Financial institutions offering ‘hot deals’ on e-commerce sites

She was surfing through the website’s “hot deal” page when she found a free coupon that guarantees prime rates on installment savings accounts. Simply downloading the coupon would ensure higher interest rates. The next day, she opened a new account at a bank branch nearby. “It’s not easy to find a 3 percent interest rate among installment saving plans,” said Lee. “I also got Tmon points worth 5,000 won ($4.40) given to the first 10,000 downloaders.”

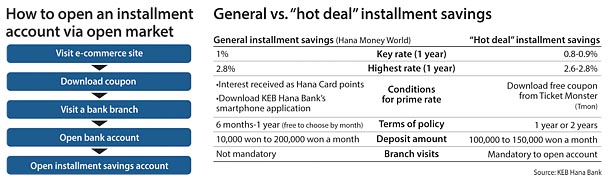

The words “hot deal” are no longer confined to physical goods or daily necessities, with banks joining the group of merchandisers on open markets. KEB Hana Bank’s “Happy Day” installment savings - the one Lee joined - was a huge success last year on Tmon, and to capitalize on this boom, the bank offered another periodic deposit plan on Tmon on Monday. The coupon, open for downloads for 28 days, guarantees prime rates of maximum 2.6 percent for one-year plans and 2.8 percent for two years. Interest rates are slightly lower than last year’s 3 percent, but still, 3,800 coupons were downloaded by 6 p.m. on the day of release.

E-commerce sites are rising as a sales channel for installment savings because they grant easier access to prime rates. High interest rates usually entail additional conditions such as downloading the bank’s app or having a certain amount in deposits. What’s different about the e-commerce coupons is that the downloader is obliged to visit the bank to open an account, the opposite of the recent trend among financial institutions looking to reduce face-to-face interaction and expand online channels. But from the bank’s perspective, this is the key advantage of e-commerce coupons: They lure in new clients to open accounts.

Among the 85,000 people who downloaded KEB Hana Bank’s coupon on Tmon, 48,000 visited brick-and-mortar branches to open a savings account. “Around 30,000 people or 60 percent of those who joined installment savings last year opened accounts at our bank for the first time,” said Bae Doe-jin, a manager at KEB Hana Bank.

Mobile carriers are proving to be effective sales channels as well. In March, Shinhan Bank released a Shinhan T Installment Savings for SK Telecom users. Subscribers are granted additional data and a higher interest rate if registering a Shinhan Bank account for automatic transfers when paying monthly phone bills. Subscribers are steadily rising.

Banks are increasingly providing promotions hand-in-hand with such non-financial sales channels to attract the younger generation. Despite the low interest rates on saving accounts, people in their 20s and 30s save regularly, even if in small amounts. “Consumers who frequent open markets tend to be price-conscious and economic. They precisely compare interest rates and share information on online communities,” said Bae. “Our plan is to extend collaboration with other fields closely related to daily life such as shopping and cars.”

For consumers, it’s important to accurately calculate how much interest they’ll receive. Installment savings sold on e-commerce so far ensure the highest interest rate if the account holder deposits 100,000 to 150,000 won a month. This means the amount of interest for consumers will not exceed 20,000 won a year.

BY SHIM SAE-ROM [song.kyoungson@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)