Household debt continues climb

According to a report released by the Korea Institute of Finance on Tuesday, 23 out of a total 72 savings banks have seen household debt, including that from unsecured loans, rise more than 50 percent so far this year compared to last year. Nine savings banks have seen their debt rise between 30 and 50 percent.

Although overdue payments on loans borrowed from savings banks have decreased, the rise in debt could lead to a much more worrisome financial crisis, especially if the central bank begins raising its key interest rate.

The overall growth of household loans has accelerated rapidly as of late. During the first half of this year, loans taken out by households from savings banks increased 22 percent from last year. That’s sharper than the 16.7 percent increase during the first half of 2015 and even the 18.6 percent increase at the end of last year.

Household loans now account for 19.9 percent of all loans borrowed from savings banks, up from 17.8 percent last year.

As borrowing from savings banks grows, the performance of these institutions, whose loans charge an average interest rate of 20 percent, has gone up as well.

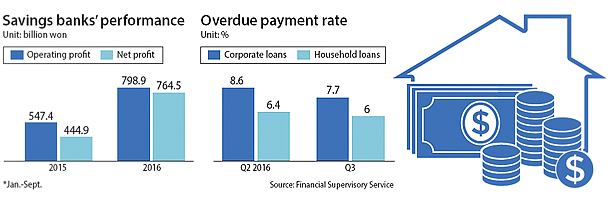

According to the Financial Supervisory Service on Tuesday, savings banks’ net profit as of the third quarter has already exceeded that of all profit made last year. Net profit from the beginning of the year to the end of September amounted to 764.5 billion won ($649 million), exceeding the 640.4 billion won net profit made in 2015 by 19 percent.

When compared to the net profit made last January to September, it is a 71.8 percent surge.

Profit isn’t the only area that has improved as the overdue payment ratio has gone down to 6.9 percent from the 9.2 percent recorded at the end of last year.

However, the improvement in overdue payment largely came from corporate borrowers, who saw their late payments drop to 7.7 percent from 11 percent last year. Household borrowers only saw their overdue payment improve marginally, from 6.8 percent to 6 percent.

“We will continue to monitor the household debt situation and guide [savings banks] to step up their loan evaluation,” a Financial Supervisory Service official said.

Lee Kyu-bok, a researcher at the Korea Institute of Finance, warned that overdue payments on the loans could increase 6 percentage points if the central bank starts raising the key interest rate. These would negatively affect families’ disposable income and lead to households tightening their purse strings.

“Korean interest rates will eventually be raised along with U.S. interest rates,” Lee said. “There is a possibility that the rate hike will not only increase the burden on loan principal returns but also lead to insolvency in both households and businesses as it could lead to contraction of the economy.”

The risks at savings banks are particularly worrying because many of those who look to savings banks for loans are those who were denied by commercial banks that offer lower interest rates.

The Korea Institute of Finance’s research estimated, based on Korea Credit Bureau data, that 70 percent of loan clients at savings banks had an average annual income of 20 million won or less.

Additionally, 46 percent of borrowers had additional loans taken out from two to three other nonbanking financial institutions. This means if the country’s key interest rate is raised, the debt insolvency could create a chain reaction that could result in a much bigger financial crisis.

Meanwhile, the loan interest rate spread at commercial banks has been rising, especially during the second half, since the government pressured the financial industry to scrutinize its loan distribution.

According to the Korea Federation of Banks, the average spread of the country’s four major commercial banks - Woori, KB Kookmin, Shinhan and KEB Hana - has risen to 1.46 percent as of October, up from 1 percent last December.

As a result, the interest on fresh loans with a variable rate at Shinhan has risen 0.26 percentage points on average compared to the end of last month. The situation wasn’t much different at other banks as KB Kookmin’s interest rate has gone up 0.16 percentage points. In other words, the spread has gone up 0.1 to 0.2 percentage points.

The higher interest prevents those with less income to apply for the lower-interest loans at the banks, which could eventually lead to more debt burden.

The financial authorities since the second half have been pressuring banks to reduce their issuance of loans as overall household debt is expected to reach an all-time record of 1,300 trillion won.

BY LEE HO-JEONG [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)