FSC reins in P2P firms

In Korea, P2P firms, which directly connect borrowers with investors through online platforms, are not under the direct supervision or management of financial authorities. The Financial Services Commission (FSC) only indirectly supervises them by requiring registration of P2P firms’ lending subsidiaries, which most P2P firms use to carry out the process of lending money to borrowers.

But this safeguard also has many loopholes. TheHighOneFunding, for example, had uploaded the name of a different person as CEO when it registered its lending subsidiary with government regulators.

Given the lack of regulations surrounding P2P lending, the FSC has been trying to make amends. On Thursday, it vowed to introduce legal changes to directly supervise P2P firms. On the same day, Kim Yong-beom, vice chairman of the FSC, hosted a meeting to review the current state of P2P lending with authorities from the National Police Agency, Ministry of Justice and Financial Supervisory Service.

“Because there are no barriers to entry in the P2P lending industry, it’s becoming difficult to differentiate between firms that are technically skilled and safe, and those that aren’t,” Kim said during the meeting. “We will revise rules concerning secured loans to have them reflect the real price of real estate and legislate new changes.”

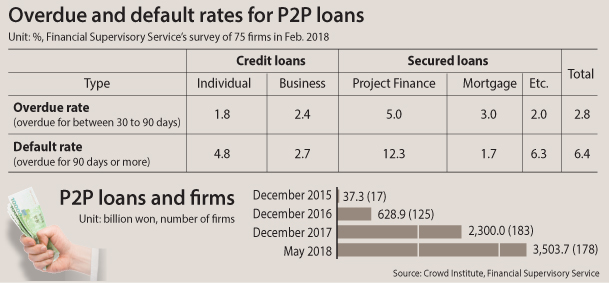

With more investors attracted to the idea of making easy money through high interest rates on P2P lending, the cumulative amount of loans on such platforms has dramatically increased, from 37.3 billion won in late 2015 to 3.50 trillion won as of May.

The platforms, though novel, do come with risks. Hera Funding, a P2P lending firm, declared bankruptcy on May 24 when it couldn’t return 13 billion won to its investors.

“I invested hoping to grow my marriage savings,” said a 33-year-old man surnamed Park who had invested 2 million won through the firm. “But I didn’t even get back my capital, let alone earn any profit.”

Because there is no principal in P2P loans, investors can’t be sure they’ll get their money back. And because there is no principal, the interest rates - and risk - are higher. An investment that promises a 20 percent return means investors are effectively counting on borrowers to pay 23 percent interest to get their money back.

To protect investors, the FSC is seeking to revise P2P lending guidelines. New provisions include preventing loans from being made if the period of investment and period of borrowing do not coincide. This measure is aimed to prevent firms from endlessly circulating investment money for profit by paying old investors with capital from new investors.

Other new measures include requesting borrowers to show documents proving a property’s value for secured loans or confirm the value of assets through a certified real estate appraiser or lawyer.

The FSC also plans to require P2P lending firms to deposit the capital and interest payments they receive from borrowers into third-party bank accounts. This move could help investors get their money back even if P2P firms themselves go bankrupt. Current regulations only require the firms keep investor capital in separate bank accounts.

If a loan is overdue, P2P firms will also have to inform investors of the leftover payment due and the late fees collected at least once a month. If a firm closes down or its executives flee abroad, the FSC will also partner with investigative authorities to bar them from fleeing the country and try to return investment money to individual lenders.

The FSC plans to complete a comprehensive survey on P2P lending firms by September and conduct on-site inspections of firms deemed suspicious.

“The P2P industry is officially beginning to filter out the fakes,” said Yang Tae-young, chairman of Korea P2P Finance Association. “Investors can reduce risk by investing across different firms that have been verified, and they should not be swayed by promises of high returns.”

BY HWANG EUI-YOUNG [kim.eunjin1@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)