Debt saw record growth in Q4

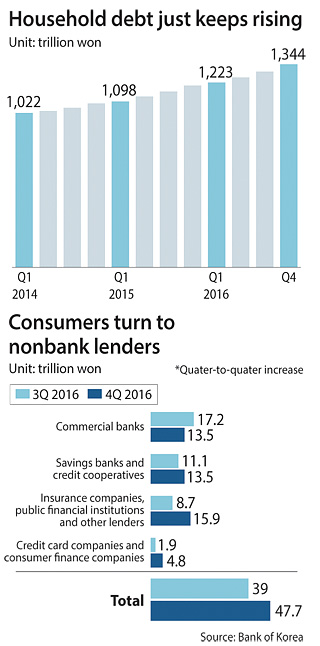

Outstanding household debt, which includes loans from banks and other financial institutions as well as credit card spending, stood at 1,344 trillion won ($1,173 billion) as of December, a rise of 3.7 percent from the previous quarter, the Bank of Korea said Tuesday.

This represents the biggest quarterly increase since the bank began keeping data in its current form in 2002.

The central bank noted that the rise was fueled by an expansion of loans from noncommercial bank lenders such as insurance companies, credit cooperatives and savings banks, which are collectively known as “second-tier lenders” in Korea.

“Banks applied tighter risk management and lending criteria as the government pushed stricter lending guidelines,” said Lee Sang-yong, head of monetary and financial statistics at the Bank of Korea. “The second-tier lenders have yet to embrace strict lending screening measures, so borrowers have flocked to these lenders.”

The amount of money owed to noncommercial banks such as credit cooperatives and savings banks had the largest quarterly increase, a surge of 4.9 percent to 291.3 trillion won.

Commercial banks, on the other hand, saw a more modest increase of 2.2 percent to 617.4 trillion.

Money owed to insurance companies also experienced a steep rise, a quarterly increase of 4.4 percent to 4.6 trillion won.

Starting in November, apartment buyers hoping to take out loans as a group - a common practice in Korea to increase the likelihood of securing a loan - were required to submit income data to banks, a measure enacted by the Financial Services Commission, the country’s financial regulator, to tighten lending standards.

Borrowers also have to pay both principal and interest in installments from the beginning, a rule that aims to hedge the risk of late payments.

Second-tier lenders were exempt from these guidelines, but they will soon have to follow them next month, the Financial Services Commission said Tuesday.

The debt from these lenders poses a greater risk to the Korean economy than from commercial banks because they cater to people with bad credit and charge higher interest rates. “Loans by second-tier lenders are more vulnerable to outside factors such as interest rate increases,” said Jeong Eun-bo, vice chairman of the Financial Services Commission.

Jeong said the government will work to keep the growth of household debt under 10 percent this year.

Private think tanks are optimistic that it can happen. Hyundai Research Institute estimates the debt level will rise 9.8 percent to 1,460 trillion won by the end of 2017.

As part of its efforts to tighten lending criteria at second-tier lenders, the Financial Services Commission will introduce a standard known as the debt service ratio, which measures potential borrowers’ creditworthiness by evaluating their debt obligations along with income.

The Financial Services Commission hopes to produce a first draft of the debt service ratio guideline by June.

The Financial Supervisory Service, another financial regulator, said it would conduct special inspections on 70 second-tier lenders during the first half of this year.

“We will investigate lenders whose credit saw a sharp rise with the Korea Federation of Savings Banks,” said Im Chul-soon, chief of the mutual savings bank examination department at the Financial Supervisory Service. “The Financial Supervisory Service will investigate 18 lenders, and the federation will look into 52 companies.”

In its report, Hyundai Research Institute said the government must clearly present policies to manage the country’s heated real estate market. The think tank noted there was a close connection between the increase in people buying apartments and rising household debt, as 60 percent of debt came from mortgages.

BY PARK EUN-JEE, CHOI HYUNG-JO [park.eunjee@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)