[DEBRIEFING] Of sidecars, uptick rules, circuit breakers and bans

The stock markets in Korea, like all markets around the world, have been exceptionally volatile in the age of the coronavirus.

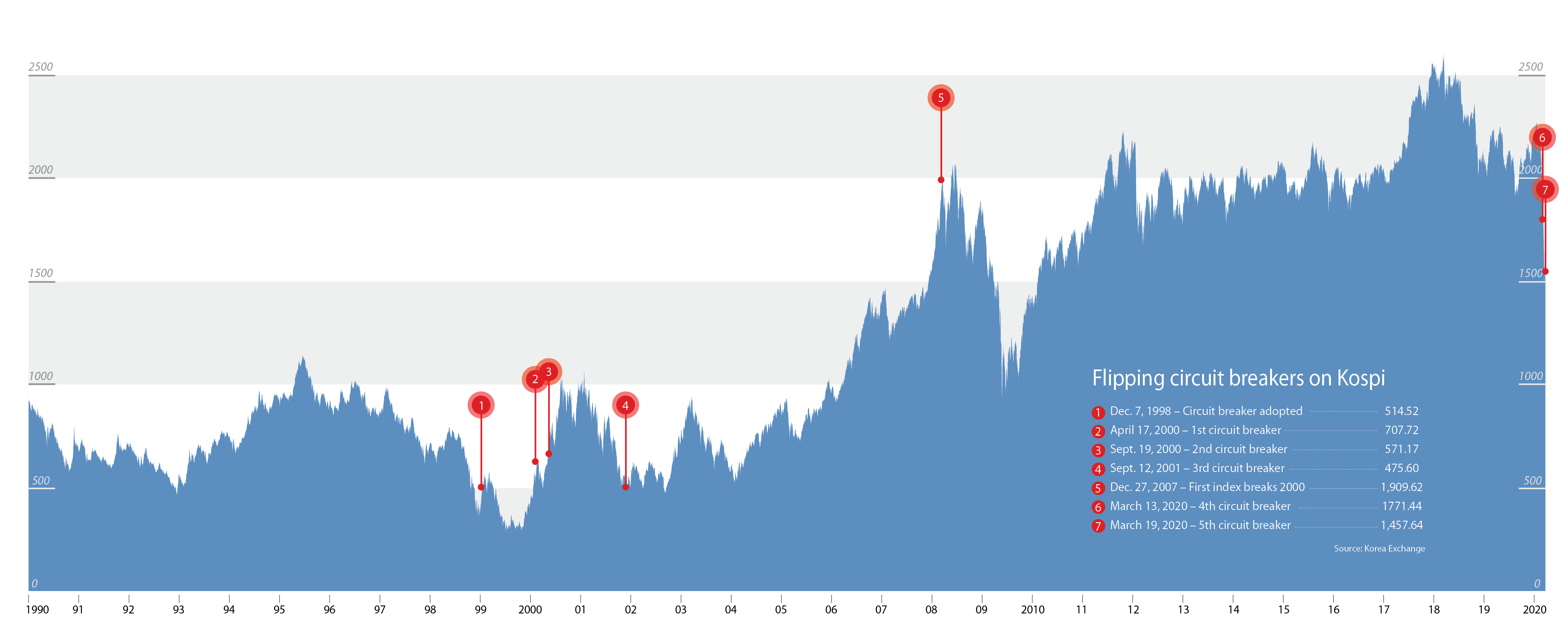

After the outbreak started and turned quickly into a pandemic, the benchmark Kospi plunged through the 2,000 level, falling to as low as 1,457.64.

Just last August, the index hit an all-time high of 2,574.76.

The first sidecar trading halt in nine years was triggered on March 12. The first circuit breaker in 20 years was flipped the next day.

A total of six sidecars have been activated this year for the Kospi, and five for the Kosdaq. Two of each were triggered for stocks rising too quickly.

But what do sidecars and circuit breakers do and what do their uses actually mean?

And what other market volatility safeguard measures are there?

