Crowdfunding regulations leave lenders at risk

Debt-based crowdfunding differs from regular investment as the capital threshold is generally lower and the screening process is less substantial than with established financial institutions. Unlike regular investment, lenders receive interest payments on the loan but do not get shares or any other form of equity.

On May 29, the producer of the mobile game Blue Marble M announced on the crowdfunding broker website Wadiz that it would postpone bond maturity repayments. Last December, the company raised 700 million won ($655,340) in investments from 770 individual investors through Wadiz. The original bond maturity date is June 15.

“Due to a lack of sales, it will be difficult to provide repayments on the date of maturity,” announced the company. “We will discuss possibly extending the bond maturity date by one year or converting it into stock at a meeting on [June] 10.”

The game company had issued a six-month bond with advertised revenue of ten percent or more annually. If the game was a hit, investors were told they could earn up to 200 percent on their investment per year.

“The company guarantees principal protection and a 10 percent revenue per year for the 6-month maturity bond,” said the gaming company in a post on Wadiz during the investment drive last year.

Despite the company’s claims, there is no guaranteed principal protection on the investment and there is no legal basis for investors to dispute their return if it doesn’t live up to the claims on Wadiz.

“As a broker, Wadiz has no authority to delete posts from investors and issuing companies,” Wadiz said via their customer service center.

As companies default on repayments, investors are finding that they have little legal protection.

“I invested because I had faith in the principal protection aspect, but now neither the issuing company nor Wadiz is assuming responsibility,” said an investor who lent 1 million won to the game producer.

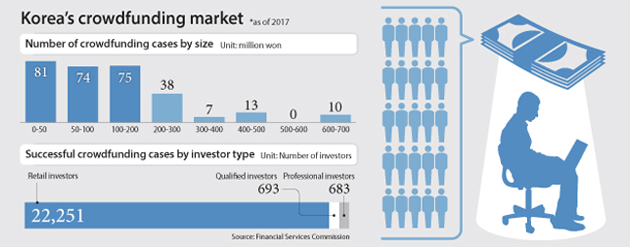

Financial authorities support crowdfunding, particularly equity bonds, as it is helpful for start-ups and job creation. A total of 299 companies have raised 50.8 billion won through crowdfunding since crowdfunded bonds were introduced on Jan. 25, 2016. Since last April, the annual investment limit of ordinary investors has been raised to 5 million won in one company and 10 million won in total.

The problem is that as crowdfunding policy focuses on attracting investment for start-ups, it lacks the means to protect investors. Although additional measures to improve the system and protect investors were announced on May 5, they may not be enough.

The policy requires a test to determine whether projects are appropriate and have potential, while limiting investment on projects that do not qualify and introducing a required minimum subscription period of 10 days.

“In the case of technological finance industry projects such as crowdfunding, over-regulating for the sake of investor protection can make things unproductive, while under-regulating can lead to losses,” said Kang Young-soo, head of the asset management department at the Financial Services Commission. “There are no principal protection guarantees in crowdfunding.”

BY KO RAN [ebusiness@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)