[The Future is Now] Are wallets becoming a thing of the past?

A food stall near Pangyo Station in Gyeonggi promotes electronic and mobile payments with a card and banner that reads “we welcome card payments” on Oct. 2. [PARK SANG-MOON]

These small food stalls, known as pojangmacha in Korean, are a common sight across the country. But this being Pangyo, things are a little bit more high tech at these small outdoor restaurants.

White cards printed with QR codes are attached to the front of each tent, the only indication that these merchants are trying to keep up with the rapidly changing payment ecosystem embraced by their large high-tech neighbors.

Jun Chae-hyun, a 29-year-old woman living in Pangyo, is one of the customers that have taken this shift in their stride.

Jun used Kakao Pay to buy tteokbokki (rice cakes in a spicy sauce) at one of the food stalls on Oct. 10.

“I rarely carry cash, and I usually just have 10,000 won ($8.80) on me, just in case I have to pay valet parking fees,” she explained.

Park Young-moon, the owner of one of the food stalls, said on Oct. 2 that only about half the payments he receives are in cash, with other customers using credit or debit cards and mobile payment systems, though the average charge is just 4,000 won.

The 55-year-old man adopted the QR code-based payment system provided by Kakao Pay earlier this year to cater to young and tech savvy customers, many of whom work at nearby tech firms.

“Many people used to tell me that they have to pass [my stall] by because they didn’t have enough cash,” Park said. “Now they can just drop by without their wallet, and the mobile payment system is more convenient for me, too, because buyers process their own payments.”

Mobile payment systems were first popularized online, where e-commerce shoppers found that using smartphone-based purchasing systems was much simpler as it bypassed the cumbersome authentication and security programs that Korean banks are infamous for.

When it comes to brick-and-mortar payments, Korea got off to a relatively late start, due in part to the popularity of credit and debit cards.

Still, mobile payment systems like Samsung Pay, Kakao Pay and Payco are now a common sight throughout Korea, from fancy restaurants and coffee shops to street vendors and mom-and-pop stores.

Just a few years ago, paying with a smartphone at a restaurant or convenience store would have looked like something out of a sci-fi movie, but today, a growing number of people go shopping with nothing but their phone in their pocket.

Meanwhile, transactions involving cash have significantly decreased in the face of the popularity of credit and debit cards that can be loaded onto different mobile payment systems.

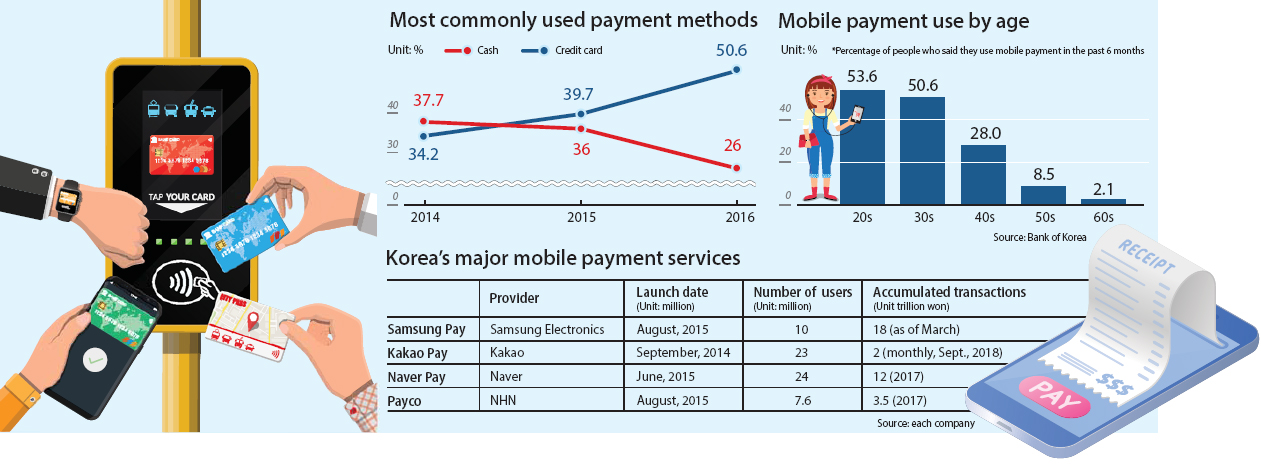

According to the Bank of Korea, the share of cash transactions - measured by the number of uses - sharply declined from 37.7 percent in 2014 to 26 percent in 2016, while credit card transactions jumped from 34.2 percent to 50.6 percent to become the most commonly-used payment method.

A survey published by the National Assembly Research Service in 2017 found that the portion of cash payments fell even further to 17 percent by the value of transactions.

The rate is lower than that of other advanced economies such as Germany (53.2 percent), the Netherlands (34.3 percent) and Canada (53.2 percent).

Users pointed to convenience as the main reason for the popularity of mobile payment systems.

The advent of applications designed to facilitate easy money transfers on mobile devices also prompted many - especially younger people - to embrace digital payments.

One of those platforms, Toss, now boasts 5 million users and has pulled in investment from deep-pocketed players including PayPal and Singapore sovereign wealth fund GIC and Sequoia China.

Tap and go

To cash in on the increasing user base, mobile payment players are vying to take a bigger slice of the market by expanding their affiliated shops and restaurants.

Samsung Pay is taking the lead with ten million users and the highest accumulated transactions totaling 18 trillion won as of March.

Launched in 2015, the digital wallet service built into the latest Samsung’s Galaxy phones was able to strengthen its footing thanks to the widespread use of the devices and the convenience and compatibility of the underlying technology.

The payment system uses near-field communication (NFC) payment technology and magnetic secure transmissions that enable the smartphones to work with the vast majority of existing card terminals.

“From the start, we put a lot of thought into making payments more convenient for our users,” said a spokesperson at Samsung Electronics.

While the spokesperson declined to reveal the exact number of shops that have signed an agreement with the payment service, he said that users can use Samsung Pay at most shops that accept card payments.

Kakao Pay, an affiliate of internet company Kakao, is seeking to carve out a niche by targeting small-sized shops run by self-employed people who might not want to take on the burden of setting up a card reader.

This is why the service incorporated within the popular messaging app Kakao Talk supports food stalls and street vendors across the country alongside well-known franchise coffee shops.

Target places include the bustling area in Insa-dong, central Seoul, a neighborhood famous for shops selling traditional artifacts, souvenirs and tea.

“We try to reach small shops that might find it difficult to set up card terminals, and we charge no fee,” said Chung Ju-hee, a public relations manager at Kakao Pay.

Kakao Pay adopted the QR code system ubiquitous in China for transferring consumers’ purchases straight to a merchants’ bank account.

The system is available at more than 100,000 retailers, and Kakao plans to open it up to Chinese tourists in partnership with Alipay next year.

Korea’s financial institutions hope to emulate the system to allow users to process purchases with linked bank accounts through their smartphones.

The central bank will spearhead the development of standardized technology and a mobile application in cooperation with 28 participating financial institutions. It aims to release the platform in the first half of next year.

Still, the infrastructure for mobile payment systems is far from flawless as it often faces technical glitches.

Lee Jung-han, who runs a stamp shop in Insa-dong, said that he encourages his clients to use cash or card because the mobile payment system often causes error.

“Mobile payments might be convenient for customers, but not so for merchants,” he said. “The reader sometimes fails to read smartphones, so I let people know in advance that this might not work.”

Toward a coinless society

All of the developments and projects add up to the idea of the coinless society envisioned by the central bank.

The Bank of Korea will first experiment with the notion to gauge the potential benefits and risks of going completely cashless.

In a roadmap announced in 2016, the bank proposed reducing the circulation of coins by 2020. To achieve the goal, it will roll out different measures to expand digital payments.

In the first phase, it will target convenience stores since they tend to hand out change in coins.

The Bank of Korea has already introduced a system where customers at convenience stores can deposit loose cash into reloadable cards like T-Money, a public transit pass, and gift cards.

Yoon Jae-ho, the senior economist at the central bank in charge of the initiative, explained that the movement is not aimed at replacing cash with digital payments as in some European countries like Sweden.

“Our goal is to diversify the range of digital payment options,” Yoon said.

In the latest stage of the coinless society movement, Yoon said that the central bank is in talks with different financial institutions to launch a service that deposits loose cash directly into users’ bank accounts next year.

Some retailers took the idea seriously and embarked on their own trials.

Starbucks Korea, for instance, is testing its cashless store concept at more than 100 locations across the country.

The project came as less people are using cash. Paying with cash has been constantly declining at Starbucks stores in Korea, from 31 percent in 2010 to 15 percent in 2013 and 7 percent last year, the company said.

But not everyone is happy with the drastic shift toward a cashless society because it can potentially exclude elderly and disadvantaged consumers.

For instance, over half of those in their 20s and 30s use mobile payment apps, but only 2.1 percent of people over 60 signed up for the service last year, according to the Bank of Korea.

Noh Yong-kwan, a researcher at the Korea Development Bank, predicted that mobile payment systems in Korea will evolve into a comprehensive retail platform.

“If you look at China’s Alipay, the platform not only offers payment service but also has a wide range of shopping items,” he said. “But to provide such services, we need one or two dominant players, but the market is fragmented.”

Noh said that when the market is consolidated, the payment service providers could incorporate retail shops selling clothes, cosmetics and financial products to scale up business.

BY PARK EUN-JEE, CHAE YUN-HWAN [park.eunjee@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)