Where are the online banks?

[YONHAP]

Fast-forward 10 months and Park has no money in the account and his debit card sits in a drawer collecting dust.

“It was interesting at first, but that was all,” said Park. “These days I can do essentially everything with the mobile app from the bank that I have used for years, and it just made no sense to change banks.”

It looks like Park isn’t the only person to fall out of love with internet-only banking. A year has passed since Korea’s two online banks - K bank and Kakao Bank - first threw their hats into the ring. After a year of operation, both banks are facing some major hurdles, including how to maintain their growth amid dwindling public interest, growing losses and a law that prevents investors from fully supporting operations.

Before internet-only banks were launched, the media was rife with speculation about how they would change the banking industry forever. One year in, and those substantial changes are yet to appear.

K bank was launched in April, marking the first time in over two decades that a new bank opened in Korea. Within just two months, the bank acquired nearly 400,000 clients. The number soared to around 510,000 in the third quarter.

The number of new clients began slowing down, falling to less than 100,000 this year. As of the end of June, a total of 760,000 accounts have been opened with K bank.

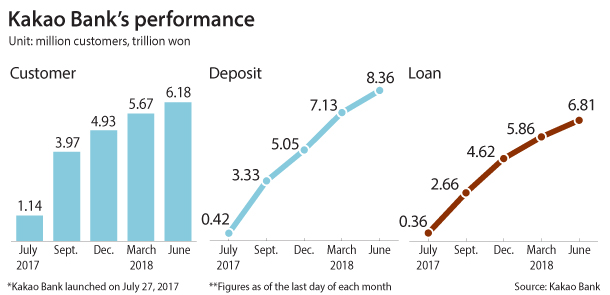

Kakao Bank, which opened in July, experienced a similar trend.

Kakao Bank got off to a far more impressive start. The service was so popular that its server crashed on its first day due to the amount of traffic. Nearly five million people signed up by the end of last year.

But its popularity also seems to be waning this year with the number of new accounts from January and June standing at around a million.

The notable fall in new customers could be seen as banks moving out of the growth phase, while some market watchers say it is a result of the lack of “innovative” and “new” services.

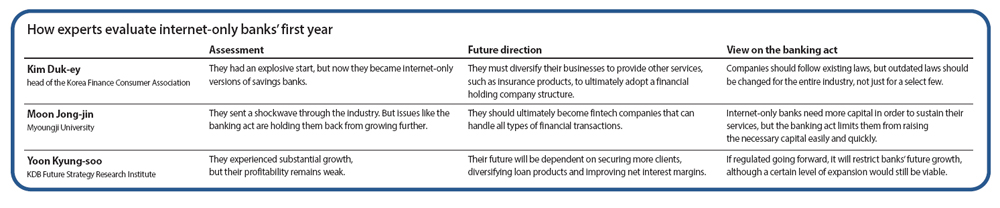

“They had an explosive start, but now it seems like … they are more convenient versions of savings banks,” said Kim Duk-ey, head of the Korea Finance Consumer Association (Kofica), a financial consumer advocacy group.

Savings banks in Korea are essentially consumer financial companies and provide loans to consumers with middling credit scores that normally range from four to six, with one being the best and 10 being the worst - the same client target group as K bank and Kakao Bank.

It is an ill-timed slowdown in growth with the numbers on their financial statement looking gloomy, according to some analysts.

After wrapping up 2017 with a net loss of 84 billion won ($74.7 million), K bank continues to be in the red, posting some 19 billion won of net losses in the first quarter of this year.

The situation isn’t much better for Kakao Bank, which concluded last year with a net loss of 104.5 billion won. The size of the loss somewhat shrunk for Kakao Bank though, recording just 5.3 billion won in losses from January to March this year.

The data also shows that Kakao Bank’s BIS capital adequacy ratio, which is the measure of a bank’s capital to its risk, has been falling from over 20 percent last year to around 11 percent this year.

A bank with higher capital ratio is considered safer.

K bank also followed a similar pattern with the ratio declining from around 17 percent in the second quarter of last year to around 13 percent in the first quarter of this year.

Analysts blamed the continuous net loss, which weighs down on its capital, for the drop.

Expanding the number of services they offer is considered a must for banks to grow and become profitable.

