[Debriefing] Internet-only banking woes

Left, President Moon Jae-in demonstrates a payment system using a QR code at an event promoting deregulation in the finance sector at Seoul City Hall, on Aug. 7. Right, members of the left-leaning Justice Party gather to oppose the government’s move to ease the banking regulation at the National Assembly on Aug. 20. [YONHAP]

The launch of internet-only banks in 2017 shook up the industry, forcing the traditional banks into the 21st century and pushing them to adopt more technology and diversify revenue streams.

But the country’s two online banks - K bank and Kakao Bank - are struggling to raise capital and expand their business due mainly to a banking regulation designed to curtail the influence of chaebol in the banking industry.

Discussions to change this 36-year-old law not only concern the banking industry, but revisit the country’s long-held struggle to strike a balance between promoting innovation and ensuring fair competition.

Here’s the basics on Korea’s cash-strapped online banks and the issues surrounding deregulation.

The major challenge facing Korea’s internet banks lie in their inability to flexibly raise capital from stakeholders. The problem is so big that K bank has had no choice but to suspend some of its loan services several times this year. For Kakao Bank, things are not dire yet, but the head of the bank has said that the company will find it hard to introduce new products, like mortgage loans and credit card services, because of insufficient capital flow.

Q. Why are they struggling to get enough capital from investors?

The lead investors of K bank and Kakao Bank - KT and Kakao - are unable to funnel more funding into the banks because of legal regulations that cap investment. The current banking act stipulates that non-financial companies, like mobile carrier KT and tech firm Kakao, can only hold shares worth up to 10 percent of the company and can only vote with 4 percent of them. This is why both companies only hold 10-percent stakes in their respective banks and other financial and corporate players the rest of the shares in a consortium format.

When the two banks look to raise capital through sales of additional shares after the initial investment, the stakeholders are unable to put more money in because it is illegal for them to grow their investment.

In the case of Kakao Bank, Korea Investment Holdings is the top shareholder with a 58 percent stake, though there is a tacit agreement that Kakao will take the top spot once the regulation relaxes. Since Korea Investment Holdings has a sound capital base, Kakao Bank finds it relatively easier to secure additional funding.

K bank’s stakeholder structure is more fragmented with interested parties holding comparably minor shares, a factor that has meant the bank was unable to raise sufficient capital in July. At the time, minority shareholders reportedly refused to chip in because they were not notified of the investment drive in advance.

The regulation dates back to 1982, when the Chun Doo Hwan government attempted to prevent banks from being exploited as the personal piggy banks of chaebol owner families.

Before 1980, banks were largely owned by the government. As the administration began the drive to privatize the banking industry in the early 1980s, a call for a regulation that limits banking shares held by non-financial companies grew. The proponents of the restriction said that, if allowed, chaebol could unfairly favor their affiliates in lending and other services by using deposit money.

The introduction of the law is linked with a perception engrained in the Korean financial industry to consider banks as a semi-public sector, given that a large portion of their capital is based on people’s savings. The Korean financial regulator imposes strict criteria and capital requirements on establishing a new bank, but big corporations are allowed to enter other financial businesses such as card, insurance and securities, given that the segments are more leveraged financial services.

Q. Is there a history of chaebol attempting to heavily invest in banks?

No chaebol has ever officially attempted to enter or invest in the traditional banking sector.

But back in 2007, an internal Samsung report was leaked that showed the group apparently considering different scenarios in which it could operate a bank.

The revelation quickly triggered a backlash from the public and civic group. A year later, Lee Hak-soo, a former vice chairman at Samsung Electronics announced that Samsung won’t enter banking industry.

As for the internet-only platform, SK Group participated in a bid to operate an internet-only bank but it didn’t make it through the government screening process in 2015.

Q. What is the government doing to try and change the current situation?

President Moon Jae-in and financial authorities have called for the need to increase the maximum amount of shares that a non-financial company can hold in an internet-only bank.

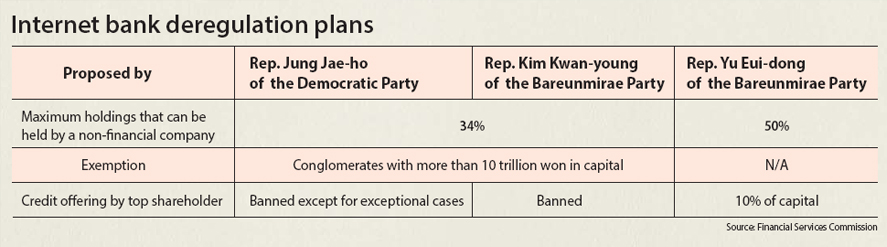

Many members of the liberal Democratic Party are skeptical about lifting the regulation, but the president’s call has prompted lawmakers to change their stance and support deregulation. The opposition parties - the Liberty Korea Party and Bareunmirae Party - have long advocated the need to relax the banking regulation, but the two sides don’t see eye-to-eye on the details

The majority of the ruling party believes the maximum 10-percent cap should be raised to 34 percent, while many in the opposition party want to push it as high as 50 percent.

Q. Is deregulation likely to be approved by the National Assembly?

The prospect for passage became more optimistic with Moon’s official endorsement last month.

Policy chiefs from the three main parties - the ruling Democratic Party, the main opposition Liberty Korea Party and the opposition Bareunmirae Party - tentatively agreed to pass a bill in August that could lift the ownership limit to somewhere between 34 and 50 percent for investors in internet-only banks. The lawmakers have so far failed to reach a consensus due to disagreement on the specific limit.

Another point of contest is whether conglomerates will be permitted to increase their stakes in internet banks. The ruling party and the Financial Services Commission say that only tech and gaming firms with less than 10 trillion won ($8.9 billion) in capital should be allowed to invest, while the opposition argues that large conglomerates should also be entitled.

Despite the dispute, analysts believe that a bill could pass as early as September.

BY PARK EUN-JEE, JIM BULLEY [park.eunjee@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)