A board at KB Kookmin Bank in Yeouido, western Seoul, on March 13 shows the Kospi closing at 1,771.44, 62.89 points or 3.43 percent lower than the previous trading day. The first circuit breaker of the year was triggered that day, the second on March 19. [YONHAP]

Stocks have been extremely volatile in recent weeks, and we’ve been hearing about sidecars, circuit breakers and short selling bans. What, exactly, are these?

Sidecars and circuit breakers are mechanisms adopted to ease the volatility in stock markets.

A sidecar suspends futures trading for five minutes to stop panic. It is triggered when Kospi 200 futures rise or fall more than 5 percent and hold that gain or loss for at least one minute.

For the Kosdaq, a sidecar is activated when the Kosdaq 150 futures rise or fall for more than 6 percent or when the Kosdaq 150 index fluctuates more than 3 percent.

The sidecar only activates once during a single trading day, and it is not triggered within the first five minutes of trading and the last 40 minutes

Circuit breakers are similar, but the restrictions are far broader in scope.

While a sidecar only suspends trades of futures, a circuit breaker suspends all trades: of all spot trading and related derivatives.

Three circuit breakers are possible: when an index falls 8 percent compared to the previous day’s close, 15 percent and 20 percent.

During a Level 1 or Level 2 circuit breaker, trades can be canceled but nothing else. Once the suspension is lifted, stocks are traded at a single price for 10 minutes.

A Level 3 circuit breaker is also triggered when stocks fall 1 percent after a Level 2 circuit breaker is initiated.

What is the theory behind these interventions? Do they really work?

The goal of the market interventions is to stabilize the stocks while protecting investors, keeping in mind that the sidecars can be triggered up and down while the circuit breakers are only activated in falling markets.

The sidecar is adopted specifically to counter the potential dangers of program trading.

In program trading, baskets of stocks are bought and sold by computers utilizing algorithms. When markets falls and they sell, that causes more declines, and so on. It’s a vicious circle.

In the other direction, the breakers are triggered to prevent a speculative rush.

The interventions are believed to calm investors and allow them to collect their thoughts, evaluate market information and rethink of their investment choices during the cooling-off period.

Over the years, the rules have changed. Sidecars were first activated with 3 percent moves. That was increased to 4 percent in 1998 and then 5 percent in May 2011.

The daily limit for individual stock price movements was changed in 2011 to 15 percent from 12 percent. It was further increased to 30 percent on June 15, 2015, in hopes of attracting the more aggressive participation of retail investors in the Korean stock market.

Circuit breaker regulations were tightened in 2015 with the introduction as the daily limit was raised to 30 percent.

No consensus exists as to whether they really work, and some academic studies question the effectiveness of the interventions. In particular, they note the magnet effect, whereby prices may tend to rush toward the trigger price as investors sell to get out before the halt begins.

Those opposing the intervention tools argue that they limit participation and thus affect liquidity. They also say that the complete shutdown of the market only contributes to market panic while frightening investors from entering the market.

In 1997 and 1998, they did not seem to work.

In 2008 during the global crisis, the sidecar was active every single trading day for a month between Sept. 16 and Oct. 15.

When were they first used and how do they fit in the development of the Korean capital markets?

Sidecars were first adopted on November 25, 1996, for Kospi stocks, while they were adopted at the Kosdaq on March 5, 2001.

The introduction at the Kospi followed with the introduction of the country’s first stock market index futures in May 1996. In July 1997, the sidecar mechanism came to the stock index option market.

The circuit breaker was adopted on Dec. 7, 1998, after dramatic falls during the first financial crisis.

The Kospi, which has reached a high of 792.29 on June 17, 2017, fell 53.8 percent for six months through Dec. 24, when the International Monetary Fund swooped in.

On Oct. 29, the Kospi fell below 500 for the first time in five years.

The first sidecar is believed to have been activated in 1997, though the Korea Exchange didn’t give a specific date. That year alone, 120 sidecars were activated. The following year, the total was 183.

The first circuit breaker activated on April 17, 2000, on the Kospi after the market dropped 90 points in 10 minutes due to the overnight market crash in the United States. The Dow Jones Industrial Average fell 5.56 percent, while the Nasdaq tumbled 9.67 percent.

