Most workers, despite pensions, aren’t ready for retirement

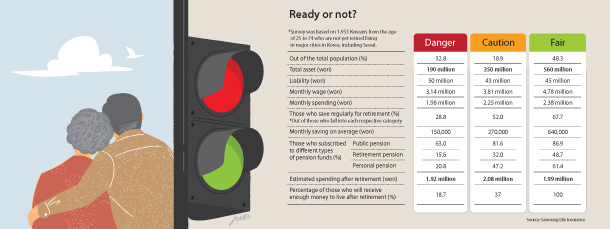

According to a survey conducted every two years by Samsung Life Insurance’s Retirement Research Center, more than 50 percent of Koreans living in major cities are not prepared for retirement. The private research center surveyed 1,953 Koreans aged 25 to 74 who haven’t retired yet and broke the results down into three categories.

Koreans in the bottom two categories, “danger,” with 32.8 of respondents, and “caution,” with 18.9 percent, are not ready for life after their careers end.

Compared to two years ago, Koreans’ retirement preparation appears to have improved. The average score for financial preparedness was 67.8 this time around, nearly 7 points up from the previous survey.

But after breaking down Koreans’ financial assets, the improved score may not provide an accurate picture of the current situation.

While the overall financial conditions improved for Koreans, most relied on real estate prices to assess their financial situation, rather than their available funds. The role of real estate in Korean households’ total assets is substantial.

According to Statistics Korea’s 2017 survey of household finances and living conditions, real estate makes up about 70 percent of the average asserts of Korean households.

Data by Korea Appraisal Board, a government-run real estate information provider, housing prices in Korea rose by 1.48 percent in 2017 compared to a year before. In Seoul, it rose by 3.64 percent, which indicates that the assets of individuals surveyed by Samsung’s research center are likely to be affected by this change.

“Monthly savings and pension subscription rates were about the same as two years ago, so the financial condition of surveyed individuals seemed to have improved because of the increase in real estate value,” said Yoon Sung-eun, a researcher at the institute. “It’s difficult to see this change as an improvement in retirement preparedness.”

The survey also showed that among those in the “danger” category, only 28.8 percent were saving for their retirement. On average, they saved about 150,000 won ($140) per month for retirement, only about one-fourth of those in the “fair” bracket.

Of the individuals in “danger,” 63 percent are subscribed to the public National Pension Service, which is required if they are employed by a company. But the subscription rate for retirement pensions (15.6 percent) and private pensions (20.8 percent) for those in “danger” is low.

About 87 percent of those in the “fair” category subscribe to the public pension, 49 percent have a retirement pension and 61 percent contribute to a private pension.

“The income substitution rate from the National Pension Service is only 24 percent, which means people must fill up the remainder with their retirement or private pension funds,” said Ryu Keon-sik, a senior researcher from the National Insurance Research Institute.

Only 18.7 percent of those in “danger” were able to cover their monthly spending with their savings and pension after retiring.

“To be able to prepare well for life after retirement, people have to work longer now,” said Kim Kyung-rok, director of the Mirae Asset Retirement Institute. “If they have subscribed to a pension, they must not withdraw from it. Those in their 60s already should consider securing some liquid cash through a reverse mortgage.”

BY HA HYUN-OCK, LEE SAENURI [choi.hyungjo@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)