issued by non-bank institutions may cause more problems in outlying areas than in Seoul and its environs.

The BOK report said the Busan and Daegu areas have housing supplies surpassing demand in the five metropolitan cities. The average home price hit 10.28 million won per 3.3 square meters, the highest since 2007.

BY SONG SU-HYUN [song.suhyun@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)