Who needs cash anymore?

“I don’t like having cash on me, especially coins because they are heavy,” Song said. “It’s also impossible to analyze my spending pattern using cash. With cards, it’s much easier to track my spending with all the related apps and services available now.”

Many Koreans, particularly among the young, feel the same way.

Cash was still the dominant payment method in Korea in 2017 with an individual carrying 80,000 won ($74.03) in cash on average, according to a survey done by the Bank of Korea that analyzed the uses of different types of payment means in the country last year. However, a growing number of Koreans, especially in the younger generation, are relying more on cards as the main means of payment for shopping.

The survey, published earlier this year, showed that approximately 58 percent of people surveyed picked credit cards as the most-preferred means of payment, whereas 18.0 percent of them chose debit cards and about 23 percent still stuck to cash.

“By age group, those older than 60 favored cash while those in their 30s to 50s preferred credit cards,” explained the central bank’s report. For Koreans in their 20s, the frequency of use of debit cards and cash were nearly equivalent — about 10 times per month on average. However, about 46 percent of them said they would rather use debit cards over cash, the report showed.

By location, cash was the dominant means of payment at traditional markets, where shop owners tend to be older and may only accept cash. Koreans also chose to pay for stuff with cash at local supermarkets or convenience stores.

But when it came to other venues, such as restaurants and department stores, credit cards were by far the most frequently used method of payment.

Other than being convenient, one of the main reasons why an increasing number of younger Koreans turn to debit and credit cards was because of the rise in online shopping, thanks to the rise of mobile phone-based shopping and payment platforms.

According to data by Statistics Korea, the amount of money spent on mobile shopping catapulted from 6.6 trillion won in 2013 to 47.8 trillion won last year, over 700 percent jump in just five years. Over 65 percent of shoppers who bought goods through mobile apps used credit cards and about 27 percent used debit cards.

Those who use mobile cards — which refers to cards stored on digital wallet services such as Samsung Pay and require much simpler verification process such as a four-digit password or fingerprint — were also on a steady rise.

In 2015, about 19 percent of mobile platform shopping was done with mobile cards. This figure rose to 25 percent in 2016 and again to 34.2 percent in 2017.

“New payment services are expected to spread, especially among the young population,” explained an official from the central bank.

A new way to assess creditworthiness

When Kakao Bank first introduced its business model, one of the most notable aspects, other than the absence of brick-and-mortar locations, was its credit-rating system. The bank said it would analyze a wide spectrum of data, including online shopping histories, to evaluate a person’s credit score.

Such a credit-valuation model, which some experts dub the “sophistication of credit analysis,” is one of the big changes from the digitalization of the financial industry.

“Companies that are leaders in financial technology are already providing high-value services by securing and utilizing various technologies of the fourth industrial revolution,” said Kim Gwang-suk, a senior researcher of Samjong KPMG’s economic research institute in a report. “With credit analysis meeting artificial intelligence and big data analysis … an advanced credit rating model that analyzes more than 1,000 different pieces of information is being applied.”

According to the report by Samjong KPMG, banks in the past relied on some 20 different pieces of data such as a person’s credit default history in order to give a credit score. That model used limited information and made it difficult for people whose credit score fell in the past to borrow from major banks, which offer much lower rates than institutions such as savings bank, which in Korea are essentially consumer finance companies.

“Such a model would expand opportunities for customers with low credit ratings or incomes for wider access to financial services,” explained the report.

The Financial Services Commission, the country’s financial regulator, recognized the importance of data in the financial sector and released a policy roadmap in March to enable financial institutions to utilize more data.

“The limitation on data usage makes it difficult for credit scoring to advance,” said an official at the regulator, explaining that financial companies stay away from using non-financial information such as utility payment records of clients.

The regulator pointed out in a press release that the type of information shared by the Korea Credit Information Services is mostly negative, such as a delay in tax payments. A wider spectrum of information, such as the entire history of tax payments, may show that a customer is mostly regular in his or her payments.

“Consumers with middling credit score from four to six [with one being the best] often had to turn to lenders that charged much higher interest rates,” said an industry insider. “The adoption of big data in the credit rating system would minimize such cases.”

Recognition in the wink of an eye

Rapid advances in technology have streamlined financial transactions for consumers, significantly reducing time and effort necessary to verify one’s identity.

When Samsung Electronics introduced the Galaxy S8 smartphone in April 2017, it came with an iris-scanning system. (The feature was first introduced in the explosion-prone Galaxy Note7 a few months earlier, which was discontinued in short dispatch.) The system allowed users to unlock their phones with a scan of their eye. But the ease of unlocking the phone was the tip of the iceberg in terms of the benefits offered by the technology.

Samsung released Samsung Pass, a programming interface that enables other companies to adopt the iris scanning system into their own services.

Soon after the release of Samsung Pass, local financial institutions such as KB Kookmin Bank used the security system in their mobile banking apps. Now, anyone who owns a Samsung Galaxy S8 or later model can log into their banking apps by just looking at their phones. They can even wire money from their accounts to other people in the same manner. Before iris scanning was possible, KB Kookmin Bank customers had to enter numbers from a security card issued by the bank, a physical card which the user had to keep nearby to make mobile banking possible.

According to Acuity Market Intelligence, a technology strategy and research consultancy, the size of the global biometrics market will grow to $50 billion by 2022, which would be annual growth of 40.93 percent from 2016 to 2022.

The emergence of such technologies has played a significant role in the government’s decision to scrap the public certification system, which was implemented nearly two decades ago and is notorious for its cumbersomeness. The system forces users to install an authentication certificate on their computers or phones, issued by a handful of selected financial institutions, when they try to access banking services without visiting a bricks-and-mortar branch. It only works on Window-based computers, a headache for anyone who uses Apple computers.

The Ministry of Science and ICT proposed an amendment to the Digital Signature Act and expects the mandatory use of the public certification system will be lifted by the end of this year.

“If the law is revised, it would stimulate competition in the industry, which will give more diversified and convenient options to choose from,” said an official from the Science Ministry.

The hottest trend in lending has nothing to do with banks. Peer-to-peer (P2P) lending directly connects lenders and borrowers through online platforms, and it’s an increasingly popular option for both parties.

“P2P finance is a fintech service that automates the entire borrowing process online and minimizes unnecessary expenses, such as branch-operation fees and labor costs, to provide lower interest rates to borrowers and higher returns to investors,” according to the Korea P2P Finance Association.

Lee Jong-ah, a senior researcher at KB Financial Group’s research center, described P2P lending as “a business structure that connects borrowers and investors without having to go through traditional forms of financial institutions." He added that the model has been spreading rapidly across the globe.

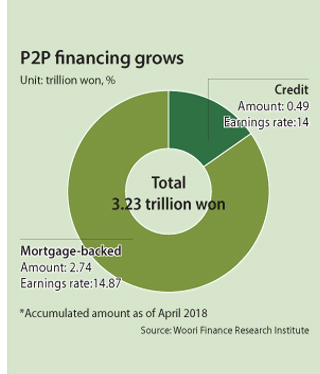

P2P lending was first introduced in 2006, but it started gaining traction in 2016. In that year, the total amount of loans issued through P2P platforms stood at 628.9 billion won ($583.43 million), according to data provided by Crowd Institute, a P2P research center in Korea. This amount more than tripled during the next year, and by the end of 2017 the accumulated amount of loans through P2P platforms was 2.34 trillion won.

As of the end of April this year, the accumulated amount was 3.23 trillion won, with collateral-backed loans at 2.74 trillion and credit-backed loans at 495.4 billion won. Crowd Institute projects that the total value of loans issued through P2P platforms in Korea will reach 4.5 trillion won by the end of this year.

According to a report by the institute, collateral-backed loans, which includes loans that use real estate as collateral, are especially popular, because they are seen as “less risky” compared to unsecured loans or credit-backed loans.

Project financing is also a popular use for P2P loans. In April this year, 108.2 billion won in P2P loans were issued to support projects such as building construction. P2P loans are an increasingly popular investment option for Koreans as they can provide as much as 15 percent interest on investments.

Korea’s financial watchdog capped individual P2P investment at 10 million won earlier this year.

Blockchain, the distributed ledger system behind the cryptocurrency boom, might just reinvent the financial system as we know it.

“Using blockchain in finance can slash data management costs, which would lead to an increase in profit and more opportunities for institutions to bring down service fees for their clients,” said Lee Dae-ki, a senior researcher at the Korea Institute of Finance. “Consumer can enjoy various perks in addition to lower fees, such as more convenient service and increased transaction speeds.”

Blockchain technology allows information to be saved in publicly distributed ledgers rather than on a centralized system. Information stored in a blockchain ledger is nearly impossible to hack, as all the data is stored in on the computers of the involved parties.

In the world of finance, blockchain allows parties involved in a transaction to eliminate intermediaries.

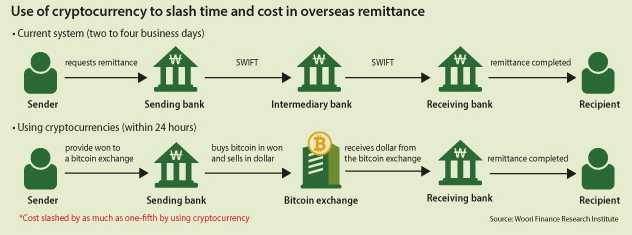

In the past, if someone wanted to wire money to another country, the sender had to use an intermediary, such as a financial messaging service provider.

The sender has to pay foreign exchange fees in order to change their currency into the recipient’s currency. By using blockchain technology and cryptocurrencies to send money internationally, the time and expense required drops dramatically, according to a report by the Woori Finance Research Institute, a research arm of Woori Bank.

Instead of exchanging currency, the sender buys cryptocurrency, such as bitcoin, and wires it to the recipient through a cryptocurrency exchange.

The purchased bitcoin will be transferred to the exchange that the recipient trades with. The bitcoin can then be converted into the recipient’s currency, and the money will be transferred to the recipient’s local bank account.

Experts say that the minute amount of fees required to conduct financial transactions using cryptocurrencies allowed people to send as little as few cents to each other.

“With fiat currency and the current money transfer system, it is impossible to outsource small tasks that require a company to pay as little as few cents overseas due to high transaction costs,” said Simon Yu, CEO of StormX, a blockchain-based freelance solutions provider. “But with blockchain technology and cryptocurrency, it’s possible to bypass that system and bring the cost down.”

According to a study by Coinone, a Korean cryptocurrency exchange, overseas remittance fees could be slashed by as much as one-fifth by using cryptocurrencies. Blockchain technology would also bring down the time required for remittances to process from two to three business days to less than 24 hours.

“Since blockchain technology does not require a substantial amount of information technology costs and significant infrastructure, it can cut costs by as much as $20 billion by 2022,” wrote Lee Jae-young, a researcher at the Science and Technology Policy Institute, in a report.

An employee at KEB Hana Bank demonstrates an asset management service run by the bank's robo advisor, which analyzes a person's investment appetite and creates a portfolio in accordance with the results. [YONHAP]

With finance industry heading towards digitalization, asset management service is also following the trend with the rise of so-called robo advisers, an automated investment advisory service that utilizes latest technologies such as artificial intelligence and data analysis.

In 2016, the Financial Services Commission, Korea’s financial regulatory agency, approved the use of so-called robo advisers, paving the way for the commercialization of automated investment services. A year later, in May 2017, Koscom, a state-run financial IT solution company, evaluated 43 robo-adviser algorithms through its Robo Advisor Test Bed Center. A total of 28 robo-adviser algorithms, including NH Nonghyup Bank’s automated asset management service NH Robo-Pro, passed Koscom’s test, which gave them permission to manage client assets.

According to a spokesperson from the bank, NH Robo-Pro is the first robo adviser to manage client pension funds.

“Through the first and second round of test bed [evaluation], 57 robo-adviser algorithms developed by 41 companies proved their system security as well as [the ability to provide strategies] optimized to the [needs] of investors,” said Kwon Heung-jin, a researcher from the Korea Institute of Finance.

According to experts, robo advisers will enable general investors to gain access to asset management services at lower fees. Previously, wealth management services were reserved for wealthier clients.

NH Nonghyup is not the only leading bank in the country throwing its hat into the robo-adviser ring.

Woori Bank has also developed Alpha, an artificially intelligent adviser that makes recommendations on client fund portfolios.

KEB Hana Bank launched its own robo adviser Hai Robo in July last year. So far, the bank has provided the service to more than 40,000 clients and it manages 500 billion won in assets.

As leading private financial institutions scramble to introduce their own robo advisers, the domestic market is expected to grow substantially in the next few years. According to a report released on May 17 by KEB Hana Bank, the market for robo advisers will grow from about 1 trillion won at the end of this year to 30 trillion won by 2025.

According to the report, robo advisers will expand their market year and become major asset managers by 2023. By then, the competition between human asset managers and robo advisers will heat up.

Korea’s banking industry, once thought to be rigid, conservative and far less open to technological change than other sectors, is becoming more digital as banks are focusing less on their brick-and-mortar branches and more on services provided through their mobile platforms.

The wake-up call came in 2017, when two new banks opened in Korea for the first time in over two decades. Unlike existing financial institutions, the two newcomers only exist online.

K bank and Kakao Bank opened in April and July to explosive popularity. Customers now expect that services like opening accounts and getting cards issued can be done with just their smartphones.

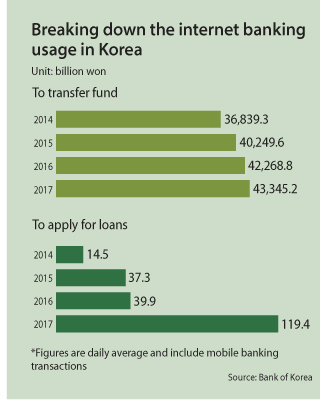

“As of the end of 2017, the total number of customers banking online stood at 135.05 million, up 10.2 percent compared to a year before,” reported the Bank of Korea. “Mobile banking clients showed a tremendous increase with the launch of internet banks.”

The data showed that mobile banking clients rose by 16 percent from 78.4 million at the end of 2016 to 90.9 million by the end of 2017. Kakao Bank has more than five million accounts as of March this year.

On these platforms, getting a loan is a lot easier and doesn’t require the cumbersome paperwork that accompanies typical bank visits. According to the Bank of Korea, the number of online loan applications rose from a daily average of 24,000 in 2016 to 99,000 in 2017.

Kakao Bank, which utilizes a treasure trove of data from Kakao, operator of the country’s most popular messaging app, to evaluate applications, issued loans worth about 5 trillion won ($4.6 billion) as of March this year.

As more Koreans do banking on their computers and phones, financial institutions other than K bank and Kakao Bank have been downsizing their physical operations.

According to the Financial Supervisory Service, the country’s financial watchdog, the total number of employees at six major commercial banks in Korea — KB Kookmin, Shinhan, Woori, KEB Hana, NH Nonghyup and the Industrial Bank of Korea — fell by 4.9 percent from 89,020 in 2016 to 84,679 in 2017. Nearly 200 brick-and-mortar branches have closed nationwide.

While the banks have been shrinking their physical operations, they have also been ramping up their digital services. “We must become the ‘first mover,’” Yoon Jong-kyoo, chairman of KB Financial Group, which owns KB Kookmin Bank, said in his New Year’s address to employees in January, “and gain a competitive edge through consumer-friendly digitalization.”

Ever since Lee Seung-keun, a 30-year-old office worker in Gimpo, Gyeonggi, switched to a Samsung Galaxy S8 last year, he rarely has to get his wallet out.

Instead, Lee uses Samsung Pay, a mobile payment and digital wallet service from Samsung Electronics.

With more services such as Samsung Pay flooding the market, Koreans like Lee are finding it much easier to make payments without needing to carry any credit cards or cash.

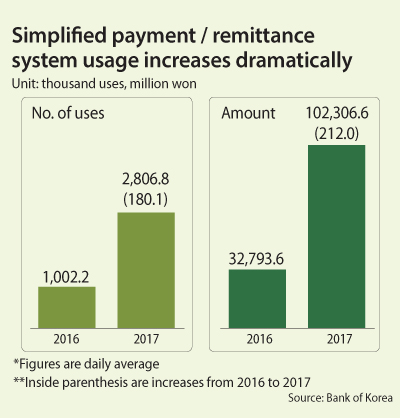

A Bank of Korea report released last month showed that in 2017 Koreans on average used digital payment services 22.59 million times per day, up 11.5 percent from a year ago, or 468.8 billion won ($434.75 million), up 36.5 percent.

The size of the domestic mobile payment market has more than doubled from 14 trillion won in 2014 to over 34 trillion won in 2016, according to Statistics Korea.

“The spread of smartphones and development of biometric authentication, as well as aggressive market participation, are creating diversified forms of [digital] payment, leading changes in the financial service sector,” said Chae Song-hwa, a member of the industry analysis team at the Institute for Information & Communications Technology Promotion.

Digital payments systems are considered a crucial element in financial technology.

Samsung Pay, for instance, uses near-field communication technology to provide a tap-on-pay solution. A user can register his or her debit or credit cards on the Samsung Pay smartphone app and pay for goods with the phone, going through a simple verification process using fingerprint or iris scanning. The total value of transactions made through the service, which was launched in August 2015, has amounted to 18 trillion won as of April this year, according to the Korean tech giant.

Some digital payment services, referred to as “easy payment” services, are embedded into mobile shopping apps and allow users to make financial transaction in less than five seconds.

For example, Coupang, an online retailer, allows its customer to link their bank accounts directly with the mobile app and enables transaction at the push of a button, eliminating processes such as typing in passwords or fingerprint verification. The e-commerce giant calls it a “OneTouch Payment” system.

BY CHOI HYUNG-JO [choi.hyungjo@joongang.co.kr ]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)