The first circuit breaker was activated on the Kosdaq on Jan. 23, 2006, after the market fell following the overnight drop in New York City.

Until now, circuit breakers have been activated only three times, the first being on April 17, 2000.

The second was on Sept. 19, 2000, when the market crashed on the dotcom bubble burst and on news that Ford was giving up on its purchase of the now-defunct Daewoo Motor.

The most recent circuit breaker for the Kospi before the coronavirus outbreak was on Sept. 12, 2001, the day after the 9/11 terror attack.

Korea is not the only country that uses these mechanisms. What other countries call halts and ban short selling?

Korea is not the first in the world to adopt market intervention mechanisms.

The United States introduced the circuit breaker in 1988 after the Dow Jones Industrial Average crashed on Oct. 19, 1987, losing 508 points or 22.7 percent. That day become known as Black Monday.

The only other time the circuit breaker was triggered was in 1997.

But this year, the circuit breaker has been flipped four times.

Like the Korean circuit breaker, the United States also has three different levels.

The first level is when the S&P 500 drops 7 percent, while the second activates when it drops 13 percent. The third is when the market falls 20 percent.

In the first two levels, the market stops trading for 15 minutes. As in Korea, the third ends all trade for the remainder of the day.

Most of the countries in Asia, including Japan, India and Thailand, have a circuit breaker. Those in India and Thailand were triggered on March 13.

China invoked its circuit breaker on the first day of 2016.

The European market does not have a market-wide circuit breaker, but it does have circuit breakers for individual stocks.

The United States also started to apply single-stock circuit breakers - or limit up-limit down, or LULD - in April last year.

How about share buybacks? Are they used much here?

The buybacks have been utilized since the law was relaxed in 1992. At first, companies were only allowed to buy back shares indirectly through financial companies.

But in 1994, the rules changed, and companies were permitted to directly buy their own shares.

It has become a common practice today.

According to the Korea Corporate Governance Service, a total of 208 public Korean companies bought back shares 2017. That number grew to 307 companies in 2018.

A total of 154 companies bought back shares in the first eight months of 2019.

In the three years through August 2019, 676 companies committed 19 trillion won ($15.5 billion) to buybacks.

Samsung Electronics topped the list, with 9.2 trillion won of buybacks between 2017 and August 2019, followed by SK hynix, with 1.7 trillion won, and SK Innovation, with 1 trillion won.

Executives have also been buying shares in the companies they lead.

In five days since March 19, Hyundai Motor Chairman Euisun Chung bought 81.7 billion won of Hyundai Motor and Hyundai Mobis shares. It is the first buyback that Chung has made since 2015.

This has raised Chung’s stake in Hyundai Motor up 0.27 percentage points to 2.62 percent. In the case of Hyundai Mobis, Chung didn’t own a single share in the automotive parts supplier. With the recent purchase, Chung now owns 0.32 percent of the company.

The move came after both Hyundai Motor and Hyundai Mobis shares fell by half in about a month.

Hyundai Motor shares in February were traded in the 120,000 won range. On March 19, they closed at 65,900 won. Hyundai Mobis, which was trading around 230,000 won in mid-February, on March 19 closed at 129,000 won.

Since the buyback, both shares have risen. Hyundai Motor stocks closed at 84,900 won on Thursday, while Hyundai Mobis closed at 167,000 won.

Lotte Group Chairman Shin Dong-bin on March 20 bought 1 billion won of shares in Lotte Corporation, raising his stake 1.2 percentage points to 11.67 percent.

What role is the National Pension Service play in the market? Does it support stock prices?

The pension funds, especially the national pension fund, have swooped in stopping share prices from falling.

Since the first sidecar and circuit breaker were triggered on March 16 through March 26, pension funds net purchased 876 billion won worth of stocks.

During the same period, foreign investors have sold off 2.78 trillion won worth of stocks.

During the 2008 global financial crisis, pension funds aggressively purchased shares in the local markets.