“Portfolio diversification by expanding the number of products, such as rental deposit loans and mortgages, will support their future growth,” said Yoon Kyung-soo, a researcher at the Future Strategy Research Institute of the Korea Development Bank (KDB). “The increase in the size of the loans issued and the rise in market interest rate will improve their net interest margin, which will have a favorable effect on their profitability.”

Kakao Bank launched its rental deposit loan service in January this year, partnering with real estate service providers such as Dabang. The total amount of loans issued through the service exceeded 330 billion won as of May this year.

“[The service] should be a new growth driver for the firm,” said Kim Jae-woo, a banking industry analyst from Samsung Securities who predicted that the service will enable Kakao Bank to break even (on a quarterly basis) by the end of this year.

But Yoon of the KDB pointed out that the bank’s recent decision to further waive fees on some of their services, such as money transfers and withdrawal, will deal a blow on their profits.

Trouble ahead

A key issue that could decide the fate of internet-only banks is the so-called Banking Act, a common enemy of K bank and Kakao Bank.

The current version of the Banking Act was intended to separate banking from commerce. As a result, it makes it impossible for non-financial companies such as KT and Kakao, conglomerates that led the consortiums that created K bank and Kakao Bank, to hold more than 10 percent of shares in a financial company.

When the consortiums were created and efforts to launch internet-only banks in Korea were being made, the government vowed that it would ease this regulation, although it has yet to live up to its words. As a result, the top shareholder of K bank is Woori Bank while that of Kakao Bank is Korea Investment Holdings, not the IT firms that led the creation of the banks.

“[The regulation] will complicate efforts to launch innovative products or to offer mortgages and corporate loans,” said Kim of Samsung Securities. “[A fragmented ownership structure is inevitable because the regulation will continue to] hinder the decision-making process.”

While there is no progress on the matter, the prospect of more internet-only banks opening is slowly fading away.

Just last year, Choi Jong-ku, chairman of the Financial Services Commission (FSC), said the government would do its best to encourage another internet-only bank to throw its hat into the industry.

Market watchers thought that major financial institutions such as KEB Hana Bank and Shinhan Bank would become contenders to lead the way along with major IT firms such as SK Telecom and LG U+. Some even predicted that KEB Hana Bank and SK Telecom would launch the next internet-only bank when they introduced Finnq, a mobile financial platform that the two companies jointly created, at the end of last year.

“At this point, there is no materialized plan on whether we would get involved in such a project,” said a spokesperson from KEB Hana Bank.

The good news for K bank and Kakao Bank is that there are some signs that the government is preparing to consider the issue again.

Last month, the government was supposed to hold a meeting presided over by President Moon Jae-in to review its regulatory reform. At the top of the agenda was the revision of the Banking Act. The meeting, which was postponed, is likely to take place later this month. The president reportedly told Lee Nak-yon, Korea’s prime minister, that he is “frustrated” about the lack of progress.

“While we need to adhere to the basic principles of the financial industries, we need to discuss how the regulation could be changed for internet-only banks to meet international standards,” said Choi of the FSC, the country’s top financial regulator, at a forum at the National Assembly on Thursday. “The social and economic conditions have matured enough now that we can accept such changes.”

“We are hopeful that things will turn for the better these days, especially because attention looks to be back from government officials on the discussion about the Banking Act,” said a manager from K bank. “It’s long overdue but we are glad to know that the government has the intention of discussing the matter.”

Some experts argue that if the law is to be changed, the government needs do so in a way that does not provide special treatment to certain groups.

“We shouldn’t change the law just to benefit a handful of companies,” said Kim of Kofica. “Firms should abide by the existing law and operate within that boundary. If the laws are outdated, then they should be changed and applied to the entire industry.”

Other industry insiders, however, say that further delaying the decision would ultimately bring down the country’s competitiveness in the global fintech market.

“Countries such as China are leaps and bounds ahead of us, and we thought easing the regulations would enable local firms to catch up in the fintech industry,” said Moon Jong-jin, professor of finance at Myongji University. “But now the government is dragging out the process, and this is causing a quite a headache for industry players because they initially expected the government’s full support.”

BY CHOI HYUNG-JO [choi.hyungjo@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)