Hopes for P2P business turn into unpaid loans

Once hailed as the “next generation of financing,” peer-to-peer finance is going the way of the dodo bird as loans are defaulted on and investors rethink the fundamental viability of the business model.Peer-to-peer finance, or P2P, connects borrowers and lenders directly online. It is small in scale and was supposed to grow into an alternate source of finance for small businesses and individuals who couldn’t borrow from banks.

Terafunding, a leader in the local P2P investment industry saw its first P2P loss, according to industry sources last Wednesday.

The losses came from three investments in construction of several houses in Goyang, Gyeonggi, and Taean County in South Chungcheong. The problematic investments were project financing of more than 10 billion won ($8.2 million). Investors who gave money to Terafunding to lend on the projects lost an average of 20 percent.

Project financing is a loan structure that relies primarily on a project’s cash flow for repayment, with a project’s assets, rights and interests held as secondary collateral.

Terafunding is one of the leading companies in Korea’s P2P finance business. Last year, it made more than 1.4 trillion won ($1.2 billion) in loans. The news of its recent loss made many investors worried about P2P funding.

In fact, other P2P businesses are seeing losses too, according to an insider in the finance industry.

8 percent, a P2P investment platform, saw a 28 percent loss in its funding of 12 musicals, according to industry sources. However, 8 Percent said that the losses would shrink after some overdue payments are collected.

Last December, the Financial Services Commission (FSC) asked prosecutors to investigate another P2P company called Pop Funding for possible fraud, according to sources in the industry. The FSC is waiting for results from the investigation, which was finished in mid-February.

Pop Funding lent money to small- and medium-sized businesses using relatively insecure assets such as production machines, cars, equipment or materials as collateral. Pop Funding was actually named by the FSC last year as a model of financial innovation - before the prosecution started investigating it.

The company is suspected of accounting fraud. Two private equity funds that invested in projects with Pop Funding were unable to pay their own investors back and had to push back the repayment date by a month.

As P2P financing became a buzzword, it attracted a lot of money.

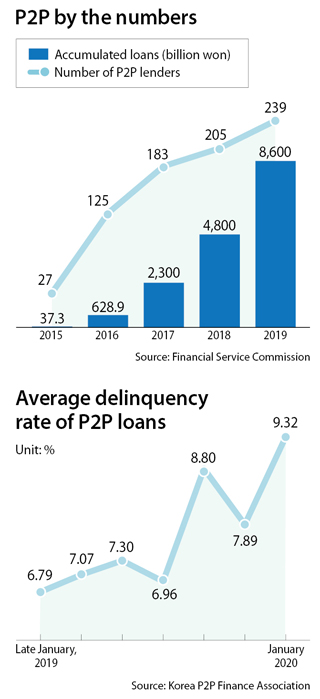

The accumulated debt generated by P2P businesses grew from 3.7 million won in 2015 to 8.6 trillion won last year. It promised high returns in a time of very low interest rates and promised all sorts of wondrous success based on the allure of tech, convenience and doing something new.

P2P businesses started making risky investments in real estate project funds, non-performing loans and mortgages. Since P2P businesses lack experience in risk assessment compared to institutional banks, P2P businesses lent recklessly.

“Simply put, [P2P businesses] lent money to projects or individuals with low credit scores, which leads to high delinquency rates and high risk of losing money,” said Kim Sang-bong an economics professor at Hansung University. “It’s better to invest in businesses that provide a wide range of investments with less focus on real-estate.”

And investors - both direct and indirect - are feeling the pinch as the delinquency rate of P2P loans continues to rise.

Currently, 45 businesses are registered as members of the Korea P2P Finance Association, and on average 9.32 percent were having trouble being repaid last January. The delinquency rate steadily rose from 7.89 percent last November to 8.43 percent last December. Some estimate loan delinquencies may run higher as there are 239 P2P businesses registered with the FSC.

Experts worry that the growing number of failures will hurt the P2P market as Korea prepares to legally formalize peer-to-peer financing.

The government passed the Act on Online Investment?Linked Financing and User Protection three years ago to clear up the legal gray areas for P2P investment. This so-called P2P Act will take effect Aug. 27.

Critics worry that problems might discourage P2P investments and put a damper on the government’s ambition to use the P2P model to cultivate a market for affordable loans.

Or P2P finance could grow steadily as in other countries, once the laws are set and early P2P disasters are forgotten. From August, companies must register with the FSC and prove at least 500 million won in capital to be in the P2P business.

They will be subject to the Loan Business Act, which limits the maximum annual interest rate at 24 percent, including fees.

“There are many companies that currently have less than 500 million won in capital. Many will run out of business [once the law takes effect] after August,” said Kwon Dae-young, head of the Financial Innovation Planning Group under the FSC.

Kwon says the government hopes the P2P market will stabilize with time. “As investors are more likely to focus on investment on P2P businesses with a good track record, the market will likely be reorganized around them,” said Kwon.

BY SUNG JI-WON [kang.jaeeun@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)