The Kospi at the end of 2007 was at 1,897.13. In 2008, it fell 40.72 percent, closing the year at 1,124.47.

Between September and October of 2008 when the global crisis kicked off with the bankruptcy of Lehman Brothers, pension funds net bought 5.26 trillion won worth of shares.

Buying these funds was especially heavy in large companies, such as Samsung Electronics, in which the pension funds bought 812.2 billion won worth of stocks; Posco, at 514.3 billion won; and KT&G, at 214 billion won.

The national pension fund, which is the largest among the funds, manages more than 700 trillion won worth of shares, of which more than 40.6 percent is invested in stocks at home and abroad.

Among the investments, 132.3 trillion won is invested in Korean stocks, and 166 trillion won is invested in overseas stocks, more than half in North America.

How about the central bank? Is it getting involved?

After market volatility increased this month, the Korean central bank also engaged in market stabilization efforts. The first action it took was lowering the key interest rate, aimed at increasing liquidity in the market.

The base rate is at an all-time low of 0.75 percent, the first time it has gone below 1 percent.

The next step it took was signing a $60 billion currency swap with the United States. This was a key move, as it discourages investors from rushing for the exits due to the weakening won.

These tools were both used by the central bank in 2008. Following the bankruptcy of Lehman Brothers, it lowered the key interest rate.

Starting with 0.25 percentage points in October 2008, the Bank of Korea lowered the key interest rate six times through February 2009. The key interest rate dropped from 5.25 percent to 2 percent. This rate remained unchanged until July 2010.

The currency swap with the United States was first introduced in 2008.

In an unexpected move, the Korean central bank was able to draw on a $30 billion currency swap with the U.S. Federal Reserve, which helped ease fears of a liquidity crisis.

The currency swap helped stabilize the Korean won against the dollar.

The won was valued at 1,089 won against the dollar at the end of August in 2008.

It dropped to 1,468 won before the currency swap deal. Once the announcement was made the won appreciated to 1,250 won.

In this crisis, the Bank of Korea has taken one additional step. It promised the unlimited availability of repurchase agreements for the next three months.

The liquidity supply in the market through repurchase agreements was also practiced during the 2008 crisis, but this is the first time no limit has been set on the agreements.

Does the swap agreement also work to stabilize the markets? It seems to have had an effect.

Korea currently has swap agreements with eight countries and is a member of the Chiang Mai Initiative Multilateralisation.

The recently signed currency swap deal with the United States is the largest, while the deal with China is for 360 billion yuan, or roughly $56 billion.

There is no ceiling in the swap deal with Canada.

The first currency swap deal between Korea and the United States was on Oct. 30, 2008, barely two months into the global financial meltdown. The amount at the time was $30 billion.

In 2008, the Kospi ended the year down 41 percent, while the Kosdaq was down 53.26 percent.

The massive sell-off by foreign investors didn’t help. They net sold more than 36 trillion won worth of Korean stocks.

It was the largest net selling by foreign investors since related data has been compiled since 1998.

Foreign investors set a new record in a selling spree that went for 33 consecutive trading days between June 9 and July 23. The previous record was 24 consecutive days in 2005.

The Kospi, which broke the 2,000 mark on July 25, 2007, 27 years after country’s first stock market was opened, halved in October 2008, falling below 1,000 on Oct. 24 closing at 938.75. On Oct. 29, the market closed 30.19 points lower than the previous day, or 3 percent.

But after news of the currency swap, the Kospi surged adding 115.75 points, or 11.95 percent, raising above 1,000.

The Korean won, which was at 1,427 won against the dollar on Oct. 29, appreciated 177 won to the dollar the following day after the news broke of the currency swap.

The recent currency swap helped the market recover rapidly.

The day after the announcement was made on March 19, the Kospi gained 108.51 points or 7.44 percent. The won appreciated from 1,285.7 won to 1,246.5 won.

Some market experts doubt that the influence of the currency swap will last. They say that even in 2008, the rebound was short lived as the Korean won depreciated, eventually edging close to 1,500 won against the dollar.

BY LEE HO-JEONG, RICHARD MEYER [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)