Korean brokerage firms fear 'China risk'

The China Energy Reserve and Chemicals Group Overseas Capital Company unexpectedly announced that it has failed to pay a $350 million bond that matured on May 11.

This triggered cross-defaults on other bonds.

A Korean special-purpose company (SPC) issued 165 billion won ($153.6 million) worth of asset-backed commercial papers whose underlying asset was the bonds guaranteed by the Chinese energy company.

Now with the default on the $350 million bond, the commercial paper is also expected to be worthless and Korean investors are expected to suffer.

These investors considered the commercial paper a safe investment that would generate steady profit as it was backed by the Chinese company, which many believed was backed by the Chinese government.

“The risk of the commercial papers issued by the SPC defaulting has gone up,” said Lee Hyuk-joon, general manager at NICE Investors Service. “Currently, the size of the damages that would be inflicted on [Korean] brokerage firm is hard to be determined.”

Recently there have been concerns rising in the Korean bond market of a so-called China risk.

Many investors were surprised to see the Chinese energy company default as it was backed by the Beijing Municipality.

The Beijing government seemingly stood on the sidelines while the energy company was struggling to pay the principal on the loan, let alone the interest. Furthering the confusion, the Chinese bond had received a high rating from local credit evaluation agencies even when it was strapped for cash.

“The fact that the bond of a company that is at risk has been distributed in the market posing as a bond with an exceptional rating is evidence that the credit risk systems have not properly activated,” said one industry official, who requested anonymity.

The two Korean credit rating agencies - NICE Investor Service and the Seoul Credit Rating - will likely find it difficult to avoid responsibility on the recent default.

These companies labeled the energy company as a public company because it was backed by the Beijing Municipality. Companies that are labeled as public companies receive high ratings on their credit score, as even if their cash dries up, the government usually backs them up.

However, the Korean credit rating agencies are being blamed for not properly assessing the Chinese energy company.

Even if the Chinese government does have a stake in a company, it can only truly be considered a public company if it is registered under China’s state-owned Asset Supervision and Administration Commission. The energy company was not.

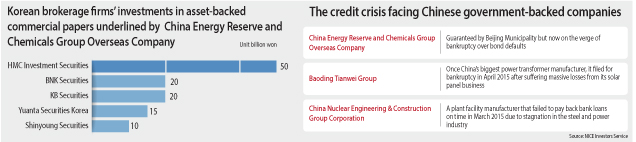

The local brokerage firms that invested on behalf of Korean investors are now on high-alert after the default. HMC Investment Securities, the brokerage arm of Hyundai Motor Group, invested the most at 50 billion won on commercial papers, followed by BNK Securities and KB Securities each investing 20 billion won; Yuanta Securities Korea with 15 billion won and Shinyoung Securities at 10 billion won.

HMC Investment Securities could face huge losses as the soaring cost of the commercial paper will be almost equivalent to the 58.9 billion won net profit the brokerage firm made last year.

As a result, there’s a conflict between the brokerage firms that invested in the commercial papers and those that were responsible for issuing them - Hanwha Investment & Securities and eBest Investment & Securities.

“This is a fraud by the companies that were in charge or failure to properly do their work if they didn’t detect any sign that something was wrong on the commercial paper that defaults just three days after it was issued,” said an official at one of the brokerage firms that faces losses on the investment.

There have been similar cases in the past where a company that were thought to be backed by the Chinese government ended up going bankrupted for defaulting on loans.

One of the most well-known cases is the Baoding Tianwei Group, which became the first Chinese state-owned company to go bankrupt after defaulting on massive loans incurred by its solar energy business.

A similar case that same year saw another state-own company China Nuclear Engineering & Construction Group Corporation faced with an overdue bank loan.

Hwang Se-woon, a senior researcher at the Korea Capital Market Institute, said the situation might get worse as the Chinese government is currently pushing to raise the efficiency of state-own companies.

“There are currently blind spots in regard to asset-backed commercial papers and the Korean government needs to closely monitor Chinese bonds that have the risk of defaulting sold under the guise of commercial papers,” Hwang said.

BY KIM DO-NYUN AND CHO HYUN-SOOK [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)