Insurers target the chronically ill

His new plan is just for diabetics, however, and also provides incentives for subscribers to take care of their health and stay fit.

But new insurance plans for diabetics have average monthly premiums of just 70,000 won ($65.17). “If you walk and exercise a lot, or if you keep your blood sugar level and blood pressure in check, you can earn points that you can use to buy healthy food and supplements,” Lee said.

Insurance plans for individuals with cancer, diabetes or other chronic illnesses that provide monetary incentives for efforts taken to improve health, such as exercise, are known as health improvement insurance, and they’re facing growing consumer demand.

According to the Financial Services Commission and the Financial Supervisory Service, four insurance companies have introduced health improvement insurance plans since April.

The companies sold 60,371 of these plans between April and May.

“Until recently, insurance products have only played a passive role in providing insurance money for incidents such as disease and death,” said Ha Joo-sik, head of the Insurance Management Department of the Financial Services Commission. “But with health improvement insurance, the insurance plans are evolving to allow consumers to prevent those incidents from occurring by taking care of their own health.”

Most plans keep track of subscribers’ physical conditions by measuring their exercise habits, such as walking and running, or by checking their dietary habits, blood sugar and physical fitness. This is usually done via smartphone apps, but smartwatches and wearable digital devices can also be synced to measure health indicators.

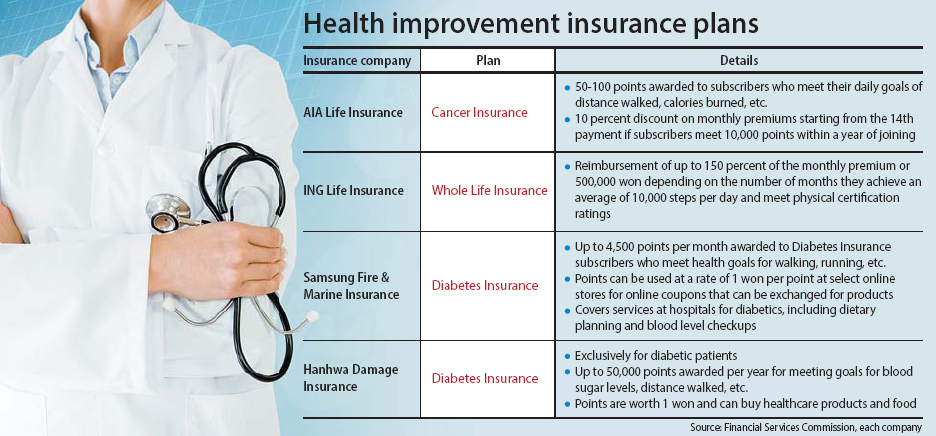

AIA Life Insurance introduced a plan for cancer patients that gives discounts on insurance premiums for walking and tracking their exercise. It measures the number of steps taken each day through AIA’s Vitality app. Consumers are awarded 50 to 100 points for meeting their daily walking, calorie-burning or other exercise-related goals, at 50 points per 7,500 steps and 100 points per 12,000 steps walked each day. If a consumer reaches 10,000 points within one year of signing up, they receive a 10 percent discount on their monthly premium starting with their fourteenth payment. “Thanks to these health care incentives, customers are less likely to suffer from disease, and insurance companies are paying less for health care coverage,” a company official said. “It’s a win-win situation.”

Meanwhile, ING Life Insurance is offering a monthly insurance premium reimbursement of up to 500,000 won for its Critical Illness Insurance lifetime subscribers, depending on the number of months they averaged 10,000 steps per day and met physical fitness requirements. Physical fitness levels are determined by combining ratings on strength, endurance, flexibility and agility.

Hanwha Insurance has also released an insurance plan exclusively for diabetic patients. When subscribers achieve their health goals, such as checking their blood sugar levels or distance walked, they receive 50,000 points a year. Subscribers are awarded 1,000 points for walking 200,000 steps in 30 days and 5,000 points for getting their blood sugar levels checked at hospitals. Points can be used to purchase health care supplies and food on an app that gives subscribers one won per point. These insurance companies developed their products based on guidelines for health improvement plans released by the Financial Services Commission last December.

“In addition to these four companies, sixteen additional insurance companies are in the process of developing health improvement plans, and some companies are planning to apply health improvement services to their existing plans,” said Oh Hong-ju, director of the Insurance Supervision Bureau at the Financial Supervisory Service.

Experts also predict that the health improvement market will grow in the future.

“Insurance products combined with health care services will continue to grow and become more popular,” said Cho Yong-woon, a researcher at the Insurance Research Institute. However, insurance companies face obstacles as they are currently prohibited from collecting health data, such as blood pressure, from consumers through wearable devices.

“As the current health improvement services of insurance companies face potentially being determined a violation of the medical law, there’s a limit to the services and plans that can be developed,” an insurance industry source said.

BY HWANG EUI-YOUNG [ebusiness